Maximizing credit cards is one of the best ways to elevate your travel. This can include getting the credit cards with the best welcome bonuses, using the right credit cards for your everyday spending, maximizing credit card bonus categories, and taking advantage of other credit card perks.

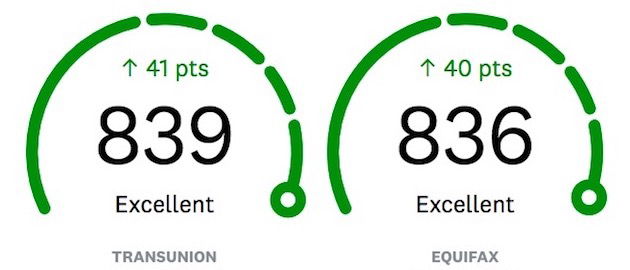

There are a lot of misconceptions about the impact that applying for credit cards can have on your credit score. I have over two dozen credit cards, and my credit score is excellent.

In this post I wanted to first share a brief intro regarding how applying for credit cards impacts your credit score, then I’ll talk about what goes into my credit card decision making process, and then I’ll share the cards I have open.

In this post:

How credit cards impact your credit score

There are a lot of misconceptions about how credit scores work, in particular people thinking that applying for credit cards hurts your credit score. That’s generally not true, and in many cases applying for cards can even help your credit score in the long run.

The beginners guide on the blog has a section about credit cards and credit scores, and should provide some insights on that. For context, I have a lot of credit cards, and my credit score is almost perfect, in the top couple of percent nationwide.

For those of you not familiar, here’s what factors into your credit score:

- 35% of your score is your payment history (the percentage of payments you’ve made on-time)

- 30% of your score is your credit utilization (how much credit you’re using compared to your total limits)

- 15% of your score is your credit age (the average age of your open accounts)

- 10% of your score is the types of credit you use (how many different types of requests for credit you have)

- 10% of your score is your requests for new credit (how many times you’ve applied for credit)

What’s most important is that you pay your bills on time, don’t utilize too much of your credit (meaning you want to ideally use 20% or less of your total available credit, and/or pay your credit card bills early), and keep some cards long term, which will help increase your average age of accounts.

The only metric that’s lowered by applying for cards is your requests for new credit, but that makes up just 10% of your score. Furthermore, credit inquiries typically fall off your report after 24 months.

Closing credit cards that are no longer working for you potentially doesn’t harm your credit much either, though alternatively you can also often downgrade credit cards instead.

What I look for in credit cards

For me, there are three things I look for when applying for credit cards:

- Credit cards that offer a big welcome bonus — often the introductory bonuses on cards are compelling, and enough reason to pick up a new card

- Credit cards that offer a generous return on everyday spending — there are some cards you have because they help you maximize the points you earn, either for everyday spending or for specific spending categories

- Credit cards that offer ongoing perks that more than justify the annual fee — some cards are worth holding onto even if you don’t plan on putting much spending on them, because they offer things like elite status, annual free nights, etc.

The 30 credit cards that I have right now

Now let me share what cards I have at the moment. I have 30 open credit cards right now — so far this year I’ve canceled one card and have applied for two cards, so I now have the most cards I’ve had in quite some time.

Below are the credit cards that I have, broken down by issuer.

My nine American Express cards

- The Platinum Card® from American Express (review) — this card has a $695 annual fee (Rates & Fees), and offers many perks that help offset it, including Amex Centurion Lounge access, Hilton and Marriott hotel status, a $240 annual digital entertainment credit, a $200 annual airline fee credit, a $200 annual Uber credit, a $200 annual hotel credit (min 2-night stay required for Hotel Collection, 1 night for Fine Hotels & Resorts), an up to $189 annual CLEAR Plus credit, a $100 annual Saks credit, and more (Enrollment is required for select benefits)

- Business Platinum Card® from American Express (review) — this card has a $695 annual fee (Rates & Fees), and offers perks to help offset that; I grabbed this card when I received a great targeted offer

- American Express® Business Gold Card (review) — this card has a $375 annual fee (Rates & Fees), and has a solid rewards structure; I opened this card account when I received a great targeted offer

- American Express® Green Card (review) — this card has a $150 annual fee (Rates & Fees), and offers all kinds of great perks, including 3x points on dining and travel, an up to $189 annual CLEAR Plus credit, and a up to $100 annual LoungeBuddy credit (Enrollment required)

