In May 2022, Star Alliance, the world’s largest airline alliance, revealed plans to launch a co-branded credit card. That’s something we’ve never seen before from a global airline alliance. This week the card has officially launched in Australia, so we have all the details. It’s an incredibly innovative product, though I doubt we’ll ever see a card like this launch in the United States.

In this post:

Details of the HSBC Star Alliance Credit Card

For context, earlier this year, Star Alliance CEO Jeffrey Goh revealed that the alliance was working on a co-branded credit card. Here’s what we learned at the time:

- The credit card will launch in late 2022

- The credit card will let members earn miles that can then be transferred to Star Alliance airline partners

- The credit card will initially be launched in one country, and if successful, the concept will be expanded to other countries

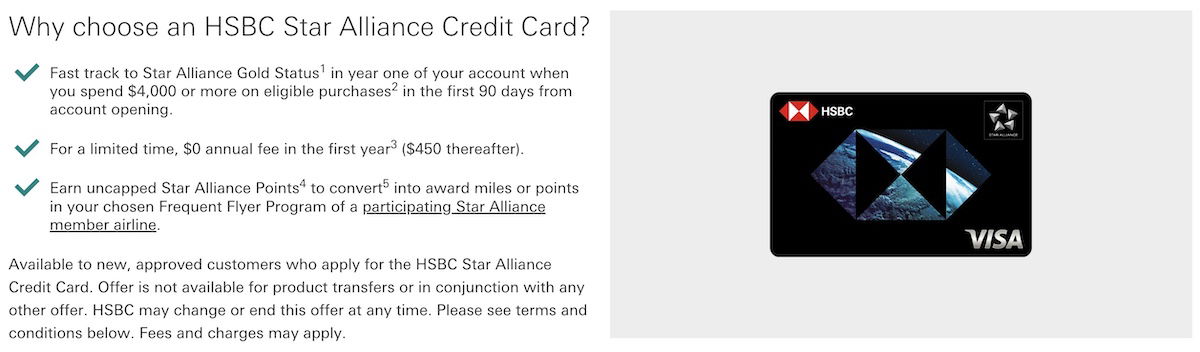

The HSBC Star Alliance Credit Card has just launched in Australia, and is open to new applicants. Here are the details of the card (all amounts are in AUD):

- The card has a $450 annual fee, waived for the first 12 months

- The card offers Star Alliance Gold status when you spend $4,000 the first year, and when you spend $60,000 in subsequent years; you can choose Star Alliance Gold status with one of seven airlines, including Air Canada, Air New Zealand, EVA Air, Singapore Airlines, South African Airways, Thai Airways, or United Airlines

- You’ll earn one Star Alliance point per dollar spent for the first $3,000 of spending per billing cycle, and after that you’ll earn 0.5 Star Alliance points per dollar spent

- You can nominate the airline you want your miles to be deposited with, and then they’ll automatically be deposited with that program after each billing cycle; you can choose from the same seven airlines as above, though note that 1,000 Star Alliance points only converts into 800 points with any of the above partners (and for Air New Zealand it’s 1,250 Star Alliance points per 10 Air New Zealand Airpoints Dollars)

It’s important to keep in mind that Australia isn’t as lucrative of a credit card market as the United States, due to lower interchange fees. Furthermore, the AUD is significantly weaker than the USD. So if the value proposition doesn’t seem great, that’s probably why.

It’s also logical that Australia is the first market where this is launching, since there’s no Star Alliance airline based there, meaning that the alliance isn’t really cannibalizing credit card business from a member airline. That being said, I know there are still a fair number of people in Australia who are loyal to Star Alliance.

This is creative, but is it lucrative?

As mentioned above, this is the first time we’re seeing a global alliance introduce a credit card. What’s my take based on the initial product being launched in Australia?

