There are a lot of misconceptions about how credit scores are calculated. When I explain to people that I have 20+ credit cards open at a given time, the first question I’m usually asked is “doesn’t that ruin your credit score?!”

The answer is no, and that in many cases it can actually improve your credit score. But it’s very difficult for that to “click” with people. So I figured I’d explain in more detail, in part by sharing my own credit score.

In this post:

My credit score is excellent

My Experian credit score is currently 809 (on a scale of 300 to 850), which is better than a vast majority of consumers. To be honest, my score is lower than it was earlier this year (when it was 837), as I’ve applied for quite a few cards, and have been a bit sloppy with keeping my card utilization really low.

That being said, there’s really not much benefit to having a credit score of 840 vs. 800, for example, as either will qualify you for just about anything you may want. So while a super high credit score might be nice for bragging rights, there’s limited value beyond that. 😉

What’s the secret to a good credit score?

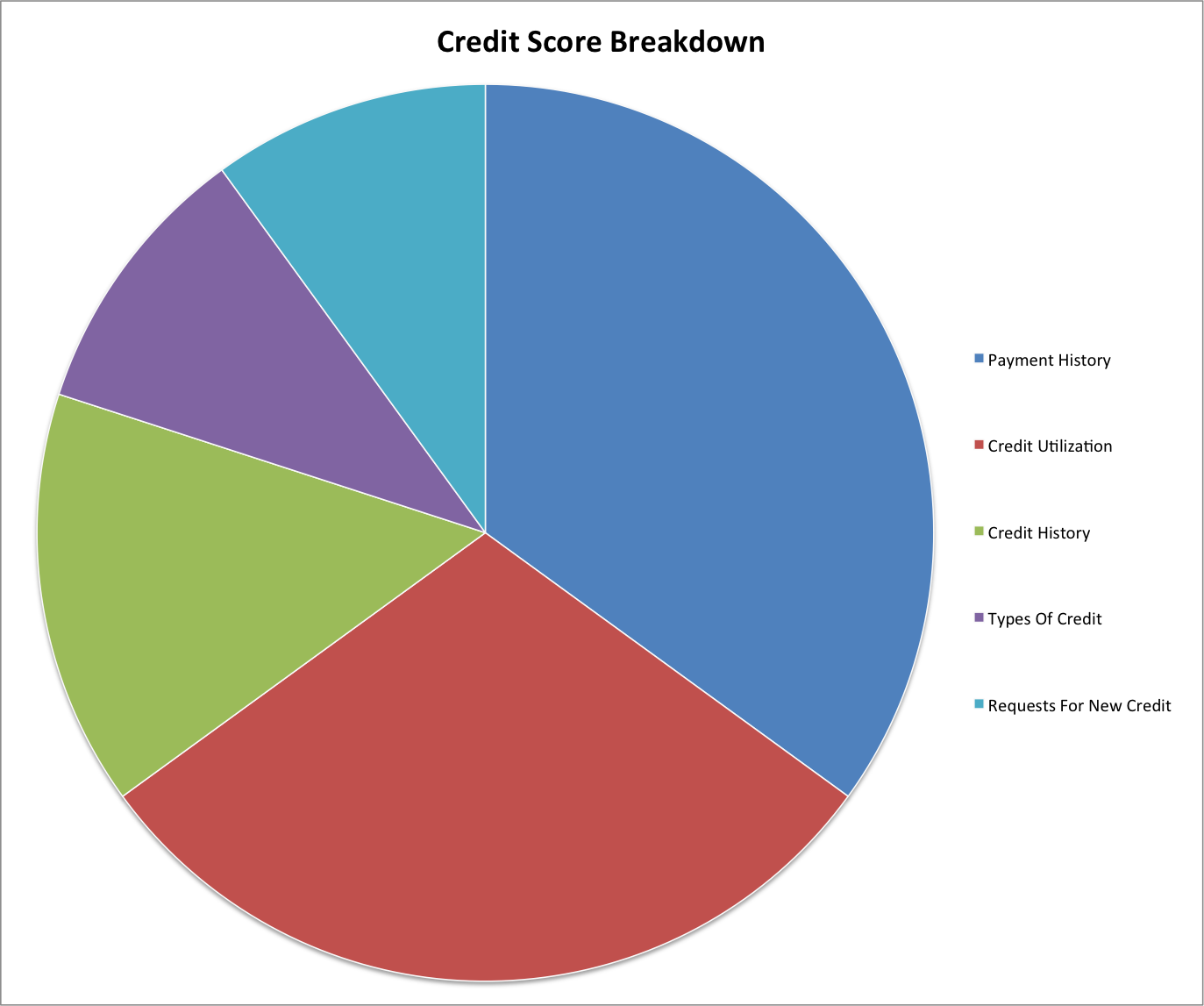

A lot of people are confused about how credit scores are calculated in the United States. To summarize, here are the major factors that determine your credit score:

- 35% of your score is made up of your payment history

- 30% of your score is your credit utilization

- 15% of your score is your credit history

- 10% of your score is made up of the types of credit you use

- 10% of your score is your request for new credit

How is it possible to have an excellent credit score while having a large number of credit cards open, and also consistently applying for new cards? Below are a few tricks that people easily overlook and/or can’t fully wrap their heads around.

Always make payments on time

35% of your credit score is made up of your payment history. That couldn’t be easier. Just pay your bills on-time, and you’ll basically get “perfect marks” for a third of your credit score. If you’re going to be involved in this hobby you’ll want to be well organized, which isn’t a lot of work, really. Just make sure you have payment due dates in your calendar, and have payment alerts set up.

Not only will you be hit with fees for making late payments, but your credit score will also be hit.

Keep your credit utilization low

30% of your credit score is made up of your credit utilization. This simply refers to what percentage of your overall credit you’re using.

Let me give an example. Say you have 10 credit cards, and have a $10,000 credit line on each. That means you have $100,000 of available credit. If you spend $90,000 on your cards each month, you’re utilizing 90% of your credit. That looks risky to the banks, because they start to wonder if you’re getting close to charging things you can’t actually pay for

