To state the obvious, this blog isn’t about investing (well, other than “investing” in your points balance), 😉 though I do often discuss airline economics, and sometimes the topic of airline stocks comes up.

While I’m interested in investing, I’m by no means a financial expert, so please don’t interpret any of this as financial advice, or anything like that. This is just an airline nerd sharing his (probably baseless) opinions, so take it with a grain of salt. However, here’s a topic that I find interesting — under what circumstances are airlines worth investing in through the stock market… if ever?

In this post:

It’s hard to argue that airlines make good long term investments

I absolutely adore the airline industry, though there’s no arguing that it’s an incredibly challenging business. At least in the United States, airlines have very high fixed and variable costs, unionized workforces with labor contracts that can’t easily be renegotiated, and they’re always the first to suffer in hard times.

Warren Buffett once famously joked that if a farsighted capitalist had been present at Kitty Hawk in 1903 (when the first flight took place), he should have shot Orville Wright.

Keep in mind that before the pandemic, Buffett’s Berkshire Hathaway was the largest shareholders of US airlines. Those stakes were all panic sold at the start of the pandemic, when they were at absolute lows. Interestingly, Berkshire Hathaway recently got back into airline investing, buying a stake in Delta.

There’s no denying that the US airline industry at large has made massive progress when it comes to becoming more sustainable. That’s largely because US airlines have figured out how to tap into loyalty programs as major profit centers, though not all airlines benefit equally from that. Airlines have also gotten much better at monetizing their products, which is a double-edged sword for consumers.

Looking at US airlines, the absolute top airlines might have a margin of 10% in good years, while most players still lose money. And when things go wrong? Well, they’re quickly begging taxpayers for a bailout to stay afloat.

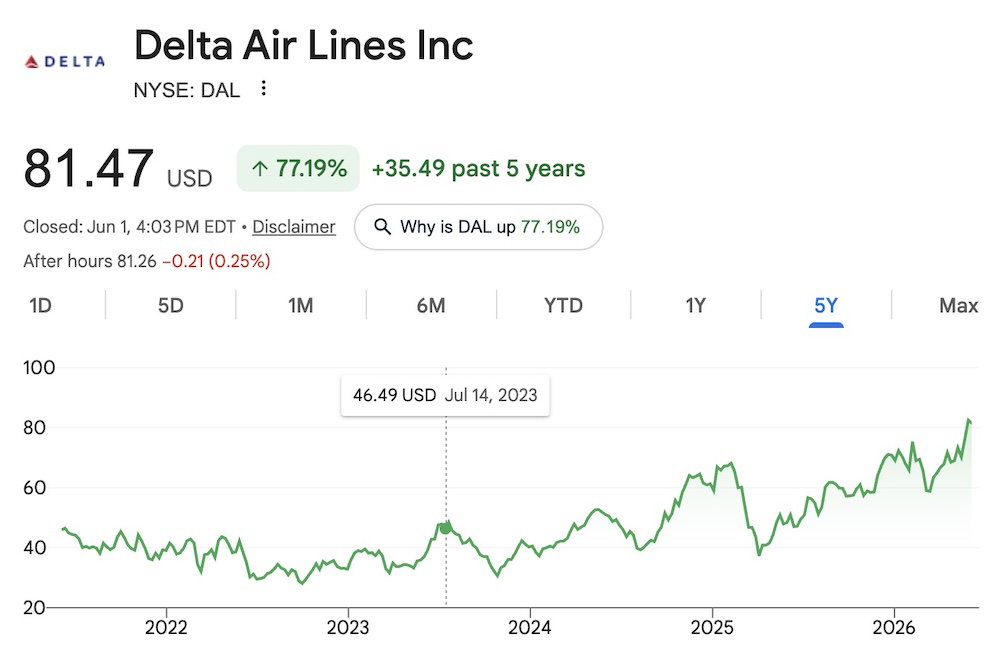

Let me be clear, there are certainly situations where airline stocks appreciate over time, even without “buying the dip,” so to speak. For example, if you purchased United stock in mid-2023 at its rough peak at the time, you would’ve seen a roughly 100% return over that period, compared to the stock price today. Pretty great, eh? And if you bought during a dip, you might’ve even seen a return of closer to 200%.

United’s turnaround, and in particular, the company’s narrative, is something we haven’t otherwise seen replicated much. You would’ve seen healthy returns with Delta stock as well, but not as high, given that the airline was already the leader at the time.

