In this post I wanted to share what I consider to be the easiest trick to boosting your credit score with very little effort — that’s to pay off nearly your entire credit card balance not just before the due date, but rather before the statement even closes. Let me explain.

In this post:

What factors impact your credit score?

Having a great credit score is important, not just for maximizing credit card rewards, but for so many things in life. There’s often confusion about how various actions — like applying for credit cards or closing credit card accounts — impact your credit score.

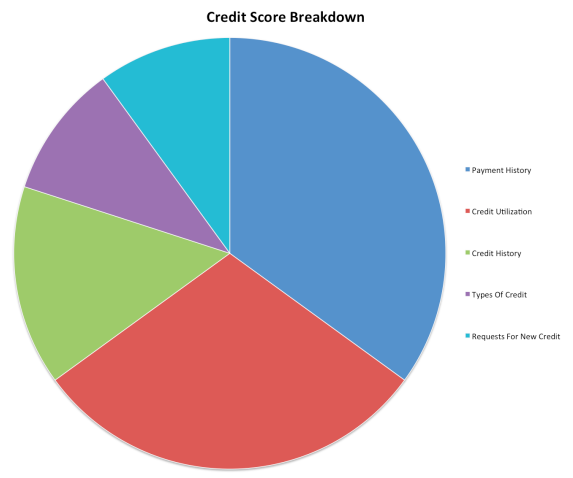

Here are the general factors that make up your credit score:

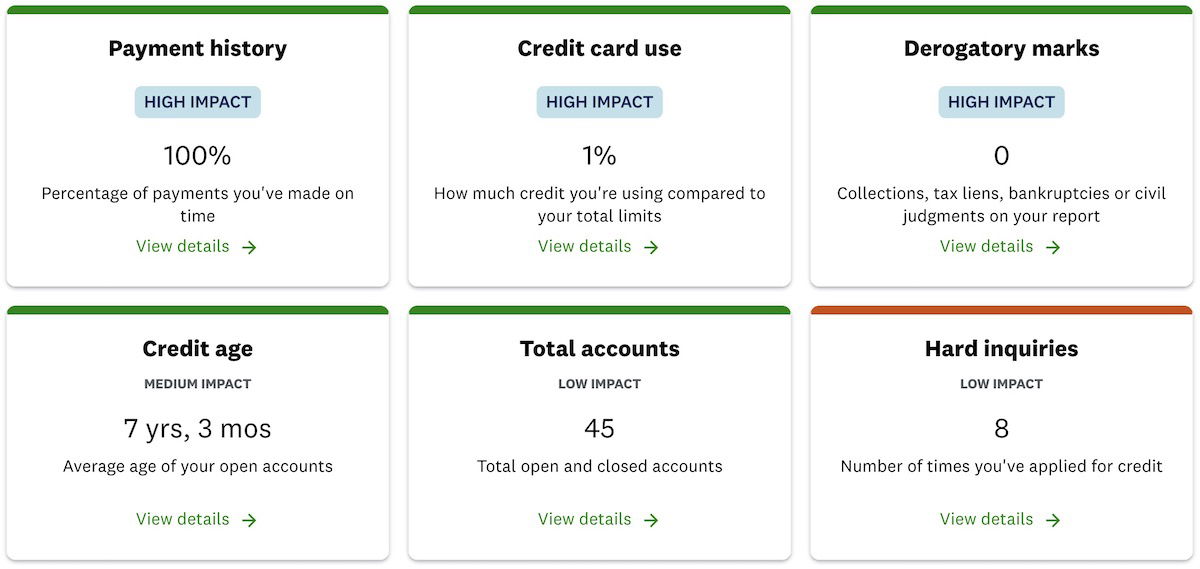

- 35% of your score is your payment history (the percentage of payments you’ve made on-time)

- 30% of your score is your credit utilization (how much credit you’re using compared to your total limits)

- 15% of your score is your credit age (the average age of your open accounts)

- 10% of your score is the types of credit you use (how many different types of requests for credit you have)

- 10% of your score is your requests for new credit (how many times you’ve applied for credit)

For the purposes of this post, let’s focus on the two biggest aspects of your credit score that you can easily control:

- Maintaining a perfect payment history should be easy — just always pay off your balance before the due date

- Keeping your credit utilization low is something you can easily control, and that’s what I wanted to focus on in this post

What is credit utilization?