- Amex EveryDay® Preferred Credit Card from American Express (review) — this card has a $95 annual fee, and offers 3x points at US supermarkets (on up to $6,000 of spending per year, then 1x) and 2x points at US gas stations, plus a 50% points bonus when you make at least 30 transactions per billing cycle

- Marriott Bonvoy Business® American Express® Card (review) — this card has a $125 annual fee (Rates & Fees), and offers an anniversary free night certificate on your account anniversary every year valid at a property costing up to 35,000 points per night, plus 15 elite nights per year, which more than justify the annual fee

- Marriott Bonvoy Brilliant® American Express® Card (review) — this card has a $650 annual fee (Rates & Fees), and offers benefits that more than justify the annual fee, including Platinum Elite status, up to $300 in statement credits per calendar year (up to $25 per month) for eligible purchases at restaurants worldwide.), plus an anniversary free night valid at a property costing up to 85,000 points per night

- Hilton Honors American Express Aspire Card (review) — this $550 annual fee card offers incredible perks, including Hilton Honors Diamond status for as long as you have the card, an annual free night certificate, a $250 Hilton resort credit every cardmember year, and a $250 airline fee credit every calendar year

- The Blue Business® Plus Credit Card from American Express (review) — this card has a $0 annual fee (Rates & Fees), and I consider it to be one of the most rewarding business cards out there, given that it offers 2x Membership Rewards points on the first $50,000 spent every calendar year (then 1x)

See this post for the best credit cards for earning Amex points, and this post for my American Express card strategy.

The information and associated card details on this page for the Hilton Honors American Express Aspire Card, American Express Green Card, and Amex EveryDay Preferred Credit Card has been collected independently by OMAAT and has not been reviewed or provided by the card issuer.

My one Bank of America card

- Alaska Airlines Visa® Business card (review) — this card has a $95 annual fee for one cardmember ($70 for the company and $25 per card), and offers several valuable perks, including an annual companion certificate, a first checked bag free, 20% back on Alaska Airlines inflight purchases, and more

My two Barclays cards

- JetBlue Plus Card (review) — this card offers a 5,000 point bonus on the account anniversary each year, plus a 10% refund on JetBlue points redemptions, which to me justifies the $99 annual fee

- AAdvantage Aviator Business Mastercard (review) — I picked up this card recently when it was offering a big bonus, but I doubt I’ll keep this card in the long run

My four Capital One cards

- Capital One Venture X Rewards Credit Card (review) (Rates & Fees) — this card has a $395 annual fee, but offers all kinds of amazing perks, including a $300 annual travel credit, 10,000 anniversary bonus miles, a Priority Pass membership, Plaza Premium lounge access, amazing authorized user perks, and much more

- Capital One Spark Cash Plus (review) (Rates & Fees) — this card has a $150 annual fee, and is currently my go-to card for everyday business spending, especially given that rewards can be converted into Capital One miles

- Capital One Spark Miles for Business (review) (Rates & Fees) — this card has a $95 annual fee (waived the first year), and offers 2x Spark miles per dollar spent, and Capital One miles can be transferred to airline partners

- Capital One SavorOne Cash Rewards Credit Card (review) (Rates & Fees) — this no annual fee card offers many great benefits, the most exciting of which is a complimentary Uber One membership and 10% cash back on Uber and Uber One through November 14, 2024

See this post for the best credit cards for earning Capital One miles, and this post for my Capital One card strategy.

My 11 Chase cards

- Chase Sapphire Reserve® (review) — this $550 annual fee card offers 3x points on dining and travel, a $300 annual travel credit, and lots of other great perks, including with DoorDash, Instacart, and Lyft

- Ink Business Preferred® Credit Card (review) — this $95 annual fee card is the all around best business card, as it offers 3x points on the first $150,000 spent in combined purchases every cardmember year on travel, shipping purchases, internet, cable, and phone services, and advertising purchases made with social media sites and search engines; the card also offers a great cell phone protection benefit, rental car coverage, and more

- Ink Business Unlimited® Credit Card (review) — this no annual fee card offers 1.5x points on all purchases, so is one of the best cards for non-bonused business spending; points can be combined with Ultimate Rewards points earned on other cards