Conversely, if you have $100,000 of available credit but only spend $1,000 per month, you’re only utilizing 1% of your credit. If you apply for new credits, the banks view you as low risk. Because you’re clearly not trying to max out your credit lines.

It actually helps to have a lot of cards, so that your overall available credit is high, while your utilization is very low. There’s one other trick here — pay off most of your credit card balance before the statement even closes. In other words:

- Say the closing date for a credit card is April 1

- The payment due date is usually a few weeks after that

- I simply pay most of my credit card bill two days before the statement even closes (in this case, March 30)

- That’s because what’s being reported to the credit bureaus is your utilization at the time your statement closes; so even if my credit line is $10,000 and I spend 90% of that, if I pay off most of that balance before the statement even closes, then the utilization rate will be super low

Keep some cards for a long time

15% of your credit score is made up of your credit history. One thing that largely factors into this is your average age of accounts.

In other words, the issuers want to see that you’ve been using credit consistently and responsibly for a long time. After all, if you’ve never had a credit card before and then suddenly get five at once, they’re not sure if you’ll be able to handle your credit responsibly (which is why it makes sense to apply for more cards gradually).

So while I apply for a lot of new cards, it’s important to also keep some cards long term. This is why I highly recommend a combination of cards that are worth paying annual fees on, as well as no annual fee cards that add value as well. Some cards are worth getting for their return on spending, while others are simply worth getting for their ongoing perks.

Not only are those cards worth it for the benefits they offer, but the added feature is that they help my credit score. That’s also why I do everything I can to keep no annual fee cards open, even if I don’t get much value from there.

That’s 80% of your credit score right there

The above alone accounts for 80% of your credit score. If you play your cards right (no pun intended), your score could actually be higher if you have a lot of cards than if you only have a few cards.

The last 20% of your credit score is made up of a combination of the types of credit lines you use and your requests for new credit. The former refers to having diversified credit lines (credit cards, mortgages, etc.) — the more variety you have, the better. It might seem backwards, but having a home mortgage or car loan can actually help your score.

The only part of your credit score that will negatively be impacted by applying for new cards is your requests for new credit, whereby your score will be temporarily hit by a few points for the inquiry. After 24 months that falls off your report, though, and you’ll just reap the positive benefits of having a lot of cards.