Credit utilization is the amount of your available credit that you’re using. For example, say that you have a credit card with $10,000 in available credit, and you spend $3,000 during a billing period. Your credit utilization would be 30%, since you’re using $3,000 of your available $10,000 credit line. Generally it’s recommended that you don’t utilize more than 30% of your available credit.

Why do card issuers care about credit utilization? Because it’s viewed as a good indicator of how fiscally responsible and high risk you are as a customer.

For example, if you’re utilizing 90% of your credit every month and then apply for a new credit card, an issuer might assume that you’re higher risk, since you’re using most of the credit you’re being given. If you are given even more credit, will you be able to use it responsibly?

Meanwhile if you utilize only a small percentage of your credit, it shows that you can manage your credit well, and you likely won’t have an issue if you’re extended even more credit.

Pay off most of your balance before statement closes

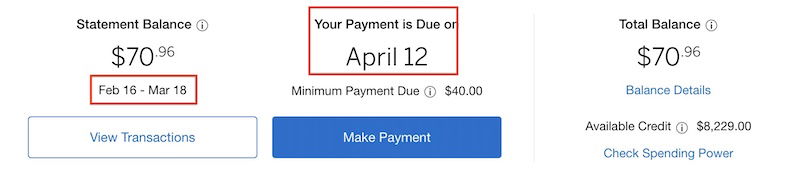

Let me cut to the chase — I pay off a vast majority of my credit card balance before the statement even closes. Yes, I’m talking about the statement close date, which is typically a few weeks before your payment is even due.

The consensus is that you should pay everything off except for a small sum (maybe just a few dollars). Your credit utilization is typically calculated at the time of your statement close date, and you ideally want that percentage to be really low.

Now, some suggest not having a $0 balance when the statement closes, since that might be viewed as the card not having been used at all (I’m not sure if that’s the case or not, but it’s an easy enough system to follow).

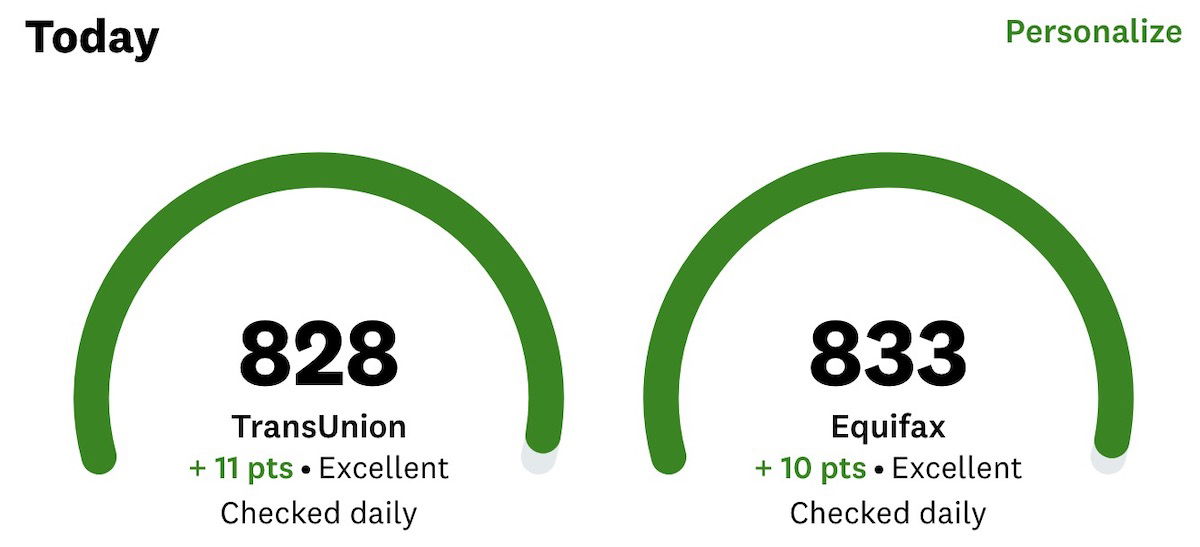

Utilizing only a very small percentage of my credit is a factor that contributes to me having an excellent credit score, and it’s why my credit utilization is only around 1%. Admittedly I have a lot of credit cards, and as a result also have a lot of available credit, but my utilization wouldn’t be that low if it weren’t for consistently paying off most of my balances prior to the statement closing dates.