- While you can earn miles with your choice of several Star Alliance programs, unfortunately it doesn’t look like there’s some central Star Alliance points currency where you can bank points; in other words, this isn’t like a transferable points currency, but rather with each billing cycle you have to designate where you want your points deposited

- It’s unfortunate that only seven Star Alliance airlines are participating in this concept, meaning this isn’t really a universal currency for Star Alliance airlines; we’re talking about not even one-third of member airlines participating

- It’s nice to see that this card is offering a pathway to Star Alliance Gold status, as that’s a tier that adds a lot of value regardless of which Star Alliance airline you fly with; the ongoing spending requirement to earn it also isn’t unreasonable, given the perks

- In the United States, frequent flyer programs are the single most profitable part of airlines, and co-branded credit card deals are a big part of that; you can bet that United won’t be down with Star Alliance having a more lucrative credit card than MileagePlus’ card portfolio, and for that matter I suspect we may not see a Star Alliance credit card launch in the United States

- We already have incredibly lucrative card ecosystems, like Amex Membership Rewards and Chase Ultimate Rewards, which allow us to build a portfolio of cards and take advantage of a variety of bonus categories; that still seems like a better option to me, given that you can transfer rewards at a later point, rather than having to commit at the time you earn your rewards

- If we see this concept expanded to more countries, I imagine the value proposition will be significantly more compelling outside the United States, since there’s not as much competition

Bottom line

The Star Alliance has launched its first credit card, with rewards that can be transferred to seven different member frequent flyer programs. This is an innovative concept that we’ve never seen before from a global airline alliance.

This concept has first launched in Australia, in partnership with HSBC. The card offers up to one Star Alliance point per dollar spent (though each Star Alliance point gets you only 0.8 partner points), and there are opportunities to earn Star Alliance Gold status. I’m curious to see how this concept evolves.

What do you make of the Star Alliance’s new credit card?

Regarding the low earn rate for Australians - for context HSBC's Platinum Qantas card only allows you to earn 1 Qantas Point for every $1 of eligible spend, up to $1,000 per statement period and then 0.5 Qantas Point for every $1 of eligible spend thereafter per statement period.

The earn rate for the Star Alliance card is not so bad in comparison.

Correct, and useful context for US readers aghast at the low earn rate. Points Guy had an article today wishing for a similar product in the US, and noting that such a card would likely have a comparable earn to other US cards.

One QF or VA mile per AUD spend on co-branded cards is as much as you can expect (sometimes 1.5 for foreign spend and 2 on spend with the issuing airline) and...

Correct, and useful context for US readers aghast at the low earn rate. Points Guy had an article today wishing for a similar product in the US, and noting that such a card would likely have a comparable earn to other US cards.

One QF or VA mile per AUD spend on co-branded cards is as much as you can expect (sometimes 1.5 for foreign spend and 2 on spend with the issuing airline) and rarely for uncapped monthly spend. Domestic airline cards at the same annual fee price point have typically better earn rates than the *A card (and often sign-up bonuses). The HSBC QF card has a lower annual fee.

Amex has co-branded cards here with similar fees and earn rates as the Visa/MC ones. They also have MR earning cards with points that can be transferred to SQ and TG (among others but not the long list available to US members) at one mile per AUD spend (and very few bonus earns). Apart from that the best Visa/MC I've seen where points can be transferred to SQ offered 0.5 miles per AUD.

So, this card is not the best deal available if you want *A miles but its returns aren't risible given the competition.

I'm already SQ gold (and Australian). I can't see any benefit to me.

Are those 7 participating airlines the only Star Alliance flying to Australia? If so, it'd explain it, and leave room for growth. This is basically a trial with no local airline to annoy.

Nice that you can send the point s to any *A airline, ANA would be my choice, shame you can’t also nominate the airline you get status with. This isn’t worth a $450 annual fee and there’s no signup bonus.

However I guess it has to be a $450 card because SQ gold gives you lounge access on virgin Australia domestically. I guess I would consider it if I was a virgin flyer domestically and wouldn’t hit virgin gold through flying.

Depends what you want status to do for you. If you want lounge access and priority check-in etc, any *A would do. If you want the status bonuses for revenue trips on your preferred *A carrier being able to choose is important. For VA, SQ status is fine, and you can link your VA and SQ FF accounts and gain some advantage from that. If you're with VA, any *A gold status fills some gaps...

Depends what you want status to do for you. If you want lounge access and priority check-in etc, any *A would do. If you want the status bonuses for revenue trips on your preferred *A carrier being able to choose is important. For VA, SQ status is fine, and you can link your VA and SQ FF accounts and gain some advantage from that. If you're with VA, any *A gold status fills some gaps in international benefits when flying UA and AC, and gives you benefits with Air New Zealand across the ditch.

All these things only matter if you've decided the card is worthwhile, and they're only relevant for the first year. I can't imagine anyone meeting the spending requirements for later year status and not earning elite status from flying.

