I have over two dozen credit cards, though I hold onto these cards for a variety of reasons. I have some of these cards because they help me maximize my everyday spending, while I have other cards because of the ongoing perks that they offer.

In this post I wanted to share the cards that I spend the most money on, as this has evolved over time.

In this post:

Credit cards worth having for the benefits

There are cards I keep long term primarily for the benefits they offer, without actually putting much spending on them. Just to give a few examples:

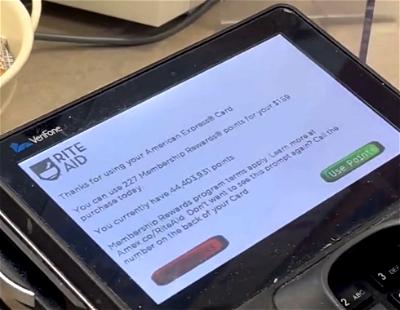

- The Platinum Card® from American Express (review) has a $695 annual fee (Rates & Fees) and is worthwhile for all of the credits that it offers (for airline fees, Uber, hotels, CLEAR, etc.), plus the lounge access, including access to Centurion Lounges, Delta Sky Clubs, and more (Enrollment is required for select benefits)

- The Marriott Bonvoy Brilliant® American Express® Card (review) has a $650 annual fee (Rates & Fees) and is worthwhile for up to $300 in dining statement credits per calendar year (up to $25 per month) for eligible purchases at restaurants worldwide, as well as a free night award valid at properties costing up to 85,000 points per night.

- The IHG One Rewards Premier Credit Card (review) has a $99 annual fee and offers an anniversary free night certificate, IHG One Rewards Platinum status, a fourth night free on award redemptions, and more

Credit cards I spend the most money on

With the above out of the way, I figured I’d talk a bit about the cards I use most for everyday spending, including personal and business purchases.

Which cards are at the top of my wallet, and under what circumstances do I use them? I use some cards because they maximize my return on everyday spending, while I use other cards because they have valuable category bonuses, ranging from dining, to groceries, to gas stations.

Below are the nine cards that I’m spending the most money on, roughly in the order of the amount that I spend on them annually.

Capital One Venture X Rewards Credit Card

This $395 annual fee card has become my go-to card for everyday personal spending. The card offers 2x miles per dollar spent with no foreign transaction fees, and I consider Capital One miles to be just as valuable as other transferable points currencies, given all the great transfer partners.

While some people may initially be put off by the card’s annual fee, personally I don’t view this card as actually costing much to hold onto, given that it offers a $300 annual travel credit, 10,000 anniversary bonus miles, and much more.

I value Capital One miles at 1.7 cents each, so to me this card offers a 3.4% return on all spending.

Read a full review of the Capital One Venture X, apply for the Capital One Venture X (Rates & Fees).

Capital One Spark Cash Plus

This $150 annual fee card is now my go-to card for everyday business spending. The card offers 2% cash back on all purchases with no foreign transaction fees. While this is a cash back card on the surface, the beauty is that in conjunction with another card earning Capital One miles (like the Venture X), cash back can be converted into Capital One miles at the rate of one cent per mile. So in reality this card can also earn me 2x miles per dollar spent.

I value Capital One miles at 1.7 cents each, so to me this card offers a 3.4% return on all spending.

Read a full review of the Capital One Spark Cash Plus, apply for the Capital One Spark Cash Plus (Rates & Fees).

Citi Double Cash® Card

This no annual fee card offers 1% cash back when you make a purchase and 1% cash back when you pay for that purchase (in the form of ThankYou points).

That’s a good return for a no annual fee card in and of itself, but what makes this card more exciting is that rewards earned on that card can be converted into airline miles and hotel points, assuming you have it in conjunction with a card like the Citi Strata Premier℠ Card (review).

I value Citi ThankYou points at 1.7 cents each, so to me this card offers a 3.4% return on all spending. For all practical purposes, this offers the same return as the Capital One Venture X (except this card has foreign transaction fees), but sometimes it’s nice to diversify the points you earn, which is why I also put spending on this card.

Read a full review of the Citi Double Cash, apply for the Citi Double Cash.

The Blue Business® Plus Credit Card from American Express

This is my backup business card for non-bonused spending. Specifically, the no annual fee (Rates & Fees) Blue Business Plus offers 2x Membership Rewards points on the first $50,000 spent annually (1x after that). That makes this the other card that earns me 2x transferable points for my business spending, allowing me to diversify my points a bit.

I value Amex Membership Rewards points at 1.7 cents each, so to me this card offers a 3.4% return on everyday spending.

Read a full review of the Amex Blue Business Plus, apply for the Amex Blue Business Plus.

Chase Sapphire Reserve®

This card has a $550 annual fee, though offers a $300 annual travel credit that can be applied toward any purchase coded as travel, making it one of the easiest to use travel credits. Therefore I consider this card to really cost me $250 per year. The card also offers several useful perks, including a Priority Pass membership.

