While there are lots of excellent business credit cards out there, I’d argue that Chase’s portfolio of business cards — including the Ink Business Preferred® Credit Card, Ink Business Cash® Credit Card, Ink Business Unlimited® Credit Card, and Sapphire Reserve for Business℠ — are among the most compelling. The cards have exceptional welcome bonuses, great rewards structures, and valuable perks.

In this post, I’d like to cover the basics of these cards, especially given the incredibly compelling welcome offers that are currently available. Why are the cards worth having, and how can you maximize your odds of getting approved when applying?

Link: Learn more about the Ink Business Preferred® Credit Card, Ink Business Cash® Credit Card, Ink Business Unlimited® Credit Card, or Sapphire Reserve for Business℠

In this post:

Chase Ink business credit cards overview

Let’s start by covering the basics of Chase Ink & Sapphire business credit cards, including the welcome bonuses, the rewards structure, the perks, and more. As I view it, these cards are mostly complements rather than substitutes, given that only two of the cards have annual fees (at very different price points), and each card has its own strengths.

These cards also have consistently great welcome bonuses, so applying for multiple cards can be a great way to earn lots of points with a reasonable spending amount, which can fuel some great travel opportunities.

Note that in this post I won’t be covering the Ink Business Premier® Credit Card (learn more). While this is a potentially useful card, it exclusively earns cash back, so it isn’t a travel rewards card, unlike the rest of the cards in the portfolio.

Ink Business Preferred Card basics

The Ink Business Preferred Card has a reasonable $95 annual fee, and there are so many reasons to pick up this card:

- It has a big welcome offer of 100,000 bonus points after spending $8,000 within the first three months

- It has a generous rewards structure, as it offers 3x points on travel, shipping purchases, internet, cable, phone services, and advertising purchases made with social media sites and search engines, on up to $150,000 in combined purchases per cardmember year

- It offers valuable perks, like cell phone protection, rental car protection, and extended warranty protection

- Having this card gives you full access to the Chase Ultimate Rewards ecosystem, including the ability to transfer points to travel partners (though World of Hyatt transfers with the card are only 4:3)

Read a full review of the Ink Business Preferred Card.

Ink Business Cash Card basics

The Ink Business Cash Card is a valuable no annual fee card, and has a compelling value proposition:

- It has a fantastic limited time welcome bonus of 100,000 bonus points after spending $8,000 within the first four months

- It has a lucrative rewards structure, as it offers 5x points on office supply stores, internet, cable, and phones services, and 2x points on restaurants and gas stations, on up to $25,000 in combined purchases per cardmember year

- It offers valuable perks, like rental car protection and extended warranty protection

- The card only offers the ability to transfer points to Chase Ultimate Rewards travel partners in conjunction with another card

Read a full review of the Ink Business Cash Card.

Ink Business Unlimited Card basics

The Ink Business Unlimited Card is a useful no annual fee card, and there are several reasons you’d want to consider this card:

- It has a lucrative limited time welcome bonus of 100,000 bonus points after spending $8,000 within the first four months

- It has a solid rewards structure, as it offers a flat 1.5x points on all business purchases, with no limits

- It offers valuable perks, like rental car protection and extended warranty protection

- The card only offers the ability to transfer points to Chase Ultimate Rewards travel partners in conjunction with another card

Read a full review of the Ink Business Unlimited Card.

Sapphire Reserve Business Card basics

While not part of the Ink portfolio, the Sapphire Reserve Business Card has a $795 annual fee, and it’s the most premium Chase business card. There are several reasons to consider the Sapphire Reserve Business Card:

- It has a massive limited time welcome bonus of 200,000 bonus points after spending $30,000 within the first six months

- It has a lucrative rewards structure, as it offers 8x points on Chase Travel℠ bookings, 4x points on direct airfare and hotel bookings, and 3x points on select advertising purchases

- It offers valuable lounge access, including Chase Sapphire Lounge access and a Priority Pass™ Select membership

- It offers a variety of credits that can help offset the annual fee, including up to $300 in annual travel credits, up to $500 in annual hotel credits, and more

Read a full review of the Sapphire Reserve Business Card.

Why the Ink Business Preferred stands out

In recent years we’ve seen business credit cards become more compelling than ever before, as credit card issuers increasingly try to create products that meet the needs of small business owners.

The Ink Business Preferred® Credit Card continues to be one of the most rewarding business cards out there. There’s not another business card that offers a combination of a huge welcome bonus, generous return on spending, and useful perks, all while having such a low annual fee.