What’s my strategy, exactly?

- I check all of my credit card transactions once a week

- When I do this I check all of the charges to make sure they’re correct, and I also pay off balances on each of my cards, except for a few dollars

- Given how many cards I have, I find this to be easier than setting a different calendar reminder for each card

How exactly does this help my credit utilization? Typically your credit utilization is measured based on your balance as of your statement closing date, so whatever shows then is what counts:

- If you have $10,000 in available credit and $3,000 in charges when the statement closes, your utilization is 30%

- Meanwhile if you have $10,000 in available credit and you already paid off $2,900 in charges, then your utilization is 1%

- There’s also nothing wrong with taking a hybrid approach — if it’s not practical for you to pay off so much prior to the statement closing date, at least pay off what you can

If you have the liquidity to do it, this is such an easy way to help bump your credit score. Even if you don’t do this on an ongoing basis, it’s absolutely vital that you do this in months where you have big charges and do utilize most of your credit, since a very high credit utilization even for just one billing cycle can do some temporary damage to your credit score.

A few months back I screwed up, and I ended up utilizing 50% of my credit on one particular card, as I made a large purchase shortly before the statement close date. That ended up causing my credit score to drop by around 30 points overnight. Fortunately that was quickly recovered, and things are looking pretty good again…

Bottom line

If you’re in a position to do so, pay off most of your credit card balance early and/or often, ideally before the statement even closes. This will help keep your credit utilization low, which is a major factor that can impact your credit score.

My credit score is nearly perfect, and part of the reason for that is because my credit utilization is somewhere around 1%. That’s primarily thanks to me typically paying off my credit card balance before the statement even closes.

Does anyone else take the same strategy I do, and typically pay off their credit card balance before the statement closing date? If so, what’s your strategy — do you pay off the whole amount, part of the amount, or…?

I pay off my credit cards every week. I download transactions once a week into quicken. Then I instruct my bank to send checks to pay off any balance. My credit score rests above 820.

Where is anybody getting 3% or better, interest rates on savings? Mine are still well below 1%.

Ally is currently at 3.4% APY. The brick and mortar banks seem loathe to pay actual interest any more, but the online banks are great.

I am a german citizen who lives parttime in the US and thanks to a SS number I can apply for US credit cards.

I started the hobby in 2013, a big Thanks to Ben.

Ever since I pay all my credit cards 2-3 times a week to a zero balance.

Credit cards is all I have, no other loans, no mortgages etc. and my credit score is always around 820 - 828 thanks to this I guess.

Having Credit cards in the most competitive and customer friendly market in the whole planet is a huge privilege.

I pay the full statement amount on the statement due date and my score ranges between 835 and 850. I don't see much need to do differently

I pay off early and my score is 850/850 even with mortgage and student loan debt. This advice Ben gives really works. Love bragging to my friends

Quick question -

I'm currently a college student looking to build my credit score. I currently have two credit cards - one with a $1500 credit line and the other with a $500 credit line.

Hypothetically, if I spend $1 on each per month, and pay it off early, then would that help build credit really fast? Since it's super-low credit utilization? Or do the banks have a minimum whereby they'd regard anything below a...

Quick question -

I'm currently a college student looking to build my credit score. I currently have two credit cards - one with a $1500 credit line and the other with a $500 credit line.

Hypothetically, if I spend $1 on each per month, and pay it off early, then would that help build credit really fast? Since it's super-low credit utilization? Or do the banks have a minimum whereby they'd regard anything below a certain number (say $5) as irrelevant in determining your credit utilization?

It seems counterintuitive that spending $1 on my credit cards in the short term and sticking to debit cards will help build credit faster, but that's what I'm getting at

This accountant agrees with @neverindoubt. Auto-pay all your bills to keep your credit score up. Last year my 16 year-old car finally died. Bought a replacement the same day because of my excellent credit.

Will a consistently high utilization on a credit card with regular full repayments befor due date help with a credit line increase?

I pay utilities, groceries, gas, insurance, etc from two credit cards, and pay the full balance every 14 days when I get paid. My no-fee credit cards are getting two (some months three) payments in full every month, I pay $0 interest, and my credit score (if I ever need it) is top of the scale. The banks pay me 2 or 3 percent in rewards, so I’m making a few bucks paying my regular...

