The Chase Sapphire Reserve® Card (review) is one of the most popular premium rewards cards. While the card has a steep $795 annual fee, it also offers a variety of benefits that can help offset that, ranging from lounge access to credits.

In this post, I’d like to focus specifically on the Chase Sapphire Reserve dining credit, which can get cardmembers up to $300 in value annually. I know this tends to cause some confusion, and there’s some nuance to redeeming this, unlike the Chase Sapphire Reserve travel credit, which is basically good as cash.

Link: Learn more about the Chase Sapphire Reserve® Card

In this post:

How to use Chase Sapphire Reserve dining credit

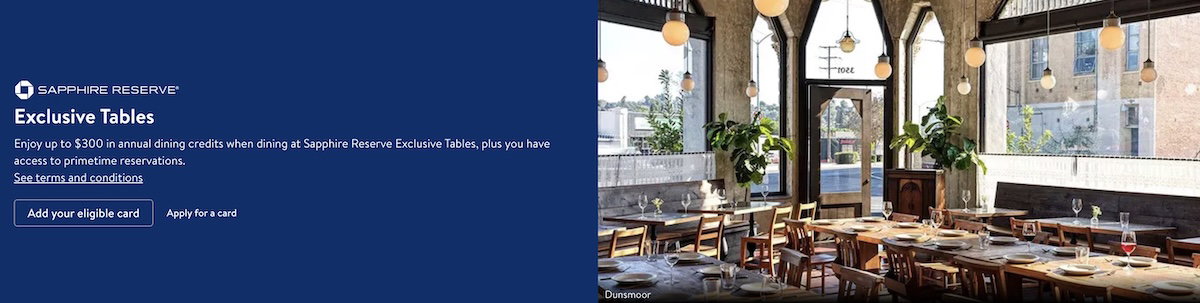

The Chase Sapphire Reserve offers up to $300 in dining credits annually, with the following basic terms to be aware of:

- The card offers an up to $150 statement credit semi-annually, once in January through June, and once in July through December

- The credit can be used across one or multiple purchases, until the $150 limit is reached

- The credit automatically posts for dining purchases at select restaurants, up to the maximum, with no registration required

- To qualify, the eligible card must be used for the dining purchase, though it doesn’t matter how you booked your reservation

- Certain types of purchases may not be identifiable and will not qualify, like delivery and takeout, merchandise and gift cards, purchases made through digital wallets, etc.

- Statement credits should post to billing statements within three business days, but may take up to four weeks

Participating Chase dining credit restaurants

Many people may wonder at which restaurants the Chase Sapphire Reserve $300 dining credit can be used. This has actually been simplified a bit since this benefit was launched. Long story short, the credit can be applied to any restaurant belonging to Sapphire Reserve Exclusive Tables, and you can find that portal here. These are also restaurants at which cardmembers can get priority reservations.

You’ll find that there are hundreds of restaurants across dozens of cities that are participating. The list remains subject to change, so I won’t fully list them here, but this includes restaurants in Atlanta, Austin, Baltimore, Boston, Charleston, Charlotte, Chicago, Dallas, Denver, Detroit, Hawaii, Houston, Las Vegas, Los Angeles, Miami, Milwaukee, Minneapolis, Nashville, New Orleans, New York, Philadelphia, Phoenix, Portland, San Antonio, San Diego, San Francisco, Seattle, and Washington DC, among other cities.

This list really has grown very nicely, especially outside of the country’s few biggest metropolitan markets.

Chase Sapphire Reserve dining credit value

Nowadays premium cards largely have high annual fees, and it’s possible to get outsized value, but it can take some effort. With that in mind, the Chase Sapphire Reserve dining credit is probably pretty polarizing for cardmembers. As is often the case, the perks of this card favor those who live in major cities.

For me, this dining credit is basically good as cash. I live in Miami, and there are a couple restaurants on the list that I frequent. So I’ll easily get $300 of value out of that per year.

That being said, of course others will feel differently. If you wouldn’t otherwise visit the restaurants on the list, then that’s a major value that you’re not going to get out of the card. Admittedly premium credit cards with a variety of statement credits are designed for there to be breakage, so you don’t need to get full value out of every benefit for a card to make sense.

Chase Sapphire Reserve dining credit FAQs

Bottom line

With the Chase Sapphire Reserve dining credit, you can get up to $300 of value per year, with a credit of up to $150 every six months. This is available at a limited number of restaurants in select cities, though the list is becoming more substantial over time, including in some smaller cities. If you’d otherwise frequent these restaurants, then this is awesome, and basically good as cash. Meanwhile if you wouldn’t frequent any restaurants on the list, it’s a different story.

What do you make of the Chase Sapphire Reserve $300 dining credit?

This and the last sapphire article nailed a decision for me. Dumping the reserve after 10 years of it being my primary go to spending card

It looks like most of the comments support you. I canceled my Chase Sapphire Reserve last October after having it for 10 years, which says a lot because I used to think it was one of the easiest premium cards to justify.

I’d honestly love to see the internal numbers right now: retention rates, downgrade activity, cancellation trends, all of it. At some point Chase has to notice the pushback. The bigger question is how...