When it comes to spending, this card offers 3x points on dining and travel. The travel category is particularly useful for me, and this card gets most of my non-airfare travel spending. On top of that, what’s great about this card is that it’s an excellent “hub” card that allows you to maximize the Ultimate Rewards points you earn across all cards.

I value Chase Ultimate Rewards points at 1.7 cents each, so to me this card offers a 5.1% return on dining and travel.

Read a full review of the Chase Sapphire Reserve, apply for the Chase Sapphire Reserve.

The Platinum Card® from American Express

While I primarily have the Amex Platinum for the perks that it offers, it’s still a card that I spend a significant amount on. That’s because the card offers 5x points on airfare purchased directly with airlines (up to $500,000, and then 1x), and it also offers excellent travel coverage. I spend quite a bit on airfare, so earning 5x points on those purchases while having solid travel protection is great.

I value Amex Membership Rewards points at 1.7 cents each, so to me this card offers an 8.5% return on airfare.

Read a full review of the Amex Platinum Card, apply for the Amex Platinum Card.

World of Hyatt Credit Card

While I wouldn’t ordinarily say this is the best card for everyday spending, I put $15,000 of spending on the Hyatt Card for a reason.

The card already offers five elite qualifying nights plus a Category 1-4 free night certificate annually just for paying the $95 annual fee.

On top of that, you get an additional two elite nights toward status annually for every $5,000 you spend, and you also get a second Category 1-4 free night certificate when you spend $15,000 on the card in a cardmember year.

This means that if you spend $15,000 on the card you’re getting an incremental six elite nights (this can help you earn Globalist status) plus a second free night certificate, which I find to be well worth it. I also try to make as much of my spending be at Hyatt hotels (where I earn 4x points).

Read a full review of the World of Hyatt Card, apply for the World of Hyatt Card.

Citi Prestige Card

This card isn’t nearly as valuable as it used to be, between the fourth night free benefit being watered down, as well as travel coverage being removed from the card.

However, this is a card I continue to use for the 5x points that it offers on dining. Not only does the card earn 5x points when dining out, but you can also earn 5x points on restaurant takeout and delivery, which is pretty awesome. I value Citi ThankYou points at 1.7 cents each, so to me this card offers an 8.5% return on dining.

The card does have a $495 annual fee, though the card’s $250 annual travel credit helps offset that. Furthermore, this card allows me to maximize the value I get with the Citi Double Cash, which is a vital part of my Citi credit card strategy.

The Citi Prestige is no longer open to new applicants, so if you’re looking to get into the Citi ecosystem I recommend picking up the mid-range Citi Premier® Card (review) instead, with a lower annual fee but compelling bonus categories and maintaining the ability to maximize the Citi Double Cash.

Read a full review of the Citi Prestige.

Bilt Mastercard®

This no annual fee card is also my newest credit card, and it is working out quite well for me. While the Bilt Mastercard is known for letting you earn points for paying your rent with no fee, I’ve had luck using this card to pay my HOA. That means I’ve been able to earn credit card rewards for my HOA, all without paying a fee.

This does require making at least five purchases with the card per billing cycle, so I also use the card for some other purchases. As much as possible, I spend on the first day of the month, as Bilt offers double rewards on that date. This is a very well rounded and lucrative card, though currently that’s the extent of how I use it.

Read a full review of the Bilt Mastercard, apply for the Bilt Mastercard.

Other credit cards I spend money on

The above are the nine cards that I’ve been putting the most spending on, though there are some other cards that I put spending on for specific reasons:

- I use the Hilton Honors American Express Aspire Card (review) at Hilton properties, as it offers 14x points

- I use the Amex EveryDay® Preferred Credit Card from American Express (review) at supermarkets and gas stations, though frankly I don’t spend much at either of those

- I use the Chase Freedom FlexSM (review) for spending in rotating quarterly categories

All of these are cards that I find useful as well, though I don’t put $15,000+ of spending per year on any of those cards.

The information and associated card details on this page for the Hilton Honors American Express Aspire Card and Amex EveryDay Preferred Credit Card has been collected independently by OMAAT and has not been reviewed or provided by the card issuer.

Bottom line

I’d like to think I have a pretty good credit card setup, as I’m earning anywhere from 2-5x points per dollar spent on my credit cards for everyday spending. When you factor in all the cards, I’m earning over 3x points per dollar spent on average, which I’d value at a return of over 5%. That’s excellent if you ask me.

To recap:

- My favorite cards for everyday, non-bonused personal spending are the Capital One Venture X and Citi Double Cash

- My favorite cards for everyday, non-bonused business spending are the Capital One Spark Cash Plus and Amex Blue Business Plus

- I use the Chase Sapphire Reserve for my non-airfare travel purchases, the Amex Platinum for my airfare purchases, and the Citi Prestige for my dining purchases

- I think it’s worth spending $15,000 on the World of Hyatt Card every year for the additional six elite nights plus free Category 1-4 certificate

- The Bilt Mastercard lets me earn rewards for paying my HOA, all without having to pay a credit card fee

What are the primary cards you use for your credit card spending?