I pay utilities, groceries, gas, insurance, etc from two credit cards, and pay the full balance every 14 days when I get paid. My no-fee credit cards are getting two (some months three) payments in full every month, I pay $0 interest, and my credit score (if I ever need it) is top of the scale. The banks pay me 2 or 3 percent in rewards, so I’m making a few bucks paying my regular monthly household expenses. Pretty easy to set up, and I basically pay everything with four or five checking debits per month. Takes literally ten minutes with a cuppa twice a week to monitor my accounts for irregularities. Took me about 30 adult years to figure this out, and my money has never been easier to track and manage.

I have lots of credit cards, so I am only borrowing a small percentage of the total credit available. I often have months where I have a very large purchase & I have not noticed that this lowers my credit score. My score is consistently well above 800, so I can't imagine that paying the balances sooner would help my score much at all.

If you are not going to take out a loan anytime soon why do you care if you’re scored drops 20-30 points. If you’re going to open a loan soon than pay them off early if someone is going to pull your credit for a loan. I don’t take out loans so I don’t worry about my score going up and down. Plus with High Savings Accounts offering over 4% interest, I’d rather hold on to my money for as long as possible.

Interesting comments about lost interest of 2-3%

For how many days /month? Minus tax charge on interest?

Having a feeling you can save more with a few less cups of coffee / month!

Personally I pay full balance daily , personal fiscal responsibility, plus I stopped drinking coffee!

“Personally I pay full balance daily , personal fiscal responsibility”

More like obsessive compulsive disorder.

Agree with the other comments, I don't think it is worth the effort because your credit score would not be that much different. Even if you had a lower utilization rate such as using most of your credit line, there is something to be said if you paid off big bills on time. As long as you pay by the due date you're fine. There are many people that have a lower utilization rate and...

Agree with the other comments, I don't think it is worth the effort because your credit score would not be that much different. Even if you had a lower utilization rate such as using most of your credit line, there is something to be said if you paid off big bills on time. As long as you pay by the due date you're fine. There are many people that have a lower utilization rate and much higher bills than you that pay on the due date and do not have a very different credit score. You have many cards each with relatively lower credit lines whereas many others have a different strategy for earning points and miles because they are not doing this as their business and have fewer cards with higher balances. Furthermore, you can setup the auto pay for your accounts.

I basically do just what you do but have just one card report a token balance of $10 which I then pay off as soon as the statement cuts.

This strategy optimized for a high credit score. But it requires a significant amount of liquidity and, in my opinion, overvalues the difference between an excellent and an exceptional credit score. I personally prefer to keep my cash as long as possible in a high yield savings account, and to pay my bill closer to the due date.

When I have to pay my property taxes, I use my credit card to earn points on my hotel loyal program. Next day, I pay off my credit card amount with online checking.

I get more points & maintain good credit score.

Sounds like a lot of effort to game the system for very little gain. The time spent on checking and paying off a dozen cards every week could be used to more enjoyable things in life….

Lots of great comments before mine, so I'll try not to duplicate :) I've moved the most important one to the top and numbered it 0 :)

0. Lenders take a lot of factors into account, and debt to income ratio (D/I) is the most important. Regardless of your high score, if you have insufficient income to satisfy the debt THAT YOU COULD HAVE it will be a red flag. In those cases the easy...

Lots of great comments before mine, so I'll try not to duplicate :) I've moved the most important one to the top and numbered it 0 :)

0. Lenders take a lot of factors into account, and debt to income ratio (D/I) is the most important. Regardless of your high score, if you have insufficient income to satisfy the debt THAT YOU COULD HAVE it will be a red flag. In those cases the easy solution (other than to get a high paying job ;-) is to close some large credit lines, and then your 1% credit utilization will be a higher percentage.

SET UP AS MUCH CREDIT AS YOU CAN BEFORE YOU RETIRE, STOP WORKING, GET FIRED, OR BE LAID OFF!!

1. Paying off cards requires liquid re$ource$, and if you have them, there may be better places to put them than paying off a card. For example, if your card said "transfer a balance over for 0% for 18% after a 3% fee" that works out to 2%/yr, so transfer the balance and then use the liquid re$ource$ in any investment that's of 18mo or less, and makes more than 2%/yr. After 17.9mos pay off the balance. I do this.

