The Chase Sapphire Reserve® Card has a $795 annual fee, and after the card’s 2025 refresh, the question of whether it’s still worth it has only gotten more contested — some people find it more valuable than before, others less. The card now carries well over $1,000 in potential credits, but it’s increasingly a “coupon book” of perks, and the gap between the headline value and what you’ll actually capture is the whole decision.

So rather than re-listing every benefit (the full Chase Sapphire Reserve review covers those), this is my honest accounting of how the math actually works for me: which credits I treat as good as cash, which I forfeit, where the lounge access earns its keep, and whether the fee still pencils out once you strip away the perks that sound great but don’t fit my life.

In this post:

My running tally so far on the Sapphire Reserve

Before getting into the individual pieces, here’s where I land on the math on the Chase Sapphire Reserve at the time of writing.

I start by treating the $795 annual fee minus the $300 annual travel credit — which I consider basically good as cash — as the real cost of holding the card. That puts my true out-of-pocket at $495 per year before any other perks. From there, the question is just how much of that $495 I claw back through the credits I actually use.

The reason I put the travel credit in a special category is because it’s a a perk that literally every cardmember should be able to take advantage of (and if you can’t, then you really shouldn’t have the card).

So to do the math on the card over roughly the past year (coinciding with the card’s refresh):

- The annual fee is currently $795

- Then from that I have gotten full value out of the $300 travel credit and the $300 dining credit, and most of the value out of the Apple TV and Apple Music benefit (which I value at maybe half of the $288 retail value), which gets me close to breaking even on the annual fee

- Then I get partial value from some of the other credits, like the hotel credit, the DoorDash credits, and more

- All-in-all, I’m coming out ahead on the card pretty directly, without even factoring in the lounge access or return on spending offered by the card

The headline takeaway: for me, the travel credit, the dining credit, and the Apple Music subscription, get me to roughly breakeven on the fee, with the other credits, lounge access, and rewards structure, as the icing on the cake.

Link: Learn more about the Chase Sapphire Reserve® Card

A solid welcome offer

The Chase Sapphire Reserve is offering a welcome bonus of 100,000 Ultimate Rewards points after spending $6,000 within the first three months. This is a very good welcome offe. I value Ultimate Rewards points at 1.7 cents each, so to me those points are worth $1,700 — a nice incentive to pick up the card.

One eligibility note worth understanding: under the current rules, the card essentially follows a “once in a lifetime” rule for the bonus. You likely won’t be eligible if you currently have the card or have had it in the past. However, eligibility (including for the bonus) is unrelated to whether you have or have had the Chase Sapphire Preferred® Card (application) or the Sapphire Reserve for Business℠ (application). Chase’s application pop-up should tell you if you’re not eligible for the bonus before there’s a hard pull on your credit.

I’ve had this card for many years, so unfortunately I don’t have much recent firsthand experience to share with getting approved, earning the welcome bonus, etc. However, there are lots of amazing uses of Chase points, so it should be easy to get outsized value with those.

The rewards structure: what I actually factor into the math

The Chase Sapphire Reserve has a lucrative earning structure on paper, but I’m honest with myself about which categories I actually value:

- 8x points on Chase Travel℠ bookings is industry-leading on paper (a 13.6% return by my valuation), but it comes with opportunity costs from booking through the portal, so I don’t really factor this into my overall valuation of the card; still, I do sometimes decide to book travel through the portal, I just don’t factor it into the valuation

- 4x points on direct airline and hotel bookings is great, and this is my go-to card for hotels, which is a big spending category for me; however, for airfare I generally use the American Express Platinum Card® (application)

- 3x points on dining continues to be a great bonus category that many people value; however, for dining I generally use the American Express® Gold Card (application)

- 5x points on Lyft rides (valid through September 30, 2027) is the equivalent of an 8.5% return on rideshare spending, and that’s useful, as I use Lyft all the time

The card also has no foreign transaction fees, and since a large percentage of my purchases abroad are dining, hotels, and airfare, I can avoid the fees while maximizing points — the best of both worlds.