Bottom line

I’m sure most OMAAT readers already know that applying for lots of credit cards doesn’t necessarily hurt your credit score, and in many cases even helps it. But for those who are “doubters,” hopefully this helps with seeing how credit scores work in practice.

I doubt I’d consistently have such a great credit score if I didn’t have so many cards, since it really gives you quite a buffer in terms of credit utilization, average age of accounts, etc. So maximizing credit card rewards isn’t just useful in terms of accessing great rewards, but it can also have a positive impact on your credit score.

I’d like to know both how often a credit score is calculated and when. I have 15 cards and no other debt (mortgage, car, HELOC etc) AND I have paid off the entire balance on each before the due date on every single one…some for decades. However, my score fluctuates between 780 and 850 every few days.

I’m wondering if it’s because they all close on different days of the month and if they...

I’d like to know both how often a credit score is calculated and when. I have 15 cards and no other debt (mortgage, car, HELOC etc) AND I have paid off the entire balance on each before the due date on every single one…some for decades. However, my score fluctuates between 780 and 850 every few days.

I’m wondering if it’s because they all close on different days of the month and if they happen to look at my “credit card utilization rate” after a big purchase like taxes or tuition, it assumes the worst. Shouldn’t they be looking at your monthly average bank balance, net assets and salary also???

You write: 'Conversely, if you have $100,000 of available credit but only spend $1,000 per month, you’re only utilizing 1% of your credit. If you apply for new credits, the banks view you as low risk. Because you’re clearly not trying to max out your credit lines.'

Not always true. I was recently denied a CITI AAdvantage Platinum Select, because my utilization rate was 'Too low' at 3%. Go figure.

You were lied to, or the Citi rep (or you) misunderstood something. You weren't denied a mastercard because your utilization is too low.

Mauipeter’s experience is consistent with mine. I have 840 credit score, low utilization, no negative history etc.

I actually got a very nice recon agent who explained that Citi uses a different scoring algorithm for AAdvantage cards from the FICO they also pull. That algorithm prefers to see usage of existent credit, so the that a large no of accounts posting at 0 or low amounts results in a lower score. He admitted it...

Mauipeter’s experience is consistent with mine. I have 840 credit score, low utilization, no negative history etc.

I actually got a very nice recon agent who explained that Citi uses a different scoring algorithm for AAdvantage cards from the FICO they also pull. That algorithm prefers to see usage of existent credit, so the that a large no of accounts posting at 0 or low amounts results in a lower score. He admitted it was silly, but that is what Citi uses. If you look on Flyertalk you will see more discussion on this.

Yes, the algorithm. That's similar to what they mentioned in their denial letter.

My credit score fluctuated between 740-780 for years. Then I started the points game. I got my first card in Sept 2022 ( had a few other long term ones without any points availability). Now, I have a total of 6 ( 4 this year) and my credit score has jumped to 847. I use all the cards and pay them in full every month. Obviously, smaller amounts on each card so as not to...

My credit score fluctuated between 740-780 for years. Then I started the points game. I got my first card in Sept 2022 ( had a few other long term ones without any points availability). Now, I have a total of 6 ( 4 this year) and my credit score has jumped to 847. I use all the cards and pay them in full every month. Obviously, smaller amounts on each card so as not to overspend. My husband still doesn't get it and can't wrap his head around the points and miles game, so I play alone.

My wife laughed at me when I started studying collecting mileage points. But now she is enjoying our business class flights & luxury hotel rooms. AND, she now has a PERFECT 850 credit score with Experian. And I don't do any of the tricks like paying off the cards before the end of the billing cycle, I just pay on the whole balance on the due date. Our income is not huge, but we do...

My wife laughed at me when I started studying collecting mileage points. But now she is enjoying our business class flights & luxury hotel rooms. AND, she now has a PERFECT 850 credit score with Experian. And I don't do any of the tricks like paying off the cards before the end of the billing cycle, I just pay on the whole balance on the due date. Our income is not huge, but we do have lots of equity in our home, But that is not factored into the credit score, right?

It does take work, effort and some money to learn and play the game but it can be very rewarding. Although sometimes I wonder if a redirected all the time and energy I put into this hobby to my work and personal development if I would make more money and be able to pay cash for luxury travel.