2. Cash is king, and your lines of credit may be reduced at any time with and without reason. My HELOC was "paused" for about 6 months during the housing market "valuation reset" following the mass of foreclosures. That meant it still looked like I had lots of credit available... was using little of it... but could only pay into it but not take more out. Nobody can do that to your cash.

3. There are way way way more credit scores than you know. Of course everyone knows about the Big-3 bureaus, and the FICO "score" but they all have **MANY** scores depending on the market. So when you go to get a home loan they look at FICO 2, 4, and 5. For car loans and credit cards 2, 4, 5, 8, and 9.

4. In most of the scores 750+ is considered "Excellent" credit, and the lender then moves to a different evaluation criteria (most of which are covered in the article) such as number of accounts, type, use, ageing, delinquency, chargeoff/collections (those are different to some lenders, equivalent to others), etc.

Thanks for the writeup. If I've contributed anything to the discussion it's that point about having sufficient income to make your D/I attractive. Su trabajo es su credito as the signs at the car lot say ;)

You sound like a day trader and a pump and dump hustler.

For those of you who say Ben's advice is a lot of work for little effort, NO NO NO. He is right. I didn't know this (I always paid my credit cards on time) and one month my credit score dropped by literally 110 points (two cards over 30% utilization plus total utilization over 10%). It took a few months to get it back up. I actually sent this into TPG and got a $200...

For those of you who say Ben's advice is a lot of work for little effort, NO NO NO. He is right. I didn't know this (I always paid my credit cards on time) and one month my credit score dropped by literally 110 points (two cards over 30% utilization plus total utilization over 10%). It took a few months to get it back up. I actually sent this into TPG and got a $200 gift card for his "Reader Mistake Story". A few of the comments (back when TPG had comments and I before I stopped reading the blog) were something like "you idiot, how could you not know this!"

I have no desire to trash my credit rating, even temporarily, for something so easy to avoid. Not sure if the advice is worth $200 to everyone else, but it certainly was to me!

I had the same experience with just one charge on one card 70% utilization, 11% total available utilization, credit score dropped from 838 to 770.

Generally I pay my off every 2 weeks.

Good write up. I've been doing this for years and yeah it definitely helps keep the score way up. Good that you wrote this up as I'm sure many people may not realize.

The banks do have mechanisms to monitor daily utilization. For example, I have a Barclay aviator card that I rarely use and a few months ago I did put a one hundred dollar charge on it. I got an email from...

Good write up. I've been doing this for years and yeah it definitely helps keep the score way up. Good that you wrote this up as I'm sure many people may not realize.

The banks do have mechanisms to monitor daily utilization. For example, I have a Barclay aviator card that I rarely use and a few months ago I did put a one hundred dollar charge on it. I got an email from American Express and I think Chase stating that there was activity on a dormant account. This was the day it posted to my Barclay account. Way before the statement closed. The account was paid off before the statement closed of course, but it was interesting to get that email from them. So they do keep watch even in the middle of a cycle. The point there is that they at least in theory do see the activity so it's not seen as just a dormant account and you are actually using the cards responsibly. Not sure how many banks do this or have the ability to do this. From what I've seen AmEx seems to be almost instantly with anything that hits the credit, even before it's closed off at the statement. Never affected me in any way. Like you, i pay everything off before the date, sometimes except for AmEx charge cards as they don't count for any utilization percentage.

I've tried to educate others on this as well throughout the years. It's a good practice to get into.

I just always pay off my cards on the due date, even using half my limit on one or two my score never drops more than 10 points

US Credit Score

. . . in my eyes, 1 BIG joke!

YES, i do pay off every card, every month on time and sometimes ahead of closing date, but looking at the different scores at the agencies, it is enough proof for me, it's a joke!

FICO has a totally (off by over 90!) compared to TrasUnion.

Citi FICO is so much better, compared to AmEx FICO.

The US system, 1 BIG joke!

. . . to me.

I think you are overthinking this. I pay on the due date and my credit score is fine.

Its not complicated or time consuming at all, it’s funny to hear that because I hear the same “it’s too complicated” argument from people who don’t earn points on spend!

