In late March we learned the full details of Apple’s new credit card, which was supposed to be launched this summer.

In this post:

Apple Credit Card Now Open To Applications

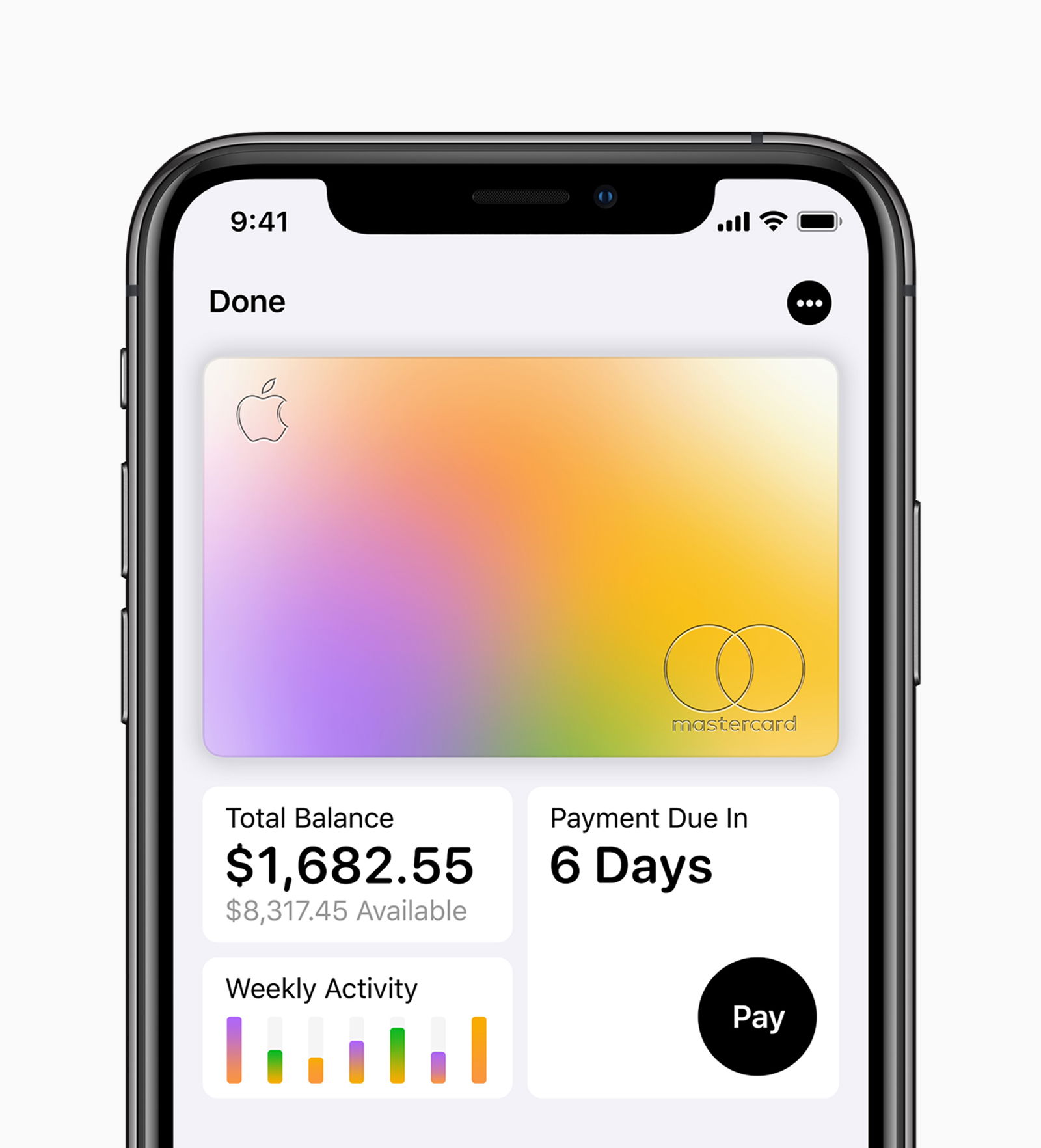

As of today the Apple Credit Card is publicly available in the US. Customers can apply for the card through the Wallet app on iPhone in minutes and start using it right away.

Now, spoiler alert — the card isn’t exactly that exciting, in my opinion. It has a couple of unique features, though primarily it will be popular because Apple has such a loyal following, and people will get anything Apple branded. Apple could start selling fax machines and people would be lining up for days to get their hands on one.

Details Of The New Apple Card

Apple is emphasizing ease of use and privacy as the key features of the card. iPhone users are able to apply directly from their phone, and receive a virtual card number immediately.