- Ink Business Cash® Credit Card (review) — this no annual fee card offers 5x points on the first $25,000 spent in combined purchases every cardmember year on office supply stores, and on cellular phone, landline, internet, and cable TV services, and 2x points on the first $25,000 spent at gas stations and restaurants; points can be combined with Ultimate Rewards points earned on other cards

- Chase Freedom FlexSM (review) — this no annual fee card offers 5x points in rotating quarterly categories, and these points can be combined with Ultimate Rewards points earned on other cards

- Chase Freedom Unlimited® (review) — this no annual fee card offers 1.5x points in non-bonused categories, and these points can be combined with Ultimate Rewards points earned on other cards; I downgraded my Chase Sapphire Preferred® Card (review) to this card in 2016

- British Airways Visa Signature® Card (review) — this $95 annual fee card is well worth it to me thanks to all the benefits it offers, like 10% off British Airways flights, up to $600 in reward flight statement credits, and more

- World of Hyatt Credit Card (review) — this $95 annual fee card is worth it for the five nights toward status annually, anniversary free night certificate, as well as the ability to put spending on the card to earn more elite nights and a second anniversary free night certificate

- World of Hyatt Business Credit Card (review) — this $199 annual fee card was recently introduced, and offers a big welcome bonus, up to $100 in Hyatt credits annually, and more

- IHG One Rewards Premier Credit Card (review) — this card offers all kinds of great perks, including an annual free night certificate valid at any IHG hotel retailing for up to 40,000 points per night, a fourth night free on award redemptions, and a lot more

- IHG® Rewards Club Select Credit Card — this card offers an annual free night certificate valid at any IHG hotel retailing for up to 40,000 points per night, which more than justifies the card’s $49 annual fee; this card is no longer being issued

See this post for the best credit cards for earning Chase points, and this post for my Chase card strategy.

My three Citi cards

- Citi Double Cash® Card (review) — this no annual fee card offers 1% cash back when you make a purchase and 1% cash back when you pay for that purchase in the form of ThankYou points

- Citi Prestige® Card (review) — this card has a $495 annual fee but offers lots of great perks, including a $250 annual travel credit, 5x points on dining and airfare, and more; I’m seriously considering downgrading this card to the Citi Strata Premier℠ Card (review)

- Citi® / AAdvantage® Executive World Elite Mastercard® (review) — this $595 annual fee card offers an Admirals Club membership for the primary member; authorized users each get Admirals Club access as well

See this post for the best credit cards for earning Citi points, and this post for my Citi card strategy.

Bottom line

Hopefully the above is an interesting rundown of the credit cards I have. I’d like to think that almost all of these credit cards serve a purpose as part of my long-term credit card strategy, either because they offer an excellent rewards structure, or because they offer perks that make the cards worth holding onto.

There are a few cards that I plan on canceling at their account renewal, though I’ll deal with those situations as they arise. As you can see, my credit score is also excellent in spite of how many credit cards I have, which should hopefully put some of you at ease who are considering applying for new cards.

How many credit cards do you have right now?

The following links will direct you to the rates and fees for mentioned American Express Cards. These include: American Express® Business Gold Card (Rates & Fees), The Blue Business® Plus Credit Card from American Express (Rates & Fees), The Business Platinum® Card from American Express (Rates & Fees), The Platinum Card® from American Express (Rates & Fees), Marriott Bonvoy Brilliant® American Express® Card (Rates & Fees), Marriott Bonvoy Business® American Express® Card (Rates & Fees), and American Express® Green Card (Rates & Fees).

Ben, what was the first ever credit card you applied for?

That is a lot of cards in the Amex and Chase eco system.

Just from what you wrote above, it appears to me that you get MORE benefits from the Citi Prestige card (now closed to new applicants) than from the Chase Sapphire Reserve. Could you elaborate why you are thinking of downgrading to the Citi Premiere?

I won't lie: that looks exhausting af. I know it's easy for you to do all these since you get to write off the annual fees and maybe you have the time to enjoy the perks, but I like @Lee's question elsewhere in this discussion: boil it down to three cards in your daily rotation and three cards in your sock drawer for special occasions.

I wouldn’t say it’s *easy* for Ben, but it’s his business to have/review/encourage you to apply for lots of credit cards.

But that’s an interesting suggestion for future posts.