Set up online bill pay for your bank. Load every card on the bank’s bill pay site (you probably always do). Then I look at quicken balances on cards. I enter each one on online bill pay (rounding up the amount to the nearest dollar...

Its not complicated or time consuming at all, it’s funny to hear that because I hear the same “it’s too complicated” argument from people who don’t earn points on spend!

Set up online bill pay for your bank. Load every card on the bank’s bill pay site (you probably always do). Then I look at quicken balances on cards. I enter each one on online bill pay (rounding up the amount to the nearest dollar to keep it fast). Bam! Done in 10 minutes. I do this once per week and I’d way rather do this than spend an hour one day per month doing the whole lot at once.

Not worth it. I pay mine every month on due date and have over 800 credit rating. Difference in 800 and 830 is minimal, if any at all, and I don’t expect to ever get a mortgage or car loan again (wrote a 7 figure check for current house and have paid cash for cars for over 20 years) so frankly a non-event. Ben you can brag about your credit score but mine is just as good for all practical purposes without prepaying

I was shocked when my score dropped 40 points last month a few days after opening a World of Hyatt credit card. I assumed that my score would take a hit of a few points due to the new inquiry….. but 40 points?! The high credit limit on this card should positively impact my utilization, so hopefully those 40 points will come back quickly!

I have fewer cards to manage but 8 I use regularly I have set the closing dates at the end of the month and normally pay off on the 1st without impacting my credit score. This month I had a single $15,000 charge on one card and I will pay it this weekend well before the closing date, as I’ve noticed in the past that one large charge can make a big dent in the score.

Personally monitoring your credit score is only really useful if you are rebuilding or beginning your credit journey, for individuals who aren’t then as long as you pay your statement balance by the due date then the score is a just a number.

Interesting harshness on Ben.

I agree that for many, the difference may not be big, and it's a lot of effort for not much return, but for me, it very much is worth it.

I've simplified by credit cards vastly over the years, and really only hold a few actual credit cards, for perhaps a total of 30K in "credit". This doesn't include my Amex Gold and Plat cards which is where 90% of my...

Interesting harshness on Ben.

I agree that for many, the difference may not be big, and it's a lot of effort for not much return, but for me, it very much is worth it.

I've simplified by credit cards vastly over the years, and really only hold a few actual credit cards, for perhaps a total of 30K in "credit". This doesn't include my Amex Gold and Plat cards which is where 90% of my spend goes. These don't have "credit" limits but still count toward my utilization, making it all the more important to pay them down. There are months I may have 20K on the Amex cards at statement close giving me a 66% utilization.

How is it “worth it”?

This strategy is missing a fundamental point. Credit utilization has no memory. If you have $100K in credit and have an $80K balance reported today and pay it off in full, when the credit bureaus are updated with the zero balance, your score will be recalculated with $0 of $100K. It will NOT remember that you had $80K last month. This, of course, assumes you pay on time, aren't applying for new credit (hard pulls),...

This strategy is missing a fundamental point. Credit utilization has no memory. If you have $100K in credit and have an $80K balance reported today and pay it off in full, when the credit bureaus are updated with the zero balance, your score will be recalculated with $0 of $100K. It will NOT remember that you had $80K last month. This, of course, assumes you pay on time, aren't applying for new credit (hard pulls), etc. Bottom line, paying before the cycle closes only helps if you are applying for credit in the coming weeks. If not, there's a real opportunity cost on your cash. Take it from me, I do this to the tune of 7 figures a year (and no, I am not a "churner").

I could care less about my credit score as long as it is decent ~720 plus etc and I have a big purchase such as a house etc. If they will give me 20K credit then trust me I will use it. What is the point of assigning a credit limit to use only 25 percent. If they give me 0 percent balance transfer to my chucking account I take it all. Use the float...

I could care less about my credit score as long as it is decent ~720 plus etc and I have a big purchase such as a house etc. If they will give me 20K credit then trust me I will use it. What is the point of assigning a credit limit to use only 25 percent. If they give me 0 percent balance transfer to my chucking account I take it all. Use the float to either make investments or even just put it in CDs for interest. Don’t worry about a few points increase in your credit score especially if you are older and acquired most of your big ticket items.