The equity isn't factored into your score. But the fact you have a mortgage and credit cards and other credit are factors.

Don't see the point of doing this.

I have had two credit cards for several years. I just ask the banks to increase the credit limit on both, resulting in the same credit level that you attain having many credit cards.

Sure, if you don’t care about perks and SUBs.

Also for most of us… expecting 50k line of credit on a single card is a big ask, even with BofA and citi who can be quite generous.

I’m not familiar with the term SUBs. Perks are provided based on your spending. To access these perks, you must meet certain minimum spending thresholds. If these align with your usual monthly expenses or involve a necessary, one-time purchase, that’s reasonable. However, deliberately increasing your spending just to earn these rewards strikes me as financially irresponsible. Moreover, it contributes to the larger issue of overconsumption, which depletes the planet's finite resources and fuels toxic consumerism.

I’m not familiar with the term SUBs. Perks are provided based on your spending. To access these perks, you must meet certain minimum spending thresholds. If these align with your usual monthly expenses or involve a necessary, one-time purchase, that’s reasonable. However, deliberately increasing your spending just to earn these rewards strikes me as financially irresponsible. Moreover, it contributes to the larger issue of overconsumption, which depletes the planet's finite resources and fuels toxic consumerism.

Lots of ways of "spending" without spending. SUB = SignUpBonus. many of us meet spending thresholds either by spending on behalf of others (friend needs a sofa, I buy it on my card, he reimburses me) or other creative means. Obviously one doesn't spend more than normal, just to increase card spend. Manufactured Spending is another popular practice, I'm told.

I have friends who "don't see the point" of flying in longhaul International Business/First. Others "don't see the point" of staying in 5-star luxury hotels. One even "doesn't see the point" of reading OMAAT.

To each, his own.

I second the advice on paying on time. Definitely setup autopay on all cards. A few years back I had a $3 charge on a card I rarely used and forgot to pay for 2 months. My credit score dropped by more than 100 points and has stayed below 800 ever since. Will probably stay that way for 7 years after the goof.

Ben doesn’t just pay “on time”, he pays before the statement even closes.

Everyone should pay “on time”. No one need pay before the statement closes.

I also pay before my statement closes and sometimes a couple of times a month.

Many people "need" to.

I pay on the due date, not before. And my credit score is 832 while my wife got a perfect 850. I am not sure why our score is so high, but paying before the closing date certainly wouldn't make the scores even higher. We have a long history of occasionally having a month or two where we borrow a lot, and then pay off on the due date. Maybe that pattern has helped us?

My son had a payment go several months late, the amount was less than $200. His credit score dropped, but came back in about 5 months. I was surprised.

“There’s one other trick here — pay off most of your credit card balance before the statement even closes.”

That’s a crazy level of Credit Score OCD.

Unless you’re getting a mortgage or car loan/ lease, the fluctuations in your score from month to month utilization changes are meaningless to your life. Why add an additional level of hassle beyond auto payment?

If you are headed for a mortgage, I can see doing that a month or two before. Otherwise, just chill.

Disagree. If you routinely charge $10k/mo and your total available is $50k your util is 20%. If you make your payment routine 3 days before statement date, instead of some other date, you're performing the same tasks, just at a different date. The benefit is a 0% util. Not sure it's as pointless as you say.

How exactly do you benefit by paying early?

If your answer is “lower utilization/ slightly higher credit score”, how does that affect your life in any way? (unless you’re about to get a mortgage)

Ben’s not the only one with OCD.

People benefit by paying off their cards early because it helps them feel less anxious / stressed about carrying a balance on their card(s). The benefit is emotional regulation/management, it’s not financial benefit.

Imagine one's utilization was really high, as it might be if one practised a lot of Manufactured Spending. Say, tens of thousands per month, through one's credit cards, bringing utilization on some cards to 90%. First, one would have to pay the cards multiple times per month, just to keep them usable. Also, by making sure they had Zero balance on Statement date, it avoids the awkward appearance of spending one's annual income monthly. Zero...