SQ Gold status might be quite handy when wait listing for saver awards.

After COVID, business travel certainly decreased....

I'm sure the sign up bonuses will come once Amex Au ups their sign up bonuses.

Whilst it’s nice to see this launch in Australia, it’s not like we don’t already have flex currency cards in the Australian market who offer a handful of *A partner transfers. It adds a big more choice but for most consumers, they won’t find value in being able to lob points to Lifemiles or Miles&More as their respective airlines don’t fly to Australia.

The mechanics of this card requiring you to set a transfer...

Whilst it’s nice to see this launch in Australia, it’s not like we don’t already have flex currency cards in the Australian market who offer a handful of *A partner transfers. It adds a big more choice but for most consumers, they won’t find value in being able to lob points to Lifemiles or Miles&More as their respective airlines don’t fly to Australia.

The mechanics of this card requiring you to set a transfer partner each month sounds extremely fustrating especially if the consumer is looking to maximise redemption value (which is a considerable value proposition over a co-brand credit card… of which the Australian market is 80%+ Qantas co-brands). If they changed this to a points bank that you could draw down on when you want to (like every other flex currency in the market), I’d suspect more folks would consider getting onboard with the card.

The other thing is that whilst Australia tends to have crappy interchange fees, the sign up bonuses aren’t too bad. This cards perks really don’t stand up enough to a solid sign on bonus which will heavily sway consumer preference to existing cards on the market.

'The other thing is that whilst Australia tends to have crappy interchange fees, the sign up bonuses aren’t too bad.'

Whether the interchange fees are crappy or not depends on your perspective. Yes they are crappy for credit card companies and the people (like points collectors) who benefit from what they can give back to us, but for other users and the businesses that accept card payments they are good, and that's who the banking...

'The other thing is that whilst Australia tends to have crappy interchange fees, the sign up bonuses aren’t too bad.'

Whether the interchange fees are crappy or not depends on your perspective. Yes they are crappy for credit card companies and the people (like points collectors) who benefit from what they can give back to us, but for other users and the businesses that accept card payments they are good, and that's who the banking regulators were thinking of when they set the rules on interchange fees. They are priced as an essential service not as a luxury, and I'm happy with that even though it limits how many points I can earn. And yes, sign-up bonuses are good here if you're prepared to go through the churn of changing or adding to your portfolio of cards. If you fly much, SQ gold status (which gets you VA lounge access) isn't too bad a sign-up bonus.

Rereading the T&Cs, 0.8 Kris miles per AUD isn't much good when compared to 1 for Amex MR and 1 QF mile that's commonly available for their co-branded cards (some of which pay an extra mile for spending with QF, and some with higher returns on foreign spending). I remain to be convinced it's a good deal for me.

In the absence of spend, does the $450 annual fee provide lounge access? If not, what's the point?

Regarding spend, what a ROTTEN card. 1X on the first $3k of spend every month and 0.5X thereafter, then transfer to Krys Miles at 0.8X? If one wants to maintain Star Alliance Gold, it's $60k per year. So, $36k at 1X and $24k at 0.5X equals 48k Star Points, which equals 38,400 Krys Miles. A$60k = US$39,200. So, the card earns roughly 1X Krys Miles per US$. Punt.

PS - Often non-US-issued cards have foreign transaction fees. May want to check on that.

Maybe they will announce some transfer bonuses. Agreed though, you would spend more time trying to maximise the earn and transfers than your time may be worth, due to the many ifs and buts in the deal.

It will be interesting to see how this works as a proof of concept. As Ben noted, interchange fees in Australia mean that credit cards can't be as lucrative as they are in the US, typically you earn one point per dollar spent (AUD) on airline specific cards and less on transferable card currencies. I'll be interested to test the value proposition against Amex MR for SQ, and *A Gold with SQ in the first year is a positive.

As Star Alliance is led by Lufthansa, perhaps the first market will be Germany (and maybe also Belgium, Austria and Switzerland).

But on the other side, Lufthansa already has own credit cards at all those markets.

Would be great for LH if you could earn more than 1 mile per $ like the LH card since no other currency can transfer to them.

If United would not be a part of it, it would benefit everyone. But with an US company and bank involved, they would abouse all others in the world, except there own.

Star alliance without United, that would be so great.