Admittedly Delta and United are the two airlines that do quite well, and we won’t look at the stock prices of other airlines, which are a bit less pretty. 😉

The two scenarios where I see merit to investing in airlines

More broadly speaking, when is there merit to investing in airlines? As I see it, there are two situations where it most makes sense:

- If you think an airline will be a target in consolidation

- If you’re just “buying the dip,” and think the price will quickly recover

I think there’s an argument to be made for buying airline stock if you think an airline will be the target of consolidation, though this is highly risky, and the upside isn’t always huge:

- I think the dream scenario is what Hawaiian Airlines saw when it was acquired by Alaska Airlines, where the stock went from under $5 to over $13 virtually overnight, given Hawaiian’s low share price and Alaska’s (relatively) high purchase price

- In fairness, we’ve also seen successful consolidation with minimal immediate upside; Allegiant recently acquired Sun Country, and that results in a premium of “only” around 20% (still good, but I think a 160% premium sounds better) 😉

- Of course many people gambled with JetBlue’s failed takeover of Spirit, and tried to buy Spirit shares, in hopes the deal would get regulatory approval; those people got burned, when a judge blocked the merger

- I’m sure many people have purchased JetBlue stock, with hopes of the carrier being acquired, though that’s looking less and less likely by the day; given the amount of debt JetBlue has, I also struggle to believe the airline would get a huge premium on its share price

I think the other argument to be made for buying airline stocks is essentially to just “buy the dips,” when things get bad, and the market overreacts. I’m reminded of the September 2025 Airlines Confidential podcast, hosted by Scott McCartney, where JPMorgan airline analysts Jamie Baker and Mark Streeter were guests (they’re both awesome guys, and you’ll hear Baker on just about every airline earnings call, and I always enjoy hearing his questions, as he doesn’t hold back).

They talked about JPMorgan’s airline investment strategy, and brought up the “down 30 in 30” trading rule. Essentially the idea is that if an airline stock loses 30% of its value in 30 trading days, there’s a high chance that this was an overcorrection, and the stock will go up quite a bit in the subsequent 180 trading days a large majority of the time.

The example they give (and this might not be 100% accurate, since they were going off memory) is that there were 29 instances where United (or pre-merger Continental) stock lost 30% of its value in 30 or fewer trading days.

The analysis was that if you purchased the stock at the very first instance where it dropped 30%, over the course of the following 180 trading days, there’s a 71% likelihood of generating greater than 50% returns, with the average being that the investment roughly doubles. And keep in mind you can do better than that potentially, since this doesn’t even assume buying at the bottom.

The idea is that when the market has decided so quickly that things are so bad, the market has routinely been incorrect. Interestingly, during the recent Iran conflict, most airline stocks didn’t quite drop that much, though American did (probably because it’s the least financially secure among the “big four”). Before the conflict, on February 6, American’s stock price was $15.24, and within 30 trading days, it fell to $10.30, a decrease of well over 30%.

A few months later, the stock is trading at $14.34 again (and days ago it was at $14.92), so that’s a nearly 50% increase in stock price within roughly a few months (and that’s not even 180 trading days).

Everyone should use their own judgment, but when you look at the charts, it does seem like one of the areas where airlines beat the market (on average) is when it comes to the depth of the dips, and the speed of recovery, given the industry’s volatility, and the panic selling that happens.

Interestingly, Baker and Streeter argued that long term they think it’s increasingly likely that you’ll be able to park money in airlines and generate above average returns on a three to five year horizon. If you time things right, that’s probably true. The issue is how few airlines are actually “healthy,” and just how much can change over a three to five year period.

Bottom line

Airlines are really tough businesses, and personally (as a non-financial expert), I fail to see merit to investing in them in the long run, given that we have access to a broader market. There are just so many other industries with better potential for higher returns, and with less volatility.

That being said, I’d argue there are two situations where you can come out ahead investing in airlines. One is if you think consolidation is likely, though that also comes with huge risks — there’s upside, but the airlines that are targets of consolidation also often aren’t in a great spot.

The other — and it’s still risky, but less so than hoping for a merger — is following the “down 30 in 30” trading rule. If an airline stock drops 30% in 30 trading days, it’s highly likely the stock will go up by at least 50% over the course of 180 trading days. There’s no guarantee, of course, but better than two-thirds odds sound pretty good to me, especially when the upside is often significantly more than 50%.

Where do you stand on buying airline stocks? Under what circumstances do you think it makes sense?

The case for buying airline stocks is best expressed by those who bought PanAm and Spirit : Fools .

Albert are you calling me a fool? I hold a number of different airlines stocks, but only World Class Airlines actually. No U.S. third world airlines holdings.

just post your investment statement.

The rational me follows a policy of putting my retirement and non-retirement investments in etfs and funds that follow the broad market (e.g., Buffet will have his wife's Inheritance put in an SP500 ETF). I allow the playful me have a small portion of my non-retirement funds for speculation (small potatoes) . Twenty months or so ago, people here and elsewhere were bashing Boeing with stupid reasoning. I bought some. It's up 48%. Same thing...