“The three credit card package for [a particular type of user]” Lather/rinse/repeat. Ben, you can thank me later.

It is very possible that these are cards between 2 people with authorized users.

My husband & I have 11 cards between us & I am CONSTANTLY deliberating others to apply for. Yes, we pay $1200/yr in annual fees but the benefits AT LEAST offset what we pay. For that we get 4 free nights/yr at IHG properties, $300 travel credit (on ANY travel purchase), 8 free SWA upgrades, 12K SWA points ($180 value),...

It is very possible that these are cards between 2 people with authorized users.

My husband & I have 11 cards between us & I am CONSTANTLY deliberating others to apply for. Yes, we pay $1200/yr in annual fees but the benefits AT LEAST offset what we pay. For that we get 4 free nights/yr at IHG properties, $300 travel credit (on ANY travel purchase), 8 free SWA upgrades, 12K SWA points ($180 value), plus excellent travel insurance that even covers Med Evac--not to mention all the points we earn for travel (we put EVERYTHING on cards & pay the off monthly; we take advantage of any bonus charging categories that we can).

I only have five. Amex Gold, Chase Preferred, BA, AA and UA. I've had them for decades. I'd like to venture into Ben's multiple card world to get some miles but pretty sure something would go arwy.

Ben, you have several "anchor" CC's on your report (from your parents history) and also several early CC's of your own (teenage years/18, etc.) Most of your readers started the Credit game MUCH later than you (I was in my late 20's and now at 36 my oldest card is around 8 years old). I now have 7 cards (9 if you count store cards) and when I open up a new one, it SEVERELY...

Ben, you have several "anchor" CC's on your report (from your parents history) and also several early CC's of your own (teenage years/18, etc.) Most of your readers started the Credit game MUCH later than you (I was in my late 20's and now at 36 my oldest card is around 8 years old). I now have 7 cards (9 if you count store cards) and when I open up a new one, it SEVERELY affects my average age of credit, and for 6 mtns to a year my score is lower. I've opened 3-4 of those through your links and am very happy where I'm at on my credit/rewards journey (and thankful for your guidance). But it would also be helpful to see the full picture for the "average consumer". I wish I could get a card on my credit history that was older than I am, but that's just not possible for me.

Can you do the math and let us know what your average points per dollar is on all spending combined?

The expression “Not enough hours in the day…” comes to mind.

The word "dinosaurs" comes to mind.

6 banks, 30 cards. Probably few hours coding for the 6 banks. few mins per card for a data dump to spreadsheet, an hour coding in Excel.

For someone with a bit of experience, very doable in 8 hours, and another 16 to spare for the rest of the day. Likely a modest cost to hire someone to do this project.

However, the project is likely a waste of...

The word "dinosaurs" comes to mind.

6 banks, 30 cards. Probably few hours coding for the 6 banks. few mins per card for a data dump to spreadsheet, an hour coding in Excel.

For someone with a bit of experience, very doable in 8 hours, and another 16 to spare for the rest of the day. Likely a modest cost to hire someone to do this project.

However, the project is likely a waste of time and money. The average doesn't really mean anything at all since your spending profile is likely different than others. Same as the 3 card covering 90% theory it might fit your profile, but correlation isn't causation.

You could be spending thousands per month while others is spending hundred of thousand.

You could be spending 20 times more in a bonus category than non bonus while others are spending evenly in every category.

I saw a comment to a different article a while back saying something like 90 to 95 percent of the theoretical maximum points attainable from ongoing spending are captured by only three well-picked cards. A fourth card adds only 2 to 4 percent. I tried it in my own situation and found it to be the case. Of course, the specific cards will differ for each person. (This excluded sign-up bonuses.)

Ben, imagine limiting yourself to keeping only three credit cards that you carry with you (in your real wallet). And, imagine keeping only three "sock drawer" credit cards that you actually use but don't need to carry with you. What would those be?

Why leave money on the table with only 3 cards in the "sock drawer"?

I don't get some of the comments here, you either maximize your returns or sacrifice them for simplicity. No need to handicap yourself for an arbitrary number "3".

But to entertain all these not so useful question.

The least complicated 3 cards that maximizes return is probably a 5% category cashback card.

So get

1. Elan Max Cash

Why leave money on the table with only 3 cards in the "sock drawer"?