Over the past year, a vast majority of my spending on this card has been for direct hotel bookings, where I earn 4x points. That’s among the best return on hotel spending on any card, and I spend quite a bit on hotels. With dining and airfare I have other cards with a better rewards structure, though I also do value the bonus points with Lyft (it’s just not as big of a spending category for me as hotels).

The credits, ranked by how much I actually value them

This is the heart of the “worth it” question. The Chase Sapphire Reserve potentially offers well over $1,000 in credits, but like so many cards nowadays, there are hoops to jump through, so I wouldn’t value them anywhere near the headline number. Here’s how each actually nets out for me, ranked from “good as cash” to “I’ll forfeit it.”

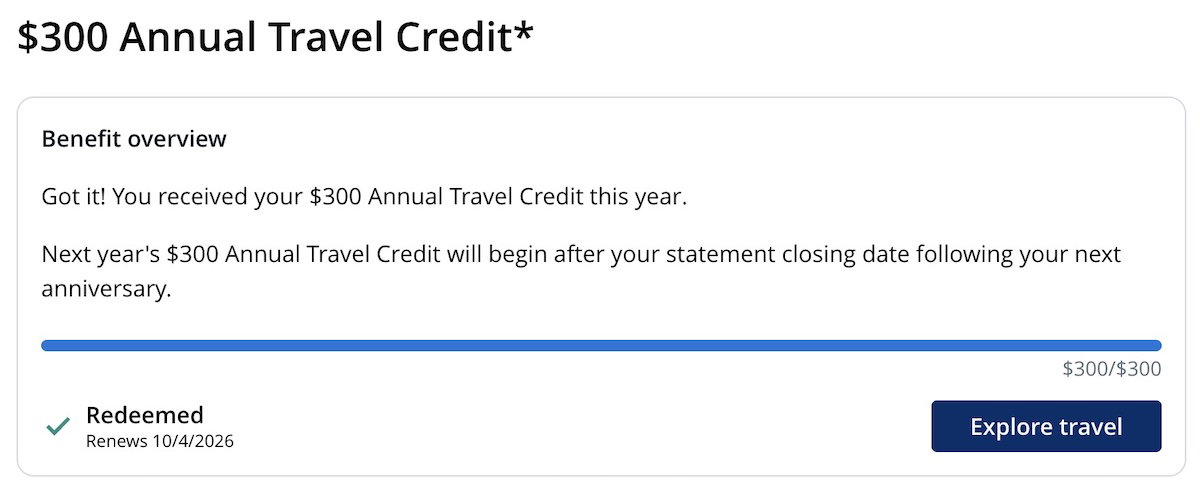

1. The up to $300 annual travel credit (good as cash)

The Chase Sapphire Reserve offers up to $300 in annual travel credits, and it’s one benefit that all cardmembers should be able to max out. There’s no registration required, and any purchase coded as travel — flights, rideshares, taxis, train tickets, hotels, and more — is reimbursed automatically, across as many transactions as needed. It’s based on the anniversary year rather than the calendar year.

I’d imagine virtually every cardmember spends at least $300 per year on travel, so I treat this as lowering the card’s real out-of-pocket to $495. And if you don’t spend at least $300 per year on some sort of travel purchase, then I really don’t think this card is for you.

I’ve had good experience with this benefit working exactly as advertised — the credits post almost immediately, in my experience, and it’s truly an effortless credit that I don’t even have to think about.

2. The up to $300 annual dining credit (close to face value for me)

The Chase Sapphire Reserve offers up to $300 in annual dining credits, and it’s also a perk that is relatively easy to use, at least if you live in a relatively large city.

This is a semi-annual credit — a $150 credit in January through June, and a $150 credit in July through December — valid at a limited number of restaurants in major cities. The list is admittedly quite small, with just hundreds of participating restaurants across the country.

The good news for me is that some restaurants in Miami that I frequent are on the list, so I get full value out of this with just two meals per year. Others will probably struggle to maximize it. For example, in Miami I enjoy restaurants like Nami Nori and Phuc Yea, both of which are on the list. The lists are pretty solid for major cities, though admittedly for smaller markets, it gets trickier.