This is way too complicated and time-consuming. Between the husband and I we have 6 open cards, 3 or 4 of which are actively in use each month. They are paid off in full on the due date with an auto-deduct from checking accounts. Because we run up a combined balance of $5-10k each month, with CD rates currently hitting 5%, the interest we would lose by paying off 3 weeks before the due date...

This is way too complicated and time-consuming. Between the husband and I we have 6 open cards, 3 or 4 of which are actively in use each month. They are paid off in full on the due date with an auto-deduct from checking accounts. Because we run up a combined balance of $5-10k each month, with CD rates currently hitting 5%, the interest we would lose by paying off 3 weeks before the due date is about $25/month.

Meanwhile, despite husband being retired and me with a mid-5 figure income, I often pull down a credit score of 850 (and I don't recall last time I saw it below 825). Maybe because neither of us have never not paid off full balance in 30-some years?

People are too fixated by an by a number made up by an authoritarian regime called credit bureau, all of which has suffered data breach.

Yet people's attention are diverted to China, ISIS, or Ukraine.

It's a rigged system because the people allow it and becomes obsess and enslaved with their made up number.

Not that the credit scoring system is a bad thing.

Is this worth doing outside of a time period when you might be applying for a mortgage or car loan? As you saw, drops in credit score due to utilization are quickly reversed by paying off the card in question -- I had a 73 point drop due to a $17k charge that I let appear on the statement close balance, but my score went up 72 points when I paid off the card before the next month's close date. So it's not like there's really a persistent credit score hit here.

This seems like too much work. I just set mines to autopay the day it's due. Still only utilizing 2%. It's not 1% but I don't think the banks care.

Interesting, I never thought about it. I just checked Amex's tool to see what the difference it would make and it said I'd go from 790-805 on VS3.0. Now, that's the same bracket but it is an increase. Maybe I'll worry about the next time I want a card or loan.

There's not really any benefit to having a fico higher than 720 or so (with a few exceptions). With interest rates over 4% you're losing serious risk free interest earning if you pay this early.

This seems so unnecessary. I have a similar number of cards to you and without prepaying balances my utilization hovers around 2% (merely from having a lot of unused credit). Why would I care if my ~825 FICO goes up another 10 points by paying down balances a month early? The opportunity cost of earning investment returns month after month on that liquidity is way too high, especially in a rising rate environment. I cant...

This seems so unnecessary. I have a similar number of cards to you and without prepaying balances my utilization hovers around 2% (merely from having a lot of unused credit). Why would I care if my ~825 FICO goes up another 10 points by paying down balances a month early? The opportunity cost of earning investment returns month after month on that liquidity is way too high, especially in a rising rate environment. I cant imagine theres a single new product you'd get approved for with an 830 FICO that you wouldnt get approved for with an 815 (or any difference in rates), for instance.

@Lucky: Yep, I do the same and so does my college student son. He has now a DL Amex Gold card, an AA MileUp card, Chase Sapphire card, and a Chase SWA Premier card. His FICO score is 820.

If your son had his credit cards auto-paid in full at the earliest scheduled date, his FICO score might drop to 810 or maybe 800, and his life would not be changed at all, except he'd have saved the time he spent OCD paying his credit card balances every week.

Seasoned hobbyists know the drill and aren't we soooo smart. But, newcomers to the game don't know the drill. So, let's cut Ben some slack, think beyond ourselves, and hope a newcomer to the game benefits from the article.

Ben's "advice" here is a lot of work for little/no benefit.

As a ruthless simplifier of my routine, I don't think the effort is worth it unless you know you'll be applying for big installment credit (car, house) soon where the small difference in credit score points *might* make an interest rate difference.

Otherwise, how does a small swing in your credit score due to having a balance affect you? It doesn't.

Just autopay the statement balance at the earliest date you can automatically schedule and...

As a ruthless simplifier of my routine, I don't think the effort is worth it unless you know you'll be applying for big installment credit (car, house) soon where the small difference in credit score points *might* make an interest rate difference.

Otherwise, how does a small swing in your credit score due to having a balance affect you? It doesn't.

Just autopay the statement balance at the earliest date you can automatically schedule and take the time you saved to [insert enjoyable activity here].

I recently noticed that when I wanted to switch my auto and home insurance policies, they said that they will have to run a credit check first, and the premium will be affected by my credit score.