I don't get some of the comments here, you either maximize your returns or sacrifice them for simplicity. No need to handicap yourself for an arbitrary number "3".

But to entertain all these not so useful question.

The least complicated 3 cards that maximizes return is probably a 5% category cashback card.

So get

1. Elan Max Cash

2. US Bank Cash+

3. Citi Custom cash

Very simple, yet all are 5% category of your choice cash back.

Simplicity is where I'm going with this. As a practical matter, at what point is the juice not worth the squeeze? Referring to my other comment, after 3 or 4 cards (wallet+sock drawer), the incremental value of each added card becomes smaller and smaller. For me, if a given card does not add $X of incremental value relative to my existing set of cards, I pass on it.

The three cards you pick are interesting....

Simplicity is where I'm going with this. As a practical matter, at what point is the juice not worth the squeeze? Referring to my other comment, after 3 or 4 cards (wallet+sock drawer), the incremental value of each added card becomes smaller and smaller. For me, if a given card does not add $X of incremental value relative to my existing set of cards, I pass on it.

The three cards you pick are interesting. Typically, such cards have dollar limits on the 5% rate and cannot scale. Such cards typically have foreign transaction fees. While you note the 5% earn rate on these cards, the earn rate doesn't present the whole picture. What about the redemption rate with which it would be combined to achieve an overall reward rate? When I seek cash back from a card, I look for an overall reward rate of 7.5%+.

But, what if a person's objective is not cash back? What if a person's objective is transferable points? And, what card(s) might one have for travel? Without foreign transaction fees?

And, so, I've asked Ben what his choices are. I'm not suggesting that the cards Ben picks are those that anyone else should pick. I'm just asking Ben.

And exactly my point of this is a not so useful question.

You bring up,

-such cards have dollar limits

-have foreign transaction fees

-redemption rate

-I look for an overall reward rate of 7.5%+.

-what if a person's objective is not cash back

These are all 'your' requirements specific to 'you'.

The 3 cards I picked is as plain generic and simple as it gets, and you...

And exactly my point of this is a not so useful question.

You bring up,

-such cards have dollar limits

-have foreign transaction fees

-redemption rate

-I look for an overall reward rate of 7.5%+.

-what if a person's objective is not cash back

These are all 'your' requirements specific to 'you'.

The 3 cards I picked is as plain generic and simple as it gets, and you don't like it a bit.

Your requirements is counter to what you're expecting, simplicity.

Not Ben nor anyone can really tell you 'at what point is the juice not worth the squeeze?'

What Ben and others can help you is you giving "your" exact spending patterns, credit profile, and expected redemption. We could then suggest you how to 'squeeze the juice' after that it's up to you to decide what point is the juice not worth the squeeze?'

Ben never suggest anyone to hold the same cards. But his choice is pretty clear, why limit the cards when you can pick 30 cards. He even gave reasons to pick each.

But to entertain all these not so useful question, again. (which probably is not what you want to hear, again) but bounded by your new constraints

1. Citi Prestige

2. Citi Double Cash

3. Citi Rewards+

Two guys are sitting at a bar. One asks the other what three songs he likes the best . . . or the three movies. You interrupt the conversation and say that this is not a useful question. Why would someone limit himself to only three songs or movies? And, the three songs or movies the one person likes are going to be different from the songs or movies that any other person likes. So,...

Two guys are sitting at a bar. One asks the other what three songs he likes the best . . . or the three movies. You interrupt the conversation and say that this is not a useful question. Why would someone limit himself to only three songs or movies? And, the three songs or movies the one person likes are going to be different from the songs or movies that any other person likes. So, it is inappropriate to even ask the question.

I simply want to know Ben's choices for his situation. Not what he thinks is appropriate for anyone else. Just him.

And, to be clear, at no point did I ever ask you about your cards or your situation.

What I look for in a (one, singular) credit card:

- An issuer with a reputation for treating customers fairly. Strange that credit card reviews don't mention that, yet it ought to be the single most important criterion. It's your money and credit rating that's on the line, after all.

- No annual fee. It's just a credit card, not some snooty club I'm joining to show off.

- Simple, no-effort-needed cashback on...

What I look for in a (one, singular) credit card:

- An issuer with a reputation for treating customers fairly. Strange that credit card reviews don't mention that, yet it ought to be the single most important criterion. It's your money and credit rating that's on the line, after all.