3. The Apple TV and Apple Music benefit (real savings if you’d pay for it anyway)

Chase Sapphire Reserve cardmembers can receive a complimentary subscription to Apple TV and Apple Music through June 22, 2027, a value of up to $288 per year. I have an Apple Music subscription, so getting that for free saves me a substantial amount of money — which is exactly the test for any “subscription” credit: it’s only worth face value if you’d otherwise be paying for it.

4. The up to $500 hotel credit with The Edit (I don’t factor it in)

The Chase Sapphire Reserve offers up to $500 in annual hotel credits, and it’s a semi-annual $250 credit, valid only for bookings of a minimum two-night stay at The Edit by Chase Travel hotels, using the “pay now” feature. I don’t place much value on it — many hotels in the portfolio are quite expensive, and the two-night minimum constraint is limiting.

To be clear, that’s not to say that I won’t use this perk, but the minimum stay causes me not to consider it to be worth face value. For example, I used the $250 credit last year for a two-night stay, while I haven’t used it so far for the first half of the year, and I suspect I won’t be able to, based on my current travel plans.

5. The up to $300 DoorDash credit (too fragmented to value)

On top of a complimentary DashPass membership (a value of up to $120 per year if you activate by December 31, 2027), the Chase Sapphire Reserve offers up to $300 in annual DoorDash credits. However, it comes in the form of up to $25 in monthly credits, broken into a $5 monthly promo credit for restaurant orders and two $10 promo credits for groceries, retail, and more. The increments are small enough that I don’t factor them into the math, even though I try to use them.

I don’t ever order groceries through DoorDash, so I don’t take advantage of the $20 out of $25 worth of monthly credits. I do use the $5 restaurant credit every month, but I also have a hard time placing too much value on that, since that’s truly the definition of a “coupon book” benefit.

6. The up to $300 Stubhub & viagogo credit (not for me)

The Chase Sapphire Reserve offers up to $300 in annual Stubhub and viagogo credits. This is a semi-annual credit ($150 in each half of the year), valid for concert and event tickets with Stubhub and viagogo, currently through December 31, 2027.

I don’t really like concerts and events, so this one isn’t of much value to me — but it’s a clean example of a credit that’s either worth full face value or essentially zero, depending entirely on whether it fits your life. I’ve fully forfeited this benefit, and ultimately I’m fine with that.

Other credits worth a mention

Let me share a few more Chase Sapphire Reserve credits and benefits that round out the card, without changing my core math.

First, there’s the up to $250 one-time Chase Travel Hotels credit (valid through December 31, 2026, for two-night prepaid bookings with IHG, Montage, Pendry, Omni, Virgin, Minor, and Pan Pacific). It’s niche, so I won’t factor it in, even though it might come in handy.

Next, there’s the up to $120 annual Lyft credit ($10 monthly, through September 30, 2027). That’s also something I use, but not necessarily something I factor into the math, given the small increments, and the number of rideshare promotions that are out there.

Then there’s the Global Entry, NEXUS, or TSA PreCheck credit once every four years. I do find this to be useful over time, as I can always use these credits for friends and family, worst case scenario, as long as I remember to pay with my card.

Then there are the $75,000 annual spending bonus benefits, which include IHG One Rewards Diamond status, Southwest Rapid Rewards A-List status, a $500 Southwest credit, and a $250 Shops at Chase credit.

I think the $75,000 spending amount could be worth chasing if you’d get value from these perks. Personally, I haven’t passed that threshold, and I don’t think I’ll do so this year either. However, if you can largely spend in categories eligible for bonus points, then the math could work out pretty nicely.