100,000 Ultimate Rewards bonus points welcome offer

The Ink Business Preferred Card is offering a welcome bonus of 100,000 Ultimate Rewards points after spending $8,000 on purchases within the first three months.

I value Ultimate Rewards points at ~1.7 cents each, so to me, 100,000 Ultimate Rewards points are worth ~$1,700. This is a great reward, and among the best welcome bonuses on any business credit card.

Valuable 3x points bonus categories

The Ink Business Preferred Card offers triple points in several useful categories that your business may spend quite a bit in, including:

- Travel

- Shipping purchases

- Internet, cable, and phone services

- Advertising purchases made with social media sites and search engines

You earn triple points on the first $150,000 spent in combined purchases in the above categories each account anniversary year (which means Chase isn’t using a January 1 through December 31 calendar, but rather it’s based on your account year).

Based on my valuation of points, that’s like earning a return of ~5.1% on spending in those categories, which is exceptional.

Cell phone protection benefit

With how expensive smartphones are nowadays, there’s a lot of value to having a credit card with cell phone protection, and that’s something that the Ink Business Preferred Card offers.

The Ink Preferred offers up to $1,000 per claim in cell phone protection against covered theft or damage for you and your employees listed on your monthly cell phone bill when you pay it with your Ink Preferred. You can have a maximum of three claims in a 12 month period, and there’s a $100 deductible per claim.

On top of that when you charge your cell phone bill to the Ink Preferred, you’ll be earning triple points on that purchase.

Rental car collision damage waiver coverage

The Ink Business Preferred Card offers primary collision damage waiver (CDW) coverage for rentals of most types of vehicles in most countries. This is one of the best credit card rental car coverage & insurance policies you’ll find.

There aren’t any countries that are specifically excluded from coverage through Chase cards, but the benefits guide does note that “coverage is not available where it is prohibited by law or by individual merchants, or is in violation of the territory terms of the rental agreement.” You’ll want to decline the rental car company’s collision or loss options.

You can confirm coverage for a particular trip by contacting the benefits team at 877-631-0919. Coverage is primary globally when renting for business purposes, while it’s primary internationally for personal rentals, and secondary in the United States for personal rentals.

When renting a car you’re also potentially earning triple points on your car rental by charging it to the Ink Preferred, since this qualifies as travel.

Comprehensive travel & purchase protection

In addition to the cell phone and car rental coverage, the Chase Ink Preferred offers other purchase and travel benefits, including (but not limited to) the following:

- Trip cancellation and interruption coverage, of up to $5,000 per covered traveler and $10,000 per trip

- Extended warranty protection, for up to a year on eligible purchases

You’ll want to read the cardmember agreement for exact terms, but this has the potential to be extremely valuable for purchases as well.

For example, I really like the trip delay coverage. If your trip is delayed by 12 hours or more, you can get up to $500 reimbursed for hotel accommodation, meals, and transportation. You just need to pay for the travel with your card, or with your Ultimate Rewards points.

Pool points with four no annual fee cards

While the Ink Business Preferred Card is valuable in and of itself, having it can make the points you earn on other cards more valuable as well. Chase has four fantastic no annual fee cards that can earn Ultimate Rewards points. I’m talking about the:

- Chase Freedom Flex℠ Credit Card

- Chase Freedom Unlimited®

- Ink Business Cash® Credit Card

- Ink Business Unlimited® Credit Card

The catch is that not all Ultimate Rewards points are created equal. By having the Ink Business Preferred, you can convert the points earned on the no annual fee cards (where one point is ordinarily worth a penny) into “premium” Ultimate Rewards points.

These can then be transferred to the Ultimate Rewards airline and hotel partners. Personally I value these points at ~1.7 cents each, so having the Ink Business Preferred makes other cards more valuable as well. That’s a major reason to have an Ultimate Rewards card with an annual fee.

Why the Ink Business Cash stands out

The Ink Business Cash® Credit Card is one of the all-around most lucrative no annual fee business credit cards out there. The card has no annual fee, an excellent welcome bonus, and a great rewards structure. In conjunction with other cards earning Ultimate Rewards points, this can be one of the most useful cards for a small business.

100,000 bonus points welcome offer

The Ink Business Cash has an excellent limited time welcome bonus of 100,000 points after spending $8,000 on purchases within the first four months.

You’ll see that the card is marketed as offering a bonus of $1,000 (rather than 100,000 points). That’s because on the surface this is a cash back card, meaning that the 100,000 points are worth $1,000 cash back. However, you can potentially convert these rewards into “full” Ultimate Rewards points, which I value at 1.7 cents each, so to me that bonus is worth $1,700. Yes, on a no annual fee card. That’s very good.

