In May I first wrote about how United was planning on introducing a prepaid debit card. While this perhaps isn’t that exciting for credit-worthy individuals, a lot of Americans aren’t in a position where they can acquire credit cards. As a result, the prepaid industry has grown massively, and is now a $100+ billion annual industry.

Well, it’s now official — the MileagePlus GO Visa Prepaid Card has been introduced. The basic details are as follows:

- The card has an $85 annual fee

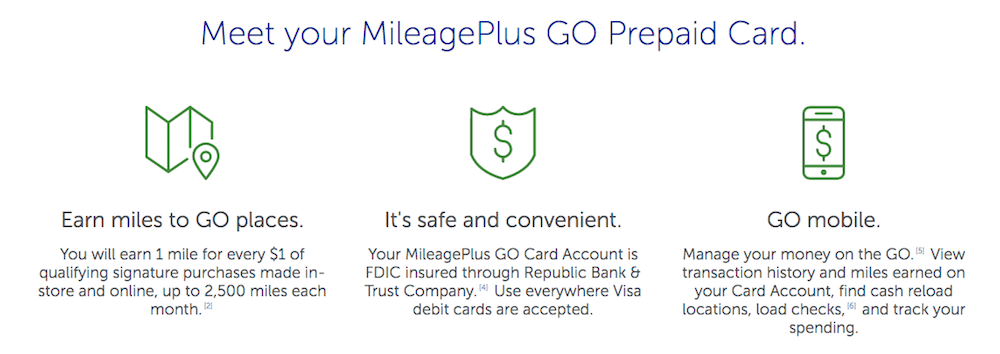

- You can earn one MileagePlus mile per dollar spent, up to 2,500 miles each month for qualifying signature purchases made in-store and online

This card is just about what I expected. PIN-based transactions don’t earn any miles, as they’ll be processed as debit. Meanwhile signature based purchases do earn miles, but at the rate of one mile per dollar spent, and with a cap of 2,500 miles per month.

For some people this card will make sense. If you’re not eligible for credit cards (either due to past problems with your credit, your age, etc.) or if you don’t feel like you can control your spending with the flexibility of a credit card, then this card could make sense. However, do keep in mind the $85 annual fee. I value MileagePlus miles at ~1.4 cents each, so you’d have to earn 6,000+ miles annually to breakeven on the annual fee.

However, if you have credit cards and use them responsibly, then there’s no upside to this card that I can think of.

I’d say the $85 annual fee is steep for this card, but then again, this is the only prepaid card on which you can earn airline miles, so it does have a unique value proposition. I suspect the reason for the annual fee is that there’s otherwise limited upside for the card issuer. Credit card companies make a lot of money on people financing charges, and that’s not an area where they can profit here, given that it’s a prepaid card.

Does anyone plan on picking up the MileagePlus GO Visa Prepaid Card, or see any other value that I’m missing?

(Tip of the hat to Points Fitness)

can i use the air miles on any air line or on what air line i can use the miles

I have a ton of student loans that can't be paid with credit cards. I think the miles I would get are worth more than the $85 annual fee. Agree or no?

One benefit you are missing is "peace of mind" of a pre-paid card.

Having suffered fraud in the past, I used pre-paid cards in high-risk situations, for example in high-fraud countries, unknown merchants, internet purchase abroad etc. I never have more money at risk then what's loaded on the card and, in case of fraud, don't have to spend my time on the phone with my bank, trying to block the card, recover funds...

One benefit you are missing is "peace of mind" of a pre-paid card.

Having suffered fraud in the past, I used pre-paid cards in high-risk situations, for example in high-fraud countries, unknown merchants, internet purchase abroad etc. I never have more money at risk then what's loaded on the card and, in case of fraud, don't have to spend my time on the phone with my bank, trying to block the card, recover funds or get a new card...

The problem with the UA card for that use case though are the high FX fee of 4.95% and a $4.95 fee at foreign ATMs. I'll stick with my AmEx Bluebird and a EUR based pre-paid card (both low fees) for high-risk situations.

This is a terrible valued card. Firstly, it's relatively expensive. The miles are only worth $600 if you spent the 2,500 points in purchases on the card at $0.02 per point and then the annual fee is $85. Furthermore, if you do not qualify for a credit card, you are likely to be in a financial situation that doesn't allow for travel often, so the points have no value. At the end of the year,...

This is a terrible valued card. Firstly, it's relatively expensive. The miles are only worth $600 if you spent the 2,500 points in purchases on the card at $0.02 per point and then the annual fee is $85. Furthermore, if you do not qualify for a credit card, you are likely to be in a financial situation that doesn't allow for travel often, so the points have no value. At the end of the year, you can only earn 30k points on this card. And United is getting "expensive" to redeem with relatively few good valued reward options.

Importantly, for people that do not qualify for a credit card and who would need this card, I'm sure the $85 could be better spent.

Can you fund with a credit card that doesn't treat it as a cash advance? That would be a huge benefit.

Any chance this is available for non US residents?

Is possible to double dip using this card? Paying off another credit card where points were earned and collect the united points with the prepaid card?

Worthless. But thanks for covering

The MileagePlus Go Visa Prepaid card is a terrible value for everyone. If one has sufficiently low credit that this is the only way to earn points then the correct answer is to walk away from the points and focus on fixing the credit problem - at a much lower cost - to get things back on track.