Lounge access: where the card actually differentiates itself

Lounge access is the piece I’d push back on anyone who calls this “just another coupon-book card.” Here’s how I think about the lounge access perks on the Chase Sapphire Reserve:

- The Priority Pass™ Select membership (with two guests) is nice, but lots of cards offer it, so it’s hardly a differentiator nowadays

- The real value is Chase Sapphire Lounge access and Air Canada Lounge access, which are unique to this card — Sapphire Reserve cardmembers get unlimited Sapphire Lounge visits with two guests, and there’s no other US-issued card that offers Air Canada Lounge access

- The value of all this varies greatly based on your home airport and travel patterns

If you ask me, Chase Sapphire Lounges are exceptional, and are a major incentive to have this card. I really think the network has elevated credit card lounges in the United States, and I particularly love the design of the lounges, the food (including a la carte and individually plated dishes), great coffee, and more. I pass through airports with Chase Sapphire Lounges enough that I really value this.

Where the math breaks down: credit card fatigue

My biggest hesitation with the Chase Sapphire Reserve isn’t any single credit — it’s the cumulative effort. I’m generally not a fan of the “coupon book” model of justifying annual fees, and the Sapphire Reserve leans hard into it.

Between the travel credit, dining credit, hotel credit, DoorDash credits, Stubhub credits, Lyft credit, and the Apple subscriptions, you’re tracking a lot of moving pieces across different apps and enrollment dates just to break even.

Most of these annual fees can be justified with some effort — but “with some effort” is doing a lot of work in that sentence, and credit card fatigue is real when you’re trying to maximize several premium cards at once.

The travel credit is the easy part, it’s everything else that takes effort, or either requires a certain conusmer profile. That’s where the math can potentially break down, as I see it.

Is the Chase Sapphire Reserve worth it for me right now?

For me, yes — but it’s closer than the headline numbers suggest, and the reason is specific. Between the $300 travel credit (good as cash), the $300 dining credit (close to face value, thanks to the Miami restaurants on the list), and the Apple Music subscription (which I maybe value at $150), I’m basically at breakeven on the annual fee before counting anything else. The lounge access and rewards structure are then the icing on the cake.

Let me be clear, though — that’s the math for me, and only for me. The card is a “yes” if:

- You’ll use the $300 travel credit (almost everyone will) and at least one or two of the harder credits actually fit your life — a dining-credit restaurant near you, an Apple subscription you already pay for, etc.

- Your home airport or travel pattern gives real value to Chase Sapphire Lounge or Air Canada Lounge access

- You spend meaningfully in the bonus categories — particularly direct hotel and airfare bookings

- You’re not already stretched thin maximizing several premium cards (the fatigue factor is real)

For me, renewing this card under the current set of benefits is a no-brainer, and that will continue to be the case until something meaningfully changes. Now, ideally we’d actually see a Chase Sapphire Lounge at my home airport some time soon (it has been rumored), which would make the value of this even better.

If the math doesn’t work: the best alternatives

If you’ve had the Chase Sapphire Reserve and no longer find it worthwhile, the key thing is to keep one card that unlocks the full Ultimate Rewards ecosystem (transfers to airline and hotel partners). That brings us to two options…

Downgrade to the Chase Sapphire Preferred

You can downgrade to the $95 annual fee Chase Sapphire Preferred, which still offers 3x points on dining, adds 2x points on all travel (so it’s better for non-hotel, non-airfare travel), offers an up to $100 annual hotel credit, and keeps great travel protection.

You’d give up the incremental Priority Pass membership (not a big deal for many), Sapphire Lounge and Air Canada Lounge access (a big deal to some), the 4x direct airfare/hotel earning, and the credits. It’s a considerably lower-cost way to stay in the Ultimate Rewards ecosystem.

Cancel and focus on the Chase Ink Business Preferred

The $95 annual fee Ink Business Preferred (application) has a massive welcome offer and awards 3x points on the first $150,000 of combined purchases per cardmember year on travel, shipping, internet, cable, phone services, and advertising with social media sites and search engines. It offers the same 3x on travel, making it the best Chase card for non-airfare, non-hotel travel (though with a cap). The important distinction: it’s a business card, so the spending you put on it should reflect that.

And whether or not you keep the Reserve, it pairs beautifully with the no-annual-fee Chase Freedom Unlimited® (application), which offers 1.5x points on everything, pooled into Ultimate Rewards — one of the best duos out there.