Beyond that, Apple is leveraging their data systems to help categorize and label transactions, which they claim will lead to customers living a “healthier financial life” and being better able to understand their spending habits.

Apple Card Rewards Structure

Apple is providing rewards in the form of cashback, which can be earned at the following rates:

- 3% on all purchases made directly with Apple, including at Apple Stores, on the App Store and for Apple services

- 3% cash back on Uber and UberEATS when you use Apple Pay

- 2% when using the Apple Card with Apple Pay

- 1% on physical card purchases made outside of Apple Pay

That’s a decent enough return on Apple and Apple Pay purchases, but there are plenty of rewards cards offering 2% back these days, so the rewards structure of the Apple Card isn’t that interesting to me.

- Earn 3% Cash Back on Dining

- Earn 3% Cash Back at Drugstores

- Earn 1.5% Cash Back On All Other Purchases

- $0

- Earn 5% Cash Back at office supply stores on the first $25k

- Earn 5% Cash Back on internet, cable TV, mobile phones, and landlines on the first $25k

- Car Rental Coverage

- $0

- Earn unlimited 1.5% cash back on all business purchases

- Car Rental Coverage

- Extended Warranty Protection

- $0

- 3% Cash Back at U.S. Supermarkets*

- 3% Cash Back at U.S. gas stations*

- 3% Cash Back on U.S. online retail purchases*

- $0

- 2% cash back on the first $50k then 1% thereafter

- Access to Amex Offers

- No annual fee

- Earn 1% cash back when you make a purchase, earn 1% cash back when you pay for that purchase

- $0

What Makes The Apple Card Different

While the Apple Card seems to fundamentally be a co-branded cashback card, there are a few intriguing differences.