Yes, having an 800 will get you a lower rate than having a 650. Having an 825 wont get you a different score than having an 800. Once your score is above 750, you generally qualify for whatever the best rate offered.

Gonna agree with you here. My credit score is only a few points lower than Ben's, and I have everything on autopay.

I suppose this tactic would be helpful for those who are on the cusp of one rating (very good > excellent).

You are leaving real money on the table, especially in a rising rate environment. If you spend $10K a month (Ben is probably spending much higher than this, given biz spend) and are paying an average of 20 days early, but could instead be earning 3% interest in a bank account (conservative; many offer more than this right now), that's ~$200 per year (12 months*$10,000*3%*20/365). This obviously scales with more spend and the earlier you...

You are leaving real money on the table, especially in a rising rate environment. If you spend $10K a month (Ben is probably spending much higher than this, given biz spend) and are paying an average of 20 days early, but could instead be earning 3% interest in a bank account (conservative; many offer more than this right now), that's ~$200 per year (12 months*$10,000*3%*20/365). This obviously scales with more spend and the earlier you pay.

Unless the credit score impact affects an interest rate on a car/house and you're in the market, this strategy makes no sense.

Completely agree w/ this poster with interest rates rising there's actual $ to be made by NOT doing this.

Also most in this "game" have high scores anyway the couple of extra points don't even matter. I had a medical bill which I'm fighting w/ the medical provider go past due and ultimately in collections (still fighting for being over charged) and the "big" hit to my score was 30 points for non payment...

Completely agree w/ this poster with interest rates rising there's actual $ to be made by NOT doing this.

Also most in this "game" have high scores anyway the couple of extra points don't even matter. I had a medical bill which I'm fighting w/ the medical provider go past due and ultimately in collections (still fighting for being over charged) and the "big" hit to my score was 30 points for non payment - great my score dropped to 810 and what . . . . so unless thre's something major coming up probably not worth it AND you're losing $ in doing so.

@Frank

I think they removed medical bills from the score last year.

You score shouldn't have dropped, or if it did it should jump back up now.

I disagree that the money left on a table is really worth it when you consider that the interest is taxable. Using your example, it's $200 per year -- but assuming a conservative 30% tax rate on that $200, it comes out to $140 (and likely less). I'd rather get the benefits to my credit score and also knowing I have a $0 balance on my credit cards than $140, but realize that math might be different for others.

But there are zero benefits to your credit score unless you are actively shopping a mortgage... Or you just don't have a good grasp on your credit in which case you probably shouldn't be here in the first place. So for your $140 example, you're essentially paying $140 for a bragging right number?

Precisely. I'm doing the exact opposite right now - trying to carry as much as I can on cards offering 0% APR for 12-18 months (even with a 3% service charge) and invest the cash in bonds paying as much as 8% in USD pegged currencies instead. Paying down debt before it's due is the worst thing to do right now especially when there is no direct financial benefit.

An 800+ FICO is an ego booster and nothing more unless you are chasing more credit.

I think this strategy makes a lot more sense to Ben than most other folks, since part of his business is selling credit cards. It's important to demonstrate that having a bunch doesn't wreck your credit score (which some folks still believe). It's a lot easier for Ben to debunk by posting a screenshot his 830 score, than posting a 780 with the disclaimer that he just made a big purchase. If normal readers are...

I think this strategy makes a lot more sense to Ben than most other folks, since part of his business is selling credit cards. It's important to demonstrate that having a bunch doesn't wreck your credit score (which some folks still believe). It's a lot easier for Ben to debunk by posting a screenshot his 830 score, than posting a 780 with the disclaimer that he just made a big purchase. If normal readers are dying to keep their scores up, just pay off early when you've made a big purchase. By definition, you should know when that happens.

I'm curious. The detailed inner workings of the credit scoring algorithms are unknown but based on experience, it seems like a high utilization on a single card can have an impact, not just total usage vs. total available. This is another reason I pay early. Anyone have a similar experience?

It has an impact on your credit score, but unless you're about to take out a big installment loan, how does it have any impact on your *life*?

Yes, I have 61 credit cards and once I spent 90% of credit limit on ONE CARD and my score plunged 100 points. So yes, it's not JUST the total amount of credit you have.

Wow. Weekly! Good info

I’m retired so I only check twice a month (1st & 15th) and then payoff the balances.