You are suggesting kicking United, a founding member, out of Star Alliance?

Sounds like a good idea for markets like the UK, where no single Star Alliance carrier has a strong presence but collectively they do.

They certainly would not undercut existing credit cards issued by member carriers - unless their end goal is to kick the carrier out of the alliance passive aggressively.

This is a good idea for markets outside of the US credit card ecosystem. We have lots of choices between products & methods to rack up points. Not the case elsewhere.

I wish airline alliances were more like hotel programs where I have more choices how I spend my miles and consistent program across all the carriers.

Booking partner airlines is already complicated. Making transferrable points is just adding another layer of complication. Not to mention having disparity between miles from different airlines.

If this card were to materialize, I would imagine a fixed point redemption would be the answer. So it could either be 10k points gets you 1-750 miles or 10k points is $100 off any ticket. Either way must be booked through some broken booking platform.

And we still...

Booking partner airlines is already complicated. Making transferrable points is just adding another layer of complication. Not to mention having disparity between miles from different airlines.

If this card were to materialize, I would imagine a fixed point redemption would be the answer. So it could either be 10k points gets you 1-750 miles or 10k points is $100 off any ticket. Either way must be booked through some broken booking platform.

And we still haven't discuss card benefits. Giving Star Alliance Silver benefits probably wouldn't attract anyone at all. Giving perks that would be similar to Star Alliance Gold would cannibalize the incentive to earn over just paying for it. That wouldn't make member airlines happy.

This could potentially be cool for people residing in a country without Star Alliance base - I live 40 minutes drive from LH Group hub but can't get airline credit card because it's across a line on the map. I understand how it may be inefficient for individual airlines to deal with these smaller markets and doing it on alliance-level could solve this issue. Ideally, SA could partner with one of the pan-European banks (e.g....

This could potentially be cool for people residing in a country without Star Alliance base - I live 40 minutes drive from LH Group hub but can't get airline credit card because it's across a line on the map. I understand how it may be inefficient for individual airlines to deal with these smaller markets and doing it on alliance-level could solve this issue. Ideally, SA could partner with one of the pan-European banks (e.g. N26) to cover the entire European market rather than individual member states only.

Don't knock it before you try it..Yes there are Americans that see no further than their own border. Lots of them unfortunately. This from an American himself.

Wasn't it also *A that promised an airline agnostic (or all-inclusive) awards booking tool? What ever happened to that vaporware.

I mean, this sounds good, but in reality doesn't add much value. The whole point of alliances is this "transfer to a *A partner" isn't necessary. If you move miles to LifeMiles or AC, you can redeem on most anything.

The only reason this would matter is if LH or SQ first redemptions are on your 'to do' list, but even then there are solutions now from cards or the banks.

"The whole point of alliances is this "transfer to a *A partner" isn't necessary."

That's a statement by someone who clearly hasn't had the face the difference in what "should be" versus what '"is," in terms of redemption.

Case in point: try to get a roundtrip Business redemption on LAX/EWR-SIN using UA miles, on anything even approaching a realistic inbound/outbound schedule.... let us know how easily that happens.

u are being naive, the banks/airlines won't allow something that will cannibalize the exisiting products. More likely we see something like Redeem your 20k *A points for a $250 towards a ticket on any Star Airline.

Likely one of the smaller players like Synchorny or Cardless

This.

A alliance transferable points system would be very cool but earning 1x or gasp. .5x is crap.

Wouldn't it just make more sense to synchronize mileage earning all Star Alliance partners and then require partners to have the same award space open to partners as to its own members. LH is notorious for offering saver fares to it's members months in advance then (even with a half full cabin) opening space a few days prior to departure.

I could include Lounge Access

I can only imagine how many times in the T&C we will see:

*Does not apply to SQ

**Does not apply to SQ

***Does not apply to SQ

...

...

...

If this allows miles and more transfers then I’m in, but I doubt it.

Maybe, just maybe, a global airline alliance has figured out that 96% of the world’s population isn’t American, and is making something credit-card-related for them?

Very unlikely. Rest of the world will still get mediocre benefit cards while still paying the same amount of fees as the american version, i.e. Amex, whose Platinum benefits are ridiculous cut down around the world when compared to US, but still charging the same fees, if not more in some markets

The rest of the world has limits on credit card transaction fees making them far less lucrative than in the US where they’re free to charge a lot more.