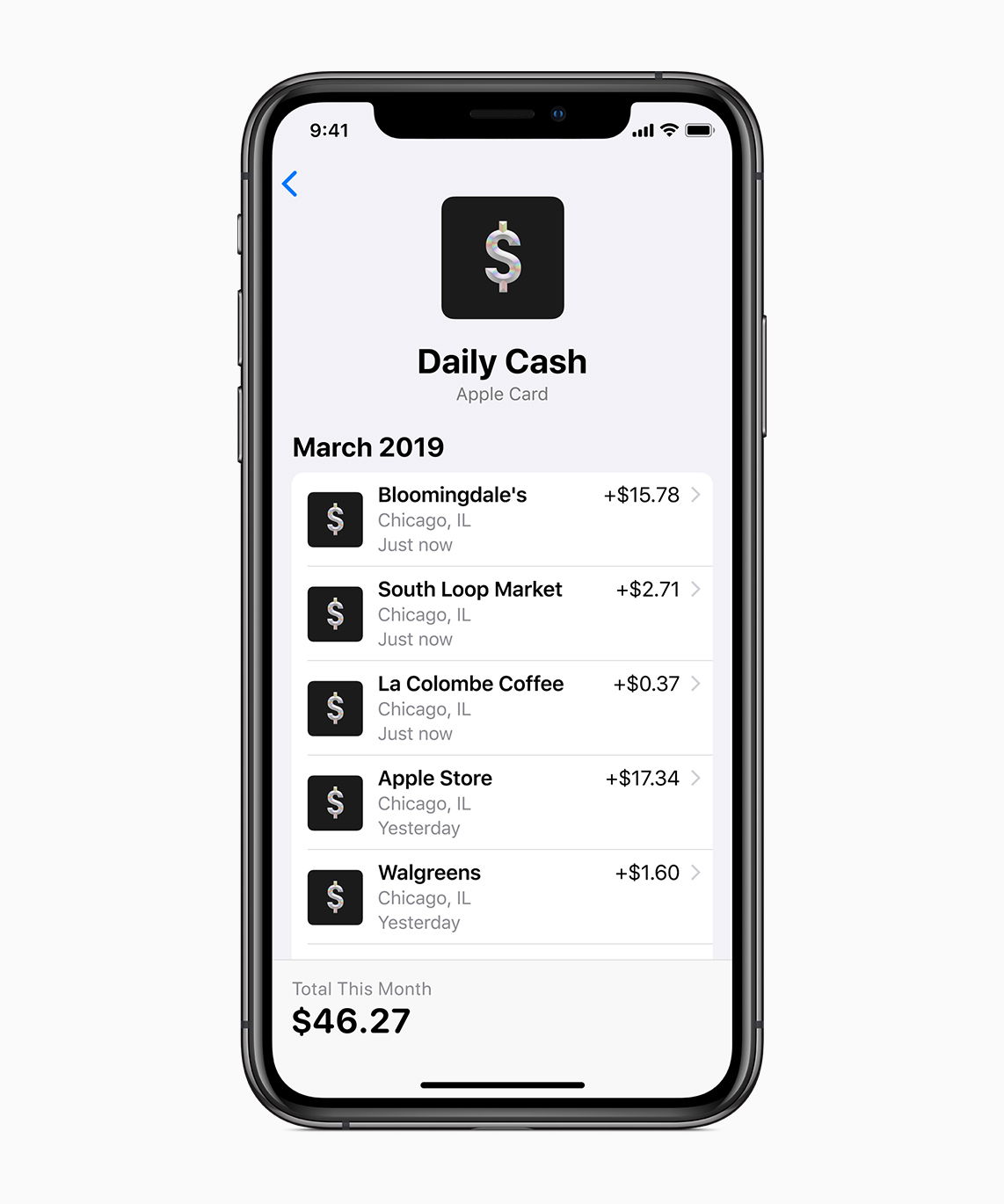

Daily Cash

One of the selling features of the Apple Card is that rewards post relatively “immediately.” This isn’t entirely unique — my Capital One miles usually show up in my account on the same day that I make a purchase — but there are still many issuers and programs that take at least a statement cycle to post.

What is interesting about the Apple Card is that the accumulated “Daily Cash” can not only be used for a statement credit (which is common), but because it is integrated with Apple Pay, cardholders can use their cash rewards for other Apple Pay activities, including sending funds to other iPhone users through Messages.

I’m sure nothing could possibly end poorly with that functionality. 😉

Security, Or Hassle?

The Apple Card is obviously focused on mobile payments, and wants to encourage cardholders to use Apple Pay for all transactions.

For retailers that don’t offer Apple Pay, however, a physical card is still being produced. The card is not just of metal, but “titanium,” and doesn’t have any account details on the card:

With no card number, CVV security code, expiration date or signature on the card, Apple Card is more secure than any other physical credit card.

As someone who seems to have their card data compromised fairly often, I appreciate the idea behind not having any account information on the physical card. From a security perspective, that seems smart.

But this is another feature that I see being potentially problematic in practice, as many cashiers are trained to match the last four digits of the physical card against the swipe-generated data. Still, given the paltry 1% return on purchases made outside of Apple Pay, this isn’t really a card I’d recommend using in those cases anyway.

No Fees

Apple is advertising that the card has no fees associated with it, including no annual fee, no late fees, no foreign transaction fees, and no over-the-limit fees. They say that their goal is also to provide interest rates that are among the lowest in the industry. While some of these are nice perks, no foreign transaction fees is a pretty common benefit nowadays.

My Take On The Apple Card

For someone willing to put a bit of effort into maximizing credit card rewards, I think there’s almost no reason to get this card. There are better cards out there in just about all categories (as I’ll outline below).

That being said, I have to give Apple credit for at least putting some thought into the card with the instant rewards, no late fees, no foreign transaction fees, and more.

If this card were being issued by anyone else, I can’t imagine it would be popular. However, Apple has a massive, loyal following, and I imagine this card will take the US by storm, simply because it’s made by Apple.

But there really isn’t anything unique here. It’s not like there aren’t other cards offering nearly instant rewards, and there are plenty of cards you can apply for directly on your iPhone, and there are lots of cards with no annual fees and even no foreign transaction fees.

Alternatives To The Apple Card

If you’re a savvy consumer, you’ll potentially be earning a lot more rewards with other cards. For one, the card’s 1% cashback on non-Apple/Apple Pay purchases simply isn’t competitive, as cards like the Citi Double Cash® Card offer 1% cash back on every purchase, and then an additional 1% cash back when you pay for those purchases (in the form of ThankYou points). The card has no annual fee, so it is an excellent option.

Otherwise, something like the Uber Visa Card offers 4% back on dining, 3% back on hotels and airfare, 2% back on online purchases, and 1% back on everything else, and has no foreign transaction fees and no annual fee.

Of course, if you’re willing to get more than one credit card and are interested in travel rewards, there’s so much more value to be had. I consider the best credit card duo to be the Chase Sapphire Reserve® Card (review) and Chase Freedom Unlimited® (review)

Apple Credit Card Summary

Apple’s new co-branded credit card is now open to new applicants. The card offers 3% cashback on Apple purchases and Uber, 2% cashback on Apple Pay purchases, and 1% cashback on all other purchases. It’s essentially a way to get you to spend more with Apple, and to increasingly use Apple Pay for purchases.

Then it offers some cool perks like instant rewards, no annual fee, no foreign transaction fees, and a cool card without any numbers on it.