- No annual fee. It's just a credit card, not some snooty club I'm joining to show off.

- Simple, no-effort-needed cashback on all purchases. Life is too short to be mucking around with points that can be devalued or with shifting reward categories.

And that's all. I get it that some people enjoy the gamification of everything and more power to them. But I'll take simple, thanks.

I ask out of pure curiosity (and truly am not being snotty with the question)- then why are you spending time reviewing and commenting on these sites that are points and miles focused? It seems to be the focus of most of them. Do you find you get enough value on flight/ lounge/ hotel reviews that it's still worth it? truly just curious.

I appreciate the question; have a "helpful" vote! I love travel (even business travel, which I suppose makes me a freak) and find OMAAT to be a great source of travel information. Although my free agent approach to airlines, hotels, and payment options serves me well, I don't mind OMAAT's points & miles focus.

Re-reading my earlier message I see that it was singularly unhelpful to anyone inspired to read Ben's article, and if there...

I appreciate the question; have a "helpful" vote! I love travel (even business travel, which I suppose makes me a freak) and find OMAAT to be a great source of travel information. Although my free agent approach to airlines, hotels, and payment options serves me well, I don't mind OMAAT's points & miles focus.

Re-reading my earlier message I see that it was singularly unhelpful to anyone inspired to read Ben's article, and if there was a "withdraw post" button I would use it. I'll try to be more on topic and thanks for provoking these thoughts.

You want a simple cash back card with no annual fee. Fair enough. Do you travel outside the US? If yes, then it will not be so simple. You will need a cash back card with no annual fee and no foreign transaction fees. Pray tell, what's your card?

I live and travel mostly outside the U.S., so yes, a card with no foreign transaction fees is a must for me. My card is the Premium CashBack+ from State Department Federal Credit Union. Being issued by a credit union you'll have to join, but that is possible even if you don't qualify by employment and it gets you better customer service than you'll get from some commercial banks.

No points, no miles, not...

I live and travel mostly outside the U.S., so yes, a card with no foreign transaction fees is a must for me. My card is the Premium CashBack+ from State Department Federal Credit Union. Being issued by a credit union you'll have to join, but that is possible even if you don't qualify by employment and it gets you better customer service than you'll get from some commercial banks.

No points, no miles, not many perks, just a boring 2% back on everything, so it's probably not what most readers here are looking for. But I did want to answer your good question.

https://www.sdfcu.org/premium-cash-back

XPL, based on your comments, here's one to consider:

https://www.penfed.org/credit-cards/pathfinder-rewards-visa

Best of luck.

Drastically simplified the Doubt family cards in 2022.

AMEX Platinum for flights, occasional AMEX hotels.

Amazon Prime VISA for Amazon.

BofA Preferred Rewards VISA for everything else.

I’m mostly out of the game now, but still enjoy reading about it vicariously through OMAAT!

@Lucky: Sorry if I missed it, but do you fully pay off all your credit cards BEFORE their statements close?

Here's a question for you Ben - surely you don't carry a wallet around with you with 30 credit cards in it? If you lost it or were robbed that would be like a full days work to cancel all the cards.

Do you use Apple Pay/Google Pay instead?

I’m sure “In my wallet” is a figure of speech.

These are VanageScore I believe, not the real FICO score. My real FICO score is always 50 points less.

Hey Ben,

Instead of downgrading your Citi Prestige to the Citi Premier, why not downgraded it to Citi Rewards+ and apply for a new Citi Premier to get the extra 80,000 TY points?

This article cracks me up!! 30 credit cards and roughly $6k/year in annual fees? I'm not sure there was a card you didn't mention nor does this remotely relate to the "Average Joe". Even your credit score is unrealistic to ALOT of people. Thanks for giving information about each card?

I imagine he would write off all the card fees as a business expense.

I do agree this article is not very useful for the 99.99% of people who would not wish to have 30 credit cards.

The article is not for people who want 30 credit cards. It's a list of cards that Lucky finds useful and uses and readers may find a few are useful for them.

Seems silly to have a bunch of cards that do the same thing. The Amex Green gets a Clear credit so does Platinum and the Green gets 3x for restaurants but Gold gets 4x - so why have the Platinum, Green, and Business Gold when the regular Gold and Platinum does the same as all three? Save yourself five bills.