Imagine one's utilization was really high, as it might be if one practised a lot of Manufactured Spending. Say, tens of thousands per month, through one's credit cards, bringing utilization on some cards to 90%. First, one would have to pay the cards multiple times per month, just to keep them usable. Also, by making sure they had Zero balance on Statement date, it avoids the awkward appearance of spending one's annual income monthly. Zero utilization is a better look than 80%. I'm pretty sure I'm not the one freak who practises this.

My fear of paying the card before the statement closes is that I won't get the points for the spending.

It makes no difference. Many card companies show you the points you earn per transaction, plus you could look at your total earned points vs. spend, if you wanted to verify with your own cards.

You will. Don't worry about that. It doesn't work that way.

Ben, that's an American thing. As told before, in Europe you can't have that quantity of CC's. At least in the country I live you can't? Which is Belgium. I have a big business and today I have 4 CC's, albeit all with a big Credit available because I can prove a big income on those banks. There is a thing here called National Bank, one that have to be consulted by every bank whenever...

Ben, that's an American thing. As told before, in Europe you can't have that quantity of CC's. At least in the country I live you can't? Which is Belgium. I have a big business and today I have 4 CC's, albeit all with a big Credit available because I can prove a big income on those banks. There is a thing here called National Bank, one that have to be consulted by every bank whenever you ask any bank to have Credit. Therefore I'm not sure your post is for great value for all OMAAT readers.

The points game is eminently an American hobby. The rest of the world is out of luck. Even Canadians cannot play. Blame it in your governments that ultra regulate the financial industry. I say this as an immigrant to the US who experienced what you are conveying before coming here. Free markets have problems but also offer amazing opportunities.

There is no connection to freedom here. This situation is partly attributed to smaller and weaker banks that failed to dominate the payment markets, unlike in France, Switzerland, and Germany, where larger banks predominantly manage payment systems.

As a Swiss covering Private Banking, I believe you also misunderstand what constitutes a free market. The US financial market is heavily regulated, and the US system is often described as "predatory" and "unfriendly" by liberal countries...

There is no connection to freedom here. This situation is partly attributed to smaller and weaker banks that failed to dominate the payment markets, unlike in France, Switzerland, and Germany, where larger banks predominantly manage payment systems.

As a Swiss covering Private Banking, I believe you also misunderstand what constitutes a free market. The US financial market is heavily regulated, and the US system is often described as "predatory" and "unfriendly" by liberal countries such as Switzerland or Singapore. For instance, US Americans are taxed based on their citizenship, not their residence. If you are unfortunate enough to inherit a US passport, you are obligated to pay taxes to a country with which you have no real connection. This is the antithesis of freedom.

@Nicolas

As a Swiss covering Private Banking, you seem to know very little about banking.

As a matter of fact, you don't seem to understand any financial system at all.

How could you even accuse someone to misunderstand what constitutes a free market.

Then the bogus larger smaller banks?

Nope, bank size has no influence over interbank networks. (seems like you don't even know this)

US system "predatory" and "unfriendly"?

...

@Nicolas

As a Swiss covering Private Banking, you seem to know very little about banking.

As a matter of fact, you don't seem to understand any financial system at all.

How could you even accuse someone to misunderstand what constitutes a free market.

Then the bogus larger smaller banks?

Nope, bank size has no influence over interbank networks. (seems like you don't even know this)

US system "predatory" and "unfriendly"?

I wonder why companies like to file Chapter 11. Too predatory I guess.

And if you even understand private banking, Switzerland or Singapore are not known because how liberal they are (they aren't but that's a whole different topic). It's because these 2 have a very stable banking system, stable economy, heavily regulated. Or in layman's term, your money is safe and secure.

This is the antithesis of freedom?

You can't even distinguish taxation and financial system.

Then you mix taxation with freedom?

Now let's pretend you know what interchange fee is and why regulating this makes the points game exclusive to US.

Let's also disregard that within EU, they also have credit bureaus and scoring system too, each with it's on methodology.

So when you say private banking, do you mean you only do transaction when you're the only one in the branch. Or just because you're the only one who knows the password to you banking app, makes your transactions on the app 'private'.

And the rest of the world is using public banking.

What utter drivel, totally incoherent poppycock!

Narcissistic mumbo-jumbo at its finest.

Game ON! Eskimo.