When you consider that this card is being issued by Apple, I imagine it’s going to be very popular.

Is anyone applying for the new Apple Credit Card?

@Rosens222

You're not looking hard enough and don't just follow only from blogs, they push cards that they get commissions.

Other cards that pop up in my mind is Barclays Arrival Plus and the Capital One Venture.

@Rosens222 The PayPal CashBack MasterCard (issued by Synchrony bank) has no annual fee, 2% on everyday spend, and no foreign transaction fee. Others exist as well. The Alliant FCU Visa Signature offers 2.5% on everyday spend with no foreign transaction fees, for $99/year.

I agree with a previous poster. For those who live or spend a lot of time working abroad, there are really zero other options (to my knowledge) that pay 2% on everyday spend without foreign transaction fees.

To all the people who say this is great for iTunes purchases, it’s really not. Costco routinely sells iTunes gift cards for 5 to 15% off. Add in the rewards I get on my card and my executive membership and I come out way ahead of 3% cash back. Perhaps this would be a good card for Apple hardware if it had promotional financing, but I’ve heard nothing about that.

@Daniel

I think Goldman is new to the game and might be extra cautious. Or they just treat credit cards as another type of loan application. Another reason could be that CR do show the difference between primary or AU but Goldman could forget to factor that in their model. Since it affect the score but not your obligation it should be treated differently.

Look for more data points, I'm willing to bet a lot of students will face your issues.

Reasons:

Your debt is too high relative to your income - examples may include loan or credit card balances

Your monthly debt obligations are too high given your income - examples may include credit card, loan, or housing payments

Your monthly debt obligations are too high given your income - examples may include loan or monthly housing payments

Note: I have 0 debt and credit score is well in the 700s.

Funny. I was denied because I'm an authorized user on a United Milageplus Presidential Plus Card where monthly spend is very high and surpasses my income (I'm a student). They don't have a reconsideration line. Never had an issue applying for my Platinum and Sapphire Preferred cards..

For all those who see this card as a bad deal, I also want to mention that the most frequent card I am paid with (in NYC providing professional services) is Amex Platinum, with its one point per dollar spent. Is that a cult too? Most people are simply oblivious or don’t care about how to maximize their rewards. Apple Card is for them, with a technology integration angle. It’s certainly not for savvy maximizers,...

For all those who see this card as a bad deal, I also want to mention that the most frequent card I am paid with (in NYC providing professional services) is Amex Platinum, with its one point per dollar spent. Is that a cult too? Most people are simply oblivious or don’t care about how to maximize their rewards. Apple Card is for them, with a technology integration angle. It’s certainly not for savvy maximizers, and I don’t think it’s trying to be. I’m not real excited about it, but I can see what it’s trying to do, and, as sucker bets go, I’ve seen far worse. Like paying with an Amex Platinum.

@Jeff

LOL, yes there are better alternatives. Don't overpay for Apple cult membership. Try Android, Linux, or USB-C instead.

The card is not worth getting 1 into chase 5/24 rule. That is the bottom line for me.

For those of us well-versed in Quadfecfas/Trifectas and know the value of every point currency, this card is not going to do much for us.

But, what about apple purchases? Apple fanatics aside, many of us have iPhones or MacBooks. We buy new hardware, software, and services from time-to-time. Are any of you considering putting your hardware, AppleCare, iCloud, or AppStore purchases on the new Apple Card?

For one, It’s a no annual fee card....

For those of us well-versed in Quadfecfas/Trifectas and know the value of every point currency, this card is not going to do much for us.

But, what about apple purchases? Apple fanatics aside, many of us have iPhones or MacBooks. We buy new hardware, software, and services from time-to-time. Are any of you considering putting your hardware, AppleCare, iCloud, or AppStore purchases on the new Apple Card?

For one, It’s a no annual fee card. There’s no downside to getting it and not using it much or at all.

Is there a better alternative for apple spend?

Maybe I should get this card just so I can have travel hackers I meet on the road mansplain to me for an hour about miles and points :)

@Jan

I never concluded that banks and consumer interests goes against each other.

But it's not your burden to protect the bank. They have to protect customers because we paid them to do so. You are not liable for unauthorized charges, why give yourself more burden just to save the banks money.

Would you use a credit card if it's a -2% cash back, in other words, you pay the bank 2% every swipe??

@Jan

I never concluded that banks and consumer interests goes against each other.

But it's not your burden to protect the bank. They have to protect customers because we paid them to do so. You are not liable for unauthorized charges, why give yourself more burden just to save the banks money.

Would you use a credit card if it's a -2% cash back, in other words, you pay the bank 2% every swipe??