No annual fee

The Ink Business Cash has no annual fee. Getting a no annual fee card that’s super rewarding is rare, especially when you consider the value of the welcome bonus.

Awesome 5x points bonus categories

The Ink Cash offers 5x points on the first $25,000 of combined purchases per account anniversary year at office supply stores, and on internet, cable, and phone services.

If nothing else, earning 5x points on your cell phone and cable bill is huge, in my opinion. However, I should note that some may prefer the Ink Business Preferred® Credit Card, which offers 3x points on your cell phone bill, but also offers a great cell phone protection plan.

Even more 2x points bonus categories

On top of the 5x points categories, the Ink Cash offers 2x points on the first $25,000 of combined purchases per account anniversary year at restaurants and gas stations.

While these are categories that other cards also offer bonuses on, that’s pretty generous for a no annual fee card, and for many businesses it may be worth putting that spending on this card.

Business rental car coverage

The Ink Cash offers primary collision damage waiver coverage for rentals of most types of vehicles in most countries, except where it is prohibited by law, by individual merchants, or is in violation of the territory terms of the rental agreement. There aren’t many no annual fee cards offering rental car coverage, so I think that’s pretty remarkable.

Prior to renting, you should check with the benefits administrator (call the number on the back of your card) to verify your coverage. Keep in mind, you’re only eligible for coverage when renting for business purposes.

Travel & purchase protection benefits

In addition to rental car coverage, the Ink Cash offers other purchase and travel benefits, including (but not limited to) the following:

- Purchase protection for up to 120 days against damage or theft

- Extended warranty protection, for up to a year on eligible purchases

You’ll want to read the cardmember agreement for exact terms, but this has the potential to be extremely valuable for purchases as well.

Why the Ink Business Unlimited stands out

The Ink Business Unlimited® Credit Card is another one of the all-around most lucrative no annual fee business credit cards. The card has no annual fee, an excellent welcome bonus, and a great rewards structure.

100,000 bonus points welcome offer

The Ink Business Unlimited currently has a limited time welcome bonus of 100,000 points after spending $8,000 within four months of account opening. This is a great welcome offer, especially for a no annual fee card.

On the surface this is a cash back card, meaning that the 100,000 points are worth $1,000 cash back. However, you can potentially convert these rewards into “full” Ultimate Rewards points, which I value at 1.7 cents each, so to me that bonus is worth up to $1,700.

No annual fee

The Ink Business Unlimited has no annual fee. Getting a no annual fee card that’s super rewarding is rare, especially when you consider the value of the welcome bonus. Not only does the card not have an annual fee for the primary cardmember, but you can also add authorized users at no extra cost.

1.5x points on everyday spending

The Ink Business Unlimited offers 1.5x points on all business purchases, with no limits. This is a straightforward rewards structure, so there’s no need to focus on bonus categories. If you use this card correctly, it’s the single best Chase business card for earning Ultimate Rewards points on everyday spending.

Note that while points on the card can ordinarily be redeemed for one cent each cash back (meaning that 1.5x points is really 1.5% cash back), in conjunction with other Chase cards, these can be converted into “full” Ultimate Rewards points. Since I value Ultimate Rewards points at 1.7 cents each, to me the card offers a 2.55% return on everyday spending, which is excellent.

Business rental car coverage

The Ink Business Unlimited offers primary collision damage waiver coverage for rentals of most types of vehicles in most countries, except where it is prohibited by law, by individual merchants, or is in violation of the territory terms of the rental agreement. There aren’t many no annual fee cards offering rental car coverage, so I think that’s pretty remarkable.

Prior to renting, you should check with the benefits administrator (call the number on the back of your card) to verify your coverage. Keep in mind, you’re only eligible for coverage when renting for business purposes.

Travel & purchase protection benefits

In addition to rental car coverage, the Ink Business Unlimited offers other purchase and travel benefits, including (but not limited to) the following:

- Purchase protection for up to 120 days against damage or theft

- Extended warranty protection, for up to a year on eligible purchases

You’ll want to read the cardmember agreement for exact terms, but this has the potential to be extremely valuable for purchases as well.

Maximize the value of Chase Ultimate Rewards

The value of the points you earn with Chase Ink & Sapphire business credit cards varies based on which cards in the portfolio you have. Assuming you have the Sapphire Reserve Business or Ink Business Preferred Card, then all the points you earn on these cards could be converted into airline miles or hotel points, using one of the Chase Ultimate Rewards transfer partners (one thing worth highlighting is that only the Chase Sapphire Reserve — both personal and business — offers 1:1 transfers to World of Hyatt, while the Ink Preferred and Sapphire Preferred offer only a 4:3 transfer ratio).