Bottom line

The Chase Sapphire Reserve is a premium rewards card with a high annual fee and very strong perks. While there’s understandably hesitation around the $795 annual fee, for many consumers the math will work — but only if you do the honest accounting rather than trusting the headline credit total.

I’m generally not a fan of the coupon-book model, but between the $300 travel credit, the $300 dining credit, and the Apple TV and Apple Music subscription, that’s basically breakeven on the fee for me — before accounting for the rest of the credits, the rewards structure, and the genuinely unique lounge access. My biggest hesitation isn’t any single number. Instead, it’s credit card fatigue, and the effort of maximizing several premium cards at once.

For those who can’t make the math work, the Chase Sapphire Preferred (lower fee, 3x points on dining, 2x points on travel) or, if you can shift spending to a business card, the Ink Business Preferred, are the most compelling ways to stay in the Ultimate Rewards ecosystem for less.

How are you feeling about the value proposition of the Chase Sapphire Reserve? Can you make the math work, or how has your strategy evolved? Which credits do you actually capture, and which do you forfeit?

I used to love the 1.5x spend on Chase Travel. But now they have this point boost system I frankly don't understand. Do you think Chase Reserve travel point boost system is worth it? Do any other Chase cards have point boost booking?

I have CSR, Amex Plat and UA Club card, so lots of fees to get some value out of each program.

The CSR is withering in my view. The UA Club card also shares many features that the CSR offers. The Amex Plat has Priority Pass, which I do like and use around the world. I've never seen a Chase lounge (EWR based) so don't really care. Use United/Star clubs in most places if I...

I have CSR, Amex Plat and UA Club card, so lots of fees to get some value out of each program.

The CSR is withering in my view. The UA Club card also shares many features that the CSR offers. The Amex Plat has Priority Pass, which I do like and use around the world. I've never seen a Chase lounge (EWR based) so don't really care. Use United/Star clubs in most places if I actually have time to go to a club or there's one in the terminal I'm using. Never seen a Centurion club either, although they are threatening to open on in EWR Terminal A, but will believe it when I see it.

Both the Amex Plat and CSR are a chore to maximize "value" at these fee levels. And they do feel somewhat redundant to me. The "dining" programs I find generally useless as well, as they are heavily giant city centric, which limits real world value. Unless you're in a huge city, good luck using either dining program.

Basically, if you're a regular suburban half business half leisure traveler, and don't live in NYC or near a Delta hub, then Amex plat is challenging, and CSR is mostly useless.

You did not mention the car rental Insurance or the travel delay and cancelation insurance. I cruise twice yearly. I do not purchase the insurance offered by the cruise lines. The coverage cost savings is at least $700.00!

Dropped CSR last year as the new coupon book model was a fight to break even without adapting my life to fit the card, which is the antithesis of what it should be. I was a proud evangelist since day 1, but with the changes, I've moved to United Quest and CSP that fit my life (and home airport) better. No frustration with CSR, but Chase made it clear that the card wasn't for me.

FWIW my husband got the Chase reserve when it first came out many years ago. He just got approved again, but Chase reached out to him and he had to call in, although it seemed mostly an identity verification issue.

You don't mention the annual fee for additional users which is steep. I agree that the coupon book in unappealing and only works if you use what's on the list.

Chase could make it a bit more flexible. As far as coupon books go, although I am not a fan Amex's is a bit more flexible. The Amex Marriott card offers a $300 restaurant credit divided monthly but any restaurant is acceptable. The Apple money could be a news and digitial subscription for example.

I definitely get the value back and then some on this card but agree it can be cumbersome at times. Another benefit I use a lot is the ability to be able to transfer points directly to both Flying Blue and Qatar, especially at times when there is a decent bonus. I do this a lot to take advantage of booking their business class award travel 350 days out when the best availability and best...

I definitely get the value back and then some on this card but agree it can be cumbersome at times. Another benefit I use a lot is the ability to be able to transfer points directly to both Flying Blue and Qatar, especially at times when there is a decent bonus. I do this a lot to take advantage of booking their business class award travel 350 days out when the best availability and best value is there as I use both airlines for select trips at the same time of year repeatedly!