They started it, they have been verbally abusing numerous guests who have posted comments on this website, long before I became a regular reader.

They continue in the same vein with whomever they choose to victimise.

They have become the site trolls who contribute nothing of any value on any topic.

Their only interests are self gratification and the attempted belittling of others.

Their command and comprehension...

Game ON! Eskimo.

They started it, they have been verbally abusing numerous guests who have posted comments on this website, long before I became a regular reader.

They continue in the same vein with whomever they choose to victimise.

They have become the site trolls who contribute nothing of any value on any topic.

Their only interests are self gratification and the attempted belittling of others.

Their command and comprehension of the English language is infantile, even by third world standards.

However, if they wish me to indulge them by trading insults, then I repeat …. Game ON!

When commenters Eskimo or Mason (likely to be the same numpty) judge or criticize another person, it says nothing about that person; it merely says something about their own need to be critical, in an infantile manner.

Criticism of Eskimo or Mason may not be agreeable, but in their case it is necessary, it fulfils the same function as pain in the human body by calling attention to the unhealthy state of their minds.

Criticism however is easy for Eskimo and Mason; achievement in their case is impossible.

One of the greatest lessons in life is to acknowledge that even fools are right sometimes …. however, sadly Eskimo and Mason are proving to be the exception.

Finally, if Mason and Eskimo agree on everything, then surely one of them is unnecessary?

Nicolas, one finds it necessary, on behalf of the sane people who participate in this aviation blog, to apologise for the unprovoked verbal attack by our resident troll.

Eskimo, along with his fanboy Mason, (who is suspected to be Eskimo in drag) satisfies his/their trolling addiction by posting utter gibberish far too frequently.

Please do not take any notice of their gross ignorance.

"Even Canadians cannot play" is complete 100% nonsense. I'm a Canadian citizen resident in Canada and I've been playing the card game for nearly two decades, with innumerable cards, innumerable First Class flights, innumerable free hotel nights under my belt. these internet assertions really do get out of hand sometimes. "Canada's credit card scene is far less rich, lively, diverse than that of the US" would be a defensible statement. "Even Canadians cannot play" borders...

"Even Canadians cannot play" is complete 100% nonsense. I'm a Canadian citizen resident in Canada and I've been playing the card game for nearly two decades, with innumerable cards, innumerable First Class flights, innumerable free hotel nights under my belt. these internet assertions really do get out of hand sometimes. "Canada's credit card scene is far less rich, lively, diverse than that of the US" would be a defensible statement. "Even Canadians cannot play" borders on trolling.

Ben's advice here is largely applicable to Canadians as well. The system in Canada is substantially similar. Certainly the basic advice about having lots of cards, paying before statement date to reduce utilization, inquiries dinging score slightly and temporarily, average age of accounts, are all similar in Canada.

@ DenB

Agree, because US or Canada is about the same. But not here.

Most of Ben's stories aren't great value for many readers. You are free to skip over the stories that aren't relevant to you.

Note that TransUnion Canada keeps hard pulls on credit reports for 6 years instead of 2, but yes it's otherwise similar. https://www.canada.ca/en/financial-consumer-agency/services/credit-reports-score/information-credit-report.html

The availability of financial products such as credit cards is dramatically smaller in Canada. And the few cards available there offer fewer perks and much smaller sign on bonuses. Credit card churning coupled with big sign up bonuses is how you play this game, and there is no place where you can do it as profitably as in the US. The financial industry in the US is the most competitive in the world, thus the...

The availability of financial products such as credit cards is dramatically smaller in Canada. And the few cards available there offer fewer perks and much smaller sign on bonuses. Credit card churning coupled with big sign up bonuses is how you play this game, and there is no place where you can do it as profitably as in the US. The financial industry in the US is the most competitive in the world, thus the credit card bonanza. The banks are not offering these sign on bonuses out of the kindness of their hearts. Unrelated: if you are American you do pay taxes on worldwide income, but you always have the option to renounce your US citizenship if it bothers you so much.

Most of Ben's stories aren't great value for many readers. You are free to skip over the stories that aren't relevant to you.

Even if you had access to a similar array of products, this article wouldn't have been applicable to anyone living outside of the USA. They just do lots of things differently to the rest of the world.