Airline Partners | Hotel Partners |

|---|---|

IHG One Rewards | |

If you don’t have either the Ink Business Preferred Card, Sapphire Reserve Business Card, Sapphire Reserve Card, or Sapphire Preferred Card, then points earned on the Ink Cash Card and Ink Unlimited Card can only be redeemed for a penny each, which isn’t nearly as good. The key to maximizing value is to build up a portfolio of Chase cards.

Ultimate Rewards points can be transferred to over a dozen loyalty programs. There’s so much value to be had maximizing those programs, especially for redemptions at luxury hotels, and for premium cabin flights.

What makes Ultimate Rewards points even better is that you can also redeem them at an efficient rate toward a travel purchase through Chase Travel. You can redeem Ultimate Rewards points at a favorable rate toward travel purchases with the Points Boost through Chase Travel feature.

Chase Ink business card application tips

With the above out of the way, let’s talk about some of the logistics of applying for and being approved for Chase Ink & Sapphire business credit cards. The great thing is that you’re potentially eligible for the welcome bonuses on multiple of these cards.

Who is eligible for Chase business credit cards?

Eligibility for a small business credit card is easier than you might think. You don’t need to have a big company, and don’t even need to be incorporated. Even a small side business with limited business revenue makes you eligible for a business credit card, even if you’re just selling things on eBay, do some consulting on the side, have a rental property, or do freelancing, for example.

It goes without saying that you should always fill out credit card applications truthfully. I’ve written in the past about how to apply for Chase business cards as a sole proprietorship.

What are restrictions on applying for Chase business cards?

Chase’s general restrictions on applying for cards are as follows:

- There’s no hard limit on how many Chase credit cards you can be approved for, but rather there’s often a maximum amount of credit the bank is willing to extend you, in which case you may be asked to switch around your credit limits on some cards in order to facilitate an approval

- While you can typically be approved for up to two Chase cards in a 30 day period, that doesn’t usually work when both are business cards; you typically want to wait at least 30 days between business credit card applications to be on the safe side, though there are mixed reports (some people don’t have to wait that long, others have to wait longer)

- Chase has the 5/24 rule, whereby you typically won’t be approved for a Chase card if you’ve opened five or more new card accounts in the past 24 months; however, note that this no longer seems to consistently be enforced

- Regarding the 5/24 rule, the good news is that when you’re approved for a Chase business credit card, that application shouldn’t count as a further card toward the 5/24 limit, given that it won’t show up on your personal credit report

Can you earn the bonuses on multiple Chase business cards?

When it comes to eligibility for the welcome bonuses on Chase Ink & Sapphire business credit cards:

- Each card has a “once in a lifetime” rule, meaning you’re generally only eligible for the bonus on each card once

- Each card is considered separately for the purposes of earning the bonus, with the exception of the Ink Cash and Ink Unlimited, where you have to choose one card for earning the bonus

- In other words, you can apply for the Sapphire Reserve Business, Ink Preferred, and then either the Ink Cash or Ink Unlimited

How should you fill out Chase business card applications?

Those who already have business credit cards are probably familiar with the application process, but for those who aren’t, here’s what you need to know. It can be intimidating to apply for your first business credit card, though even if you’re a small business or sole proprietor, you should be eligible.

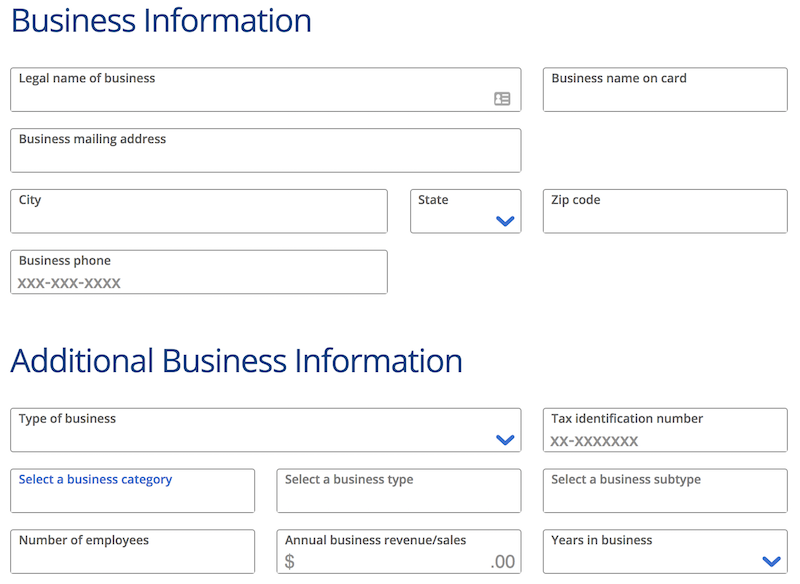

When applying for a Chase business credit card, you’ll be asked the following questions, in addition to the typical personal questions about your income, Social Security Number, etc.:

- Legal name of business

- Business mailing address & phone number

- Type of business

- Tax identification number

- Number of employees

- Annual business revenue/sales

- Years in business

If you’re a sole proprietor, how should you approach this? First of all, and most importantly, answer everything truthfully. I think the concern that a lot of people have is that they think they need an incorporated business, a separate office, etc., in order to be considered for a business card. That’s not the case:

- You can use your name as the legal name of your business

- The business mailing address and phone number can be the same as your personal address and phone number

- If you’re a sole proprietorship, you can select that as your type of business

- For the tax identification number, you can put your Social Security Number

- For number of employees, saying just one is perfectly fine

- For your annual business revenue, be honest about what it is

- For years in business, there’s no shame in saying that it’s new, that it has been one to two years, etc.

How hard is to get approved for a Chase business card?

When it comes to getting approved for business credit cards, Chase certainly isn’t the easiest issuer. In general I find American Express business cards to be easiest to be approved for. However, getting approved for Chase business cards isn’t as tough as some people assume, at least if you have excellent credit.

In my experience instant approvals on Chase business cards aren’t that common, so don’t be worried if the approval doesn’t come through right away. You’ll often get a pending decision response, and then eventually (hopefully) an approval.

Still, sometimes instant approvals do come through, and it’s always exciting when that happens. Just don’t be surprised if it doesn’t.

How does the 5/24 rule impact Chase business credit cards?

Chase has what’s known as the 5/24 rule, whereby you typically won’t be approved for a Chase card if you’ve opened five or more new card accounts in the past 24 months (however, there are increasingly reports that this is no longer enforced).

One exception is most business cards, including select cards issued by American Express, Bank of America, Barclays, Capital One, Chase, and Citi, generally won’t count as an additional card toward that limit, because they won’t be shown on your personal credit report.

One positive thing is that while Chase business cards may be subjected to the 5/24 rule, when you’re approved for them, they don’t count as a further card toward that limit.

In other words, if you’ve opened four new accounts in the past 24 months and then apply for a Chase business card, you’ll still be at four cards. If you then apply for another Chase business card, you’ll still be at four cards.

Can you be approved for all Chase branded business cards?

If your goal is to be approved for the Sapphire business card and two of the three Ink business cards (since you have to choose between the bonus on the Ink Cash and Ink Unlimited), your best strategy is “slow and steady,” as they say. I’d recommend applying for the cards a bit over 30 days apart, at the absolute fastest. If you apply for the first card on day one, apply for the second card on day 35 (or so), and then the last card on day 70 (or so). Or maybe wait even longer between applications.

If it were me, I’d definitely recommend making the Sapphire Reserve Business Card or Ink Business Preferred Card first, since they’re the all-around most lucrative, and have the biggest welcome offers.

Then you have to decide whether the Ink Business Cash Card or Ink Business Unlimited Card is a better option for you as the second card to apply for. If it were me, I’d probably apply for the Ink Business Unlimited Card, given that it offers 1.5x points on all business purchases, so it nicely balances the 3x points categories on the Ink Business Preferred Card.

I’d note that while this is how it’s supposed to work, Chase also sometimes has limits on how much credit can be extended to someone, so it’s totally possible that Chase will approve you for two of these, but not the third. Everyone’s situation will vary.

Chase Ink business credit card FAQs

Bottom line

Chase has some fantastic credit cards, and in particular, the issuer has great business credit cards. The lineup of Chase Ink & Sapphire business credit cards have some phenomenal bonuses, and between the Ink Business Preferred Card, Ink Business Cash Card, Ink Business Unlimited Card, and Sapphire Reserve Business Card, you could potentially earn bonuses hundreds of thousands of Ultimate Rewards points. That’s huge.

Not only do the cards have great initial bonuses, but they have excellent bonus categories, ranging from 1.5x points on all purchases, to 3-5x points in select categories.

Applying for business credit cards in general can be intimidating for new businesses, though I recommend giving it a try using the above tips, and you’ll probably be pleasantly surprised by the results.

Do you have any Chase business cards? If so, what was your experience getting approved for them?

In other news, if you think it's worth reporting, United is launching Cartagena Colombia