People like @Stallion or @Srujan Deshpande unknowingly thinks it's a good idea to use a negative cash back card so the banks can make enough money to waive you annual fee. Right?? Because banks want to survive and we want banks to survive, interests goes the same way!!!!!

In reality, go look at Equifax, they screw you over the settlement with FTC, they get paid, lawyers get paid, management still stays, consumers got nothing. Same here, banks will leave you out to die while they save themselves. And not only do you rot and die, you are protecting those banks who left you to die.

@Eskimo

"Your last point is completely wrong. It doesn’t safeguards the interest of end users, it safeguards the interest of the banks."

That might be - but how do you come to the conclusion that protecting the interests of the bank automatically goes against the interests of the consumer? I think they largely overlap to be honest.

This is good news for points and miles hobbyists because a lot more people will be opting for cash back and thus less competition for flight award redemption.

Question. What’s CSR’s award rate for Uber eats? Is it 3x cuz it’s travel/dining? This didn’t occur to me until I started using Uber Eats a lot recently.

@Lars K yes, for the 3% return on Apple purchase (or non bonus spend Apple Pay purchases) is decent. Still, I think some might find more value in timing high value purchases at Apple with a CC signup bonus (minimum spend).

Also, for the heavy iTunes user (such as myself), better deals can be found with discounted iTunes cards via Costco, Amazon, Target, and eBay. With multiple sales through the year these cards can typically...

@Lars K yes, for the 3% return on Apple purchase (or non bonus spend Apple Pay purchases) is decent. Still, I think some might find more value in timing high value purchases at Apple with a CC signup bonus (minimum spend).

Also, for the heavy iTunes user (such as myself), better deals can be found with discounted iTunes cards via Costco, Amazon, Target, and eBay. With multiple sales through the year these cards can typically be picked up for anywhere between 5% - 20% off.

I think it makes sense to get the card solely for Apple purchases. 3% is decent, no other card offers bonus spend on Apple products. For a no fee card, why would you NOT get it for Apple and itunes purchases?

I'm WAY over 5/24 so I went ahead and applied for it just to have as there is no fee. It's through Goldman Sacs. I just had to upload the front and back of my driver's license but I was instantly approved and for a $50,000 credit limit. Just took a few seconds.

I doubt I'll ever use it. Maybe at Apple Store for 3% but even on that I can generally get more benefit...

I'm WAY over 5/24 so I went ahead and applied for it just to have as there is no fee. It's through Goldman Sacs. I just had to upload the front and back of my driver's license but I was instantly approved and for a $50,000 credit limit. Just took a few seconds.

I doubt I'll ever use it. Maybe at Apple Store for 3% but even on that I can generally get more benefit using an Amex Blue card with 2 X Membership Rewards points as I can use it to transfer to programs like Avios when they have 40% bonus and then use it for expensive business/first class flights that far exceed 3% cash back.

Still, I figure it doesn't hurt to have.

Only for suckers.

Replying to @Stallion from before the repost.

I agree up till the last point. Yes, I'm aware some system is better than others. But just like @Srujan Deshpande you also scare the s*** out of me. Another who falls into the thinks they know about credit but they really don’t. You are another victim of Apple’s target group.

Your last point is completely wrong. It doesn't safeguards the interest of end users, it safeguards the interest of the banks.

I'm not sure that there is a value add for the "Apple experience" because in my professional and personal capacity, it is just slightly more attention to customer care as you find in many higher end brands (which Apple is ultimately, a high end brand). I have friends who work at Apple who won't be getting the card because of it's unimpressive rewards. Not sure who would think this is a good idea, and I'm...

I'm not sure that there is a value add for the "Apple experience" because in my professional and personal capacity, it is just slightly more attention to customer care as you find in many higher end brands (which Apple is ultimately, a high end brand). I have friends who work at Apple who won't be getting the card because of it's unimpressive rewards. Not sure who would think this is a good idea, and I'm not sure who even cares how "cool" their credit card looks. With over 50 credit cards in my possession at one time or another, I've never worried about or had problems with security that weren't resolved easily with the major bank the card was issued through.

Ultimately Apple is just doing what they do best, trying to get Apple fanboys (and girls) to buy into a product that integrates into their ecosystem so you use their services so their profits are multiplied with your one credit card usage. It's not better, but enough people are committed to Apple enough they may be tricked into thinking it does something for their lives. And this is coming from someone who uses many Apple products (iPhone, MacBook, etc.) and still think their hardware/software integration is worthwhile, but this credit card integration is just Apple trying to make up some profits from declining iPhone sales.