The following links will direct you to the rates and fees for mentioned American Express Cards. These include: The Blue Business® Plus Credit Card from American Express (Rates & Fees), The Platinum Card® from American Express (Rates & Fees), and Marriott Bonvoy Brilliant® American Express® Card (Rates & Fees).

Bottom line, you are being paid to promote the cards you have. I am unsure how you obtain the values or percentages for points that you earn. I think it should be based on redemption habits and the relative cash cost of your redemption. so I think people value different point related cards differently.

If you spend using touch-pay, you gotta have US Bank Altitude Reserve for 3X points. 325 annual travel/dining credit with 400 annual fee with lots of other benefits. Offset the annual fee for 30k points.

Same as other people. Very surprise that didn't see Amex Gold in your portfolio.

Also, could you share about brand of card holder and wallet that you use?

I found your blog about 9 years ago which I have 2 credit cards and 1 charge card. After reading your blog, now I have 14 cards (most of them apply through your link)

Ben, just curious . . . across all of your spending, how many points per dollar are you averaging? Thanks.

Disregard. I see your overall results near the end.

1)Everything online and paid via store app (such as Publix or walmart checkout), domestic air travel : Bofa Custom Cash rewards (Mastercard) - 5.623%

2)Foreign spend: BofA Travel Rewards 2.625%

3)Hotels: Amex Hilton Surpass

4)Dining: BofA Custom Cash rewards (Visa) 5.625% & Amex Gold 4x

When I exceed the quarterly $2500 limit on the BofA Mastercard (#1), I simply switch the #4 BofA Visa Card to Online spending category and put Amex...

1)Everything online and paid via store app (such as Publix or walmart checkout), domestic air travel : Bofa Custom Cash rewards (Mastercard) - 5.623%

2)Foreign spend: BofA Travel Rewards 2.625%

3)Hotels: Amex Hilton Surpass

4)Dining: BofA Custom Cash rewards (Visa) 5.625% & Amex Gold 4x

When I exceed the quarterly $2500 limit on the BofA Mastercard (#1), I simply switch the #4 BofA Visa Card to Online spending category and put Amex Gold to work for dining for the rest of the quarter

ALso all other blogs have enhanced commenting system allowing edits. when will OMAAT have such capability?

Forgot to mention that BofA Travel rewards also gets all my other spend.

How thick is your wallet?

I have the Citi Rewards + CC. With this card I receive a 10% rebate on on all of my Citi Premier CC redemptions. When combined with the Double Cash CC, they are earning 3.3% or 2.2%.

I have been using the Venture X and SavorOne for more than a year now, and the points adds up real quick. I also have the Amex Green Card for the ClearMe benefit and Amex Offers. But here is the thing, I basically don't travel, maybe one or two times in a year. I am thinking to move my spending to PenFed Pathfinder credit card that give me Priority Pass for free (if you are...

I have been using the Venture X and SavorOne for more than a year now, and the points adds up real quick. I also have the Amex Green Card for the ClearMe benefit and Amex Offers. But here is the thing, I basically don't travel, maybe one or two times in a year. I am thinking to move my spending to PenFed Pathfinder credit card that give me Priority Pass for free (if you are a Honors Member, otherwise $95/y) for those 2 times I travel in the year and the Bilt Mastercard.

No Amex Gold for dining and groceries?

Another card I use for cash back but doesnt help for travel points earning is BOA Cash Rewards where as a platinum honors member receive 5.25% cash back on online purchases for $2500 per quarter.

I'm surprised not seeing Amex Gold, 4X in groceries and dining is unbeatable, plus occasional amex transfer bonus.

I have really concentrated my card spending this year:

- Amex Delta Reserve - Will hit $30K soon to reach MQD waiver, MQM bonus, etc.

- Amex Gold - most dining, all grocery

- Chase Sapphire Preferred - some dining, some travel

- Capital One Venture - general spending

- Amex Platinum - airfare, big purchases where I need insurance / protection, other random items

- Apple Card - Uber,...

I have really concentrated my card spending this year:

- Amex Delta Reserve - Will hit $30K soon to reach MQD waiver, MQM bonus, etc.

- Amex Gold - most dining, all grocery

- Chase Sapphire Preferred - some dining, some travel

- Capital One Venture - general spending

- Amex Platinum - airfare, big purchases where I need insurance / protection, other random items

- Apple Card - Uber, drugstores, Apple, random Apple Pay purchases

Other honorable mentions include Chase Freedom Flex, Amex Marriott Brilliant. I haven't engaged much with Citi TYP but I can do Citi Double Cash / Citi Premier when I want to. I am debating whether I should shift Amex Delta Spending to a Citi Mileup to accumulate some Loyalty Points in the second half of the year. Chase Freedom Unlimited has taken a backseat to CapOne Venture for now.