This week I used the $300 travel credit, $250 IHG credit, $250 Edit credit and $150 dining credit. I earned the 150,000-point bonus earlier this month. That will get me 12 nights @HR Bangkok which is worth $2400 to $2600. Great card for me.

@Ben, I think you should discount the $300 travel credit value to account for the zero points. Non-bonused travel = 300 points ($4.5). Airfare/hotel = 900 ($13.5). Travel portal = 2400 ($36).

Chase could easily change this so that you earn full points, since they do so on all the other purchases that get offset by the new credits (Stubhub, dining, etc.).

Oops. Forgot they increased direct airfare and hotel, so it's 1200 points ($18).

I have to say that the card barely makes sense when accounting for the AF. The Platinum offers so much more value for the annual fee. The edit would be better if it didn't require a 2-night reservation, like it does with the Platinum FHR. I'll probably get rid of this card next annual fee, its very underwhelming

@Lucky are there portions of this post that are generated?

I agree that a great summary for this card is "fatigue". If I'm paying $800, they should be working for me, not making me have to sit down and do the math to claim $5 here and there.

The prestige used to have a feature where if you found a lower price on something they would refund you the difference. That was a great value add to the fee.

I also agree with the...

I agree that a great summary for this card is "fatigue". If I'm paying $800, they should be working for me, not making me have to sit down and do the math to claim $5 here and there.

The prestige used to have a feature where if you found a lower price on something they would refund you the difference. That was a great value add to the fee.

I also agree with the comment that rental insurance is valuable for many and shouldn't be discounted.

I kept it this year because the timing of the change meant I could double dip on the dining and stubhub credit, but I think it's my last year.

I'm about the same as you for now. We have plenty of restaurants in San Diego and where I typically travel. I've managed to use The Edit 3 times for some pretty nice stays. There is also a Chase lounge at SAN and other airports I use frequently.

That being said, it's a bit of a PIA to use the coupons and it will be on the chopping block each year whether to keep or quit. It's not a "no brainer" any longer.

You mentioned that the CSR has no foreign transaction fees, which is obviously a great feature of the card. Still, how do different banks like Chase, AMEX, etc., treat currency conversions? Is there an industry standard? Have you ever addressed this in an article?

You left out the car rental insurance coverage. Primary coverage. That has value more than DoorDash and similar benefits of meager value.

I would strictly want this card for the sign-up bonus. Other than Air Canada and Singapore Air, I don't value the transfer partners enough to accumulate Ultimate Rewards points through spend. Citi, American Express, and Capital One have better airline transfer partners. As for the annual fee, I could justify the travel credit easiest. I would use the Stubhub credit, but not at face value. Mostly resale tickets are sold there, usually at inflated prices....

I would strictly want this card for the sign-up bonus. Other than Air Canada and Singapore Air, I don't value the transfer partners enough to accumulate Ultimate Rewards points through spend. Citi, American Express, and Capital One have better airline transfer partners. As for the annual fee, I could justify the travel credit easiest. I would use the Stubhub credit, but not at face value. Mostly resale tickets are sold there, usually at inflated prices. Maybe 60-75% of face value. I get Apple TV discounts through T-Mobile, so Chase would only save me $3 per month. Overall, it would be a challenge to break even on the annual fee; a challenge that I wouldn't want to take.

I will probably get this card for the sign-up bonus. Doubtful this would find a place in my wallet for the long term.

FYI, the Edit credits are not semi-annual anymore. You can use the credits whenever you want--twice in the first half of the year, twice in the second half, or once per half.

thank you, was about to say this

interesting that you didnt even mention the best perk it offers: points boost on luxury hotels. Yes they have nerfed to mostly 1.65cpp which sucks, but being able to burn points at 1.65-2.0cpp on luxury hotels like St Regis/Capella/Four Seasons/etc. is incredible. Literally no other card offers this at more than 1.0cpp. It's an absolute game changer. I get why you specifically don't use it since you book via Ford, but to not mention it in your review is a miss IMO

That is definitely the best CSR perk if you earn a lot of UR across Chase cards as compared to other travel cards- so long as the price is reasonably comparable to other booking channels (after factoring in the value of any benefits/perks), it's definitely the best card if you want to redeem for high-end hotels but would not pay actual cash for those stays (since FHR is only 1 CPP).