Readers of this blog are the least likely candidate for this card. It’s easy to forget that we see credit cards through a very different lens than most people.

The rewards on this card are nothing to get excited about, but it’s not the worst product out there for those who use a lot of Apple Pay. (Think of all the people who don’t have a paid Chase card and use a Freedom Unlimited for...

Readers of this blog are the least likely candidate for this card. It’s easy to forget that we see credit cards through a very different lens than most people.

The rewards on this card are nothing to get excited about, but it’s not the worst product out there for those who use a lot of Apple Pay. (Think of all the people who don’t have a paid Chase card and use a Freedom Unlimited for cash back.)

I imagine the value add has to do with how well Apple Card integrated into the phone/Mac/watch ecosystem. It may hit pleasure centers for people who regard credit cards with suspicion, by offering a non-card experience. Instead, it’s (in theory) offering an Apple experience, which I know some of you might scoff at, but I can tell you, in my professional and personal capacity, is a Real Thing that is qualitatively different from other brand experiences.

That, in my mind, the purpose of the minimalist, numberless physical card — it’s not supposed to look or feel like a credit card. It’s supposed to look and feel like a logical extension of your vertically Integrated Apple product life. As product ecosystems go, there’s not much that competes with it.

Disclosure: I’m a Mac consultant who is certified by Apple, but I don’t work for them, and don’t hesitate to recommend competing products when I think it’s in the best interest of my client.

My Apple Card arrived last week (early invite recipient) and the physical card is beautiful! Packaging is also very pleasing in typical Apple fashion. Won’t be using it for anything other than Apple purchases but it’s cool to have a looks nice in my wallet :)

Recession right around the corner, this is just another sign of the peak.

Apple CC, just what we need as consumer CC debt just hit all time highs. I am sure the interest rate will still be 20% plus as the Fed funds rate will be at ZERO next year.

Not sure of the details since I don't plan to get the card, but if you lose your iphone you may have some issues since the card is integrated so tightly with the iphone. I don't think you can pay the card w/o using the iphone (i.e., there isn't a website you can use with a computer).

Anyhow, something to consider and make plans for, if you are the type that misplaces phones.

If it was chip and pin I'd get it for the times in Europe you need to use an unmanned terminal, like purchasing a train ticket. That can be a lifesaver but otherwise I don't see any value.

@Eskimo know what you are talking. What @Srujan Deshpande said is a tried and tested system not only in India and Asian countries but also Europe.

America did not even have the chip implemented until a couple of years back.

That's when we realized the mistake and asked for it.

Even in Europe you need to enter pin when using chip based cards.

We are either to lazy or dump to follow...

@Eskimo know what you are talking. What @Srujan Deshpande said is a tried and tested system not only in India and Asian countries but also Europe.

America did not even have the chip implemented until a couple of years back.

That's when we realized the mistake and asked for it.

Even in Europe you need to enter pin when using chip based cards.

We are either to lazy or dump to follow it and then choose to blame it on others who are doing it the right way to safeguards the interest of end users.

“Stolen Apple/iTunes accounts are some of the most valuable on the black market because of the Apple Pay info stored within them and how easy it is to load on a phone.”

Congrats on dumbest post of the week, AlexS

Well, that’s one ugly credit card.

@AlexS

The ApplePay, Cash, Touch and FaceID security is housed in the secure chip of the iPhone/iPad or Mac, not in the iTunes/Apple account.

"Apple could start selling fax machines and people would be lining up for days to get their hands on one."

Me: I am shocked -- shocked, I say! -- to find fax machines being sold here!

Apple: Your fax machine, sir.

Me: Thank you.

These days, Apple is kind of like Sony. Used to be awesome, but now just another tech company.

The thing is, I’m not aware of any no annual fee credit cards with zero foreign transaction fee outside the US. I travel a lot and I’d welcome a free credit card that helps me avoid these fees but I doubt Apple credit card will be available globally .

@Srujan Deshpande

It's people like you who scare the s*** out of me the most. Those who think they know about credit but they really don't. You are a great example of Apple's target group.

In India you bank is adding you, the customer, more burden and complications to PROTECT THE BANK FROM FRAUD. If your card is illegally used who is responsible, you or your bank?

Think carefully. All those PIN and 2FA...

@Srujan Deshpande

It's people like you who scare the s*** out of me the most. Those who think they know about credit but they really don't. You are a great example of Apple's target group.

In India you bank is adding you, the customer, more burden and complications to PROTECT THE BANK FROM FRAUD. If your card is illegally used who is responsible, you or your bank?

Think carefully. All those PIN and 2FA is does it save your money or your bank's money.