It looks like most of the comments support you. I canceled my Chase Sapphire Reserve last October after having it for 10 years, which says a lot because I used to think it was one of the easiest premium cards to justify.

I’d honestly love to see the internal numbers right now: retention rates, downgrade activity, cancellation trends, all of it. At some point Chase has to notice the pushback. The bigger question is how long it takes before they rethink the benefits again.

Just another case of couponing. Having to go out of my way to use a coupon does not equal much value. Same with The Edit credit. Often enough these hotels are lower priced by around the same amount of the credit if booked directly with the property.

I'm so mad at myself for renewing this card in January I should have cancelled or at a minimum downgraded to Preferred. The new "benefits" are a joke.

The best dining credit seems to be the one on the Marriott Amex because the only limitation is that it is divided into a monthly allowance but it allows any restaurant coded transaction. The problem with this is if your city is not mentioned this has no value. Some of the cities really are not what they say because they have restaurants in nearby places instead.

I am so done with this credit card. The cost-benefit analysis has collapsed from my vantage point.

As Andrew said below, very different from Amex's Rest credit. Most of the eligible restaurants are "I suppose if I want to capture the credit" type of restaurant. And, not restaurants that I would normally choose. That's is challenge of this credit. And, it seems Chase has been very intentional with it. Combined with everything else, I feel as if Chase is *trying* to mess with me.

I was surprised to receive the dining credit for a restaurant I haven't seen on any list. As far as I know they don't take reservations and therefore are not bookable on OpenTable. Our bill was under $150 so we went back the next week and got the remainer of the full $150 credit. We dined more than a month ago and the dining credit still shows as used. This was at The Fish House in Monterey, CA.

I don't understand this statement: "Certain types of purchases may not be identifiable and will not qualify, like delivery and takeout ..."

In my experience, it works for take out when calling over the phone and paying on arrival or making the order in person, paying in person, and taking the food to go.

Maybe you meant that it won't work if the take out order and payment is done online like through DoorDash or some other third party?

Thank you, RealTaylor, you answered my question, and I hadn’t even seen where it was addressed in the peace which I truly did read.

@ RealTaylor -- Exactly, "may" is the key word there, and the idea is that it won't qualify if you order through a third party (like DoorDash), or if the restaurant somehow processes delivery order payments differently (which is rare).

Can it be used for carryout orders?

@ TravelinWilly -- I think you already know the answer now based on the above, but just to be 100% clear, you're fine with carry-out as long as it's done directly with the restaurant, and you pay there.

And it's a great question, so let me add that to the FAQs. :-)

Phoenix Palace in Chinatown. Thank me later. (Even if you don’t have a credit. Worth it.)

My understanding is that Amex's dining credit works virtually anywhere bookable through Resy. CSR partners with OpenTable. If CSR really wants to compete with Amex, why not open this benefit up to many, many more restaurants bookable through OpenTable, rather than just a select few in major cities?

I live in Seattle, which has a few restaurants on the list, but they're not places I'd be going anyways. I'd get far more value from this...

My understanding is that Amex's dining credit works virtually anywhere bookable through Resy. CSR partners with OpenTable. If CSR really wants to compete with Amex, why not open this benefit up to many, many more restaurants bookable through OpenTable, rather than just a select few in major cities?

I live in Seattle, which has a few restaurants on the list, but they're not places I'd be going anyways. I'd get far more value from this perk if it included OpenTable-bookable restaurants more generally.

That concept would cost Chase a lot of money.

We don't know if behind the scenes the "exclusive" restaurants are subsidizing to some extent the dining credit. It would not shock me if they are.

Opening it up to more restaurants would likely hurt Chase's bottom line. They like that it's difficult to use.

That concept would cost Chase a lot of money.

We don't know if behind the scenes the "exclusive" restaurants are subsidizing to some extent the dining credit. It would not shock me if they are.

Opening it up to more restaurants would likely hurt Chase's bottom line. They like that it's difficult to use.

@ Andrew -- It's a fair point, of course, and both Amex and Chase have different advantages with their premium cards. Conversely, Chase is great with the travel credit, while Amex's airline fee credit is of limited value.

My thoughts are along the same lines as what GEG_WA said. I suspect there's a closer financial relationship here, where the cost of this benefit is being subsidized somewhat by third parties. Meanwhile Amex owns Resy, so...

@ Andrew -- It's a fair point, of course, and both Amex and Chase have different advantages with their premium cards. Conversely, Chase is great with the travel credit, while Amex's airline fee credit is of limited value.

My thoughts are along the same lines as what GEG_WA said. I suspect there's a closer financial relationship here, where the cost of this benefit is being subsidized somewhat by third parties. Meanwhile Amex owns Resy, so clearly the goal there is to simply get people to increasingly use the platform.

I also live in Seattle and used our credit at TOMO. It was okay, but not a restaurant I would visit if I did not have a credit. Definitely not a restaurant I'd spend $200+ on. The other options in Seattle seem like douchey "tasting menu" prix fixe places. For $150, just get me a big steak.