Greedy high fees .

Sure, a person can garner $X of the card's credits, but how much of a hassle does it take to do so? Of course, snag the SUB. But, the hassle factor makes it hard to justify as a keeper. And, there are better earn rates for spending. As for its "best in class" travel protections, skilled hobbyists can find close-enough alternatives.

I'm struggling with this one. I also have the Amex Gold and Platinum cards so, like Lucky, I don't value the dining or airfare bonuses on the CSR. Also, I find the Edit credit much less valuable than Amex's FHR credit (which I use every year). I'm probably about breakeven as well or maybe a litte up but also spend $3000-$3500 a year in AFs across almost 20 cards (some no AF and 3-4 more...

I'm struggling with this one. I also have the Amex Gold and Platinum cards so, like Lucky, I don't value the dining or airfare bonuses on the CSR. Also, I find the Edit credit much less valuable than Amex's FHR credit (which I use every year). I'm probably about breakeven as well or maybe a litte up but also spend $3000-$3500 a year in AFs across almost 20 cards (some no AF and 3-4 more premium cards). Also, looking at Bilt Paladium coupled with a downgrade of CSR to CSP but have another 2 months to decide. Right now may keep another year but will definitely be a year to year decision unlike my Amex Platinum which will likely be a keeper until I'm gone.

End of the day - still making my annual fee back, but boy has this card gotten annoying. If you don't value CSR lounges (and I do because the LGA one is great AND it has the best guest policies that work for families) drop the card ASAP.

It's amazing to me that a card that used to market itself as a 3x travel card 1) still has a $300 travel credit - the whole...

End of the day - still making my annual fee back, but boy has this card gotten annoying. If you don't value CSR lounges (and I do because the LGA one is great AND it has the best guest policies that work for families) drop the card ASAP.

It's amazing to me that a card that used to market itself as a 3x travel card 1) still has a $300 travel credit - the whole point of which was to get people to use this card for all things travel because of the former 3x category and 2) has a terrible, terrible program like The Edit which is leaps and bounds worse than FHR with wildly inflated pricing.

I don't think 8x is industry leading when Strata Elite is 12x hotels / 6x air. The idea that you wouldn't book direct on an airline booking with Amex Plat 5x and book through Chase because you may get an extra 3x points... hotels I'm more than willing to book through portals (usually so many hotels if something goes wrong), flights are a completely different story.

I hear you on stubhub with young kids and such, but you get $150 2x a year. I understand you can now pay with Paze with Stubhub - register your Chase cards with Paze (through the digital wallet on the Chase app) and that's an extra 10x Chase miles through 12/31. And stack it with a portal - Rove just had 9x, Rakuten is at 10x once a month. That's ~20x miles or 6,000 miles - throw the tickets away, who cares. At 1.5cpp that's $90 in value for doing absolutely nothing, which I think therefore is a fair value for this credit.

Isn’t the Edit credit now just 2x per year but at any time (not semiannual)?

yes

Very much on the fence about renewing. As Ben says, the $300 travel credit is a no brainer. I’ve also managed to use the Edit & IHG hotel credits this year but not sure I would in the future. Sapphire lounges are really nice by U.S. standards, but I find they over promise and under deliver. They used to offer free flowing champagne but the last few visits it’s always been out of stock. And...

Very much on the fence about renewing. As Ben says, the $300 travel credit is a no brainer. I’ve also managed to use the Edit & IHG hotel credits this year but not sure I would in the future. Sapphire lounges are really nice by U.S. standards, but I find they over promise and under deliver. They used to offer free flowing champagne but the last few visits it’s always been out of stock. And there’s always a wait to get in & very crowded once you do make it in.

Don’t forget the $120/yr ($10/mo) Peloton credit!