Now for your "personal" bank account, you should have all those security to protect YOUR money.

Not that you can change India's system or anything, but just to remind you to think critically who is the system really protecting at whose expense.

Like I said, Apple is targeting people with no clue, and you are case in point.

So much credit card fraud in a developed country? xD

In India, you have to enter your pin in the pos machine to complete any swipe transaction. Online, a code is texted to your registered phone that you have to enter to finish the purchase.

Sure it adds a couple of seconds, but the added security is much more important. Never suffered credit card fraud in India but a couple of times in the...

So much credit card fraud in a developed country? xD

In India, you have to enter your pin in the pos machine to complete any swipe transaction. Online, a code is texted to your registered phone that you have to enter to finish the purchase.

Sure it adds a couple of seconds, but the added security is much more important. Never suffered credit card fraud in India but a couple of times in the States.

Also we mainly use Google Pay or Paytm for cashless which is easily authenticated by touch ID or a pin.

Safety is the number 1 priority.

When is Apple Pay going to come here?

I second DC's comment - utter rubbish. A card for the up and coming generations who know zilch about credit and interest...

Typical Apple... Release something completely behind the times, have a major marketing blitz, and the sheeple will be lapping it up like it was the best thing ever.

I've had my CC#s stolen many times, but all through merchant breaches, never through abuse of the physical card.

@Quinn: Bullshit. There's nothing new nor novel about this card. There's plenty of credit cards out there which are instant, on-the-spot approval. I believe my Delta...

Typical Apple... Release something completely behind the times, have a major marketing blitz, and the sheeple will be lapping it up like it was the best thing ever.

I've had my CC#s stolen many times, but all through merchant breaches, never through abuse of the physical card.

@Quinn: Bullshit. There's nothing new nor novel about this card. There's plenty of credit cards out there which are instant, on-the-spot approval. I believe my Delta Amex was instant approval, with the final screen showing me the card #, CCV, expiration so I could use it immediately. I had no problem using it online and it worked fine with Samsung Pay, even in places which didn't accept touch-free payments. Apple Pay still requires POS systems and readers be set up to work with it. When one of my Chase cards' # was stolen, it automatically updated in the app, no waiting.

As far as it being secure because it's on the phone, I don't think so. Stolen Apple/iTunes accounts are some of the most valuable on the black market because of the Apple Pay info stored within them and how easy it is to load on a phone.

Indeed, Apply Pay skims a portion of the transaction to Apple. That is probably why you only get 2% only when using Apple pay, but not using the physical card. Personally, Apple pay acceptance did not work very well for me, I use Samsung Pay because I can use the magnetic strip emulation when touch and pay doesn't work.

Apple is skimming all ApplePay purchases by certain percentage, no? Giving bonus spend on the category where company is making independent cash flow (huge one, at that) just reads as yet another Apple “advantage”: make sure customer is permanently locked into our monopoly with big barriers to try anything else. No wonder Apple fanatics are so fanatical... it is new religion of a sort, where questioning Apple-anything is met with “thou are heathen one”.

No annual fee and no foreign transaction fee. That's got to worth something. I am not sure there is any other annual fee-free card that does that.

@ William -- There are several, actually: https://onemileatatime.com/best-travel-credit-cards/no-annual-fee/

OMG

There goes a new credit card debt record. Targeting people who has no clue how the credit system works.

This could be revolutionary, as it is the beginning of the end. RIP US economy.

The brainchild of MBAs in Apple. What to do with $250 billion in CASH, which by the way is more than Portugal's GDP!!!!!!.

Create a credit card and lend some cash out. That way our fanboys can buy...

OMG

There goes a new credit card debt record. Targeting people who has no clue how the credit system works.

This could be revolutionary, as it is the beginning of the end. RIP US economy.

The brainchild of MBAs in Apple. What to do with $250 billion in CASH, which by the way is more than Portugal's GDP!!!!!!.

Create a credit card and lend some cash out. That way our fanboys can buy 2 iPhones and a MacBook Pro instead of just buying a flip phone. In 6 months, we repo the Macs and charge 20% interests while refurb the repo Macs and sell them to the next sucker with less credit.

Capitalism at it's finest.

I'm afraid that your joke on Apple selling fax machines might come to pass. The way Apple is regressing it might come to be.

Brit on the move - it doesn't differentiate Apple, but that doesn't matter. Even within the comments on here you can see people falling for the hype merely because it's Apple.

Is that Apple credit card hosted by capital one, American Express, Chase Bank, or Barclays?

I've been wondering what this card would offer. Not sure that cash back is for me. The data system they mention is not really that innovative - actually, it's lame - lots of cards categorize spending today so their claim of living a “healthier financial life” is silly. I don't get how they think this differentiates Apple. Same for the instant credit of awards, not new. I think this is just Apples attempt to cash...

I've been wondering what this card would offer. Not sure that cash back is for me. The data system they mention is not really that innovative - actually, it's lame - lots of cards categorize spending today so their claim of living a “healthier financial life” is silly. I don't get how they think this differentiates Apple. Same for the instant credit of awards, not new. I think this is just Apples attempt to cash in (pun intended) on the CC industry. After all, they have a huge fan base of loyal customers :)

The real innovation is the mechanism of the credit card. Rather than applying, waiting to get approved and waiting a week or two for the physical card to arrive in the mail, you can start charging to the account immediately, both online and in person.

If you lose your phone, your credit card information is secure since it can't be accessed without biometrics and passwords. Your phone gets remotely wiped. You access your info from...

The real innovation is the mechanism of the credit card. Rather than applying, waiting to get approved and waiting a week or two for the physical card to arrive in the mail, you can start charging to the account immediately, both online and in person.

If you lose your phone, your credit card information is secure since it can't be accessed without biometrics and passwords. Your phone gets remotely wiped. You access your info from another device and all the information is repopulated for immediate use.

If your card number itself is compromised, you can immediately be issued new details.

"Not really" would've been a nice TLDR answer to the page header, but as you said it will probably get plenty of takers anyway, because apple.

So tell me how the Apple/Goldman card is going to help me fly for free?

I don't get it. This is simply a branding hype of Apple and does nothing to help us travel for free.

Pick any Chase /Am-Ex/BofA card that get get me free travel.

So what's the advatange of the App card?

"Apple could start selling fax machines and people would be lining up for days to get their hands on one."

So true! ;)

2x daily spending is good enough for many spending without nick and dime - I mean come on, for many people, miles mostly come from signing up anyway.

And no hidden fees/less hassle to deal with customer service is highly underrated - Hit by it once and you'd appreciate it much more.

Answering your question. Nope. Anyone who would get it either should own stock in Apple or is a certifiable dipshit.

Apple innovating as always, love it! cant wait to get it.

There is a potential danger to this new card, especially for those new to the world of credit. While the lack of late fees should be applauded, it may lull unsuspecting consumers to paying their bill whenever they feel like it, which I suspect will not be protected from having substantial negative impacts to credit scores.

I live in Malta, my home loan bank (Which I get paid into) does not offer Credit cards. Effectively leaving my unable to get a credit card, all banks require income to be paid into them.

If Apple Card is launched in Malta I Would get one as it would be the only option.

They could certainly fill a niche, like Revolut has done for Debit cards.

Junk

What will the current Barclays Apple Visa be converted to?

As someone who lives abroad, no foreign transaction fees + 2% back on ApplePay is a really compelling proposition. Yes, CSR is great for dining out, flights and Ubers, but for day-to-day purchases (like the grocery store, fitness classes and cell phone bills), there's no card offering the same.

Hilton Marriott Avis Hertz etcetc They usually ask me to.present card and they match it with last four digits on reservation. Will be interesting when someone shows this card :-)

Anyone who has an Altitude Reserve and spends more than 3000 annually on mobile transactions comes out ahead of this new offering or any other card offering 2% back. I don't see anything exciting here.

I’ll be curious to see how this impacts the co-branded Barclays card, which while not a great card in terms of rewards, often has promos for 12-18 month no interest financing for Apple store purchases.

It doesn't interest me. I can see how it could be a good card for young people and beginners who don't yet understand how to use credit wisely, but I wonder if those type of customers will even be approved. As for the claim on the Apple website that "Apple Card completely rethinks everything about the credit card," I just don't see it.

@Steven

Third world countries have way more developed world card system than the US, which seems forever stuck in time and prone to fraud.

Hard pass, no bonused spend.

Miss the days when Apple used to do things that were amazing. Another yawn for a company that used to elecit wows.

It’s a hard pass for me. I’m looking to keep my credit available to pick up a more lucrative card in the future. With the double cash card already in my wallet this isn’t compelling.

I wish them the best of luck. We won't apply because the value offered through this card is less than any other card in our wallets.

The security features don't appear to be any better than any other ApplePay system, so I don't value them. Sure, won't be scraping your data, but Goldman surely will.

Eventually, the US will move away from the third-world card system currently in place, and as it becomes more like the civilized world Apple's card will be moot.

You ignored the most important part - the titanium physical card is one of the best looking cards available.

Seems like a decent card option for Apple products, recurring iTunes bills, etc. No real reason not to get it.