The rational me follows a policy of putting my retirement and non-retirement investments in etfs and funds that follow the broad market (e.g., Buffet will have his wife's Inheritance put in an SP500 ETF). I allow the playful me have a small portion of my non-retirement funds for speculation (small potatoes) . Twenty months or so ago, people here and elsewhere were bashing Boeing with stupid reasoning. I bought some. It's up 48%. Same thing about Southwest a year ago. My investment is up 28% before considering dividends. Yes, PAPER profits. But, betting against the smug, opinionated, loud mouthed element here and at other travel blogs seems a good strategy. It's better than going to Vegas.

Anything is "better than going to Vegas" .

Boeing profits come from manufacturing mass killing machines.

From missiles to MAXs.

And boy did Benny used a lot of missiles in the past year.

The 30% seems like a random number.

Bob Crandall, former CEO of AA, stated that airlines were a great place to work.

However, he discouraged his employees from investing in airlines calling it a "nasty, rotten business."

Enough said!!

"100% return over that period, compared to the stock price today. Pretty great, eh?"

Um, compared to what? 100% return is what Micron achieves every month. You need to look at risk-adjusted returns.

let's not forget that DAL and LUV are the only 2 US airlines that pay dividends and there are some investors that seek out dividend paying stocks.

Well golly-gee! Delta Airlines pays less than 1% dividend, while Southwest Airlines are paying just a little more at 1%. Contrast this with say Singapore Airlines who are paying between 4-5%, or even BA (IAG) of 2%.

Not a lot to crow about Walter …. right?

every investment is about timing and a track record.

UA gained as much post covid because it was the so badly managed for so long. and then it hit the ceiling which is below parity with DL

and yet UA doesn't make as much revenue or have a market cap as high as DL even though UA flies 10% more ASMs.

DL has demonstrated over the past decade plus that it is the best run...

every investment is about timing and a track record.

UA gained as much post covid because it was the so badly managed for so long. and then it hit the ceiling which is below parity with DL

and yet UA doesn't make as much revenue or have a market cap as high as DL even though UA flies 10% more ASMs.

DL has demonstrated over the past decade plus that it is the best run airline worldwide and has the market cap to prove it.

Over the past year, DAL stock is up 68% which beats the rest of the US airline industry and most major indices.

and it will be the refinery and MRO businesses that will give DL a combination of advantages which no other airline can match

If we know anything about flight, it’s that things can only go up, and they stay up forever. For-eva-eva!

Stock market bulls excrement is now your mantra Walter? I know little about the U.S. Airline stocks market. I know only a little more about the World Class Airlines stocks we hold, however, I am always willing to learn from your experience Walter, do prattle on and give us all the benefit of your vast knowledge?

To quote:

There are two types of people.

Those that can’t market time and those that don’t know they can’t market time.

Apparently MNL airport operators are forcing CX to close their lounge.

Could be an interesting article considering it's the best lounge by far in that hellhole of infrastructure

There are often buyers for United, Delta, and Southwest, but not American because UA, DL, WN are part of the S&P 500. So buy a 500 index fund and you own UA, DL, WN.

In the long run airline stocks are a good way to become a millionaire. Only caveat is you have to start with a billion.

Think our legacy airlines are more credit card businesses than actual airlines. They lose money on flying people around.unless you are AA and you still barely make money.

Very simple concept that some people struggle for years to understand until they eventually learn from experience (and probably some never internalize this):

Everything you think you know or can predict about a financial asset’s future performance is already priced in.

That’s it. Every possible idea has already been thought of, traded upon, and the now-current price already reflects that.

Unless you have inside information (which is illegal) or are a member of...

Very simple concept that some people struggle for years to understand until they eventually learn from experience (and probably some never internalize this):

Everything you think you know or can predict about a financial asset’s future performance is already priced in.

That’s it. Every possible idea has already been thought of, traded upon, and the now-current price already reflects that.

Unless you have inside information (which is illegal) or are a member of congress, don’t delude yourself into imagining that you’re a special sort of clever.

@ Simon -- People say that, but... have you seen the market recently? ;-)

@Ben Schlappig

Economist John Maynard Keynes famously noted, "The market can remain irrational longer than you can remain solvent."

So you can be correct but still not come out ahead financially.

Have you heard of the Bogleheads?

@Simon , the quote about irrationality is very wise but probably less relevant today than it used to be. Algorithmic trading quickly amplifies any subjectivity that pricing in inevitably entails which means that there's more overcorrection nowadays than what you might've seen in the past. You didn't need to be a commodities guru back in March 2020 to realise that oil prices can't stay negative (!) for too long. This isn't even about timing the...

@Simon , the quote about irrationality is very wise but probably less relevant today than it used to be. Algorithmic trading quickly amplifies any subjectivity that pricing in inevitably entails which means that there's more overcorrection nowadays than what you might've seen in the past. You didn't need to be a commodities guru back in March 2020 to realise that oil prices can't stay negative (!) for too long. This isn't even about timing the market, it's about value investment - similarly, there are quite a few decent companies in the S&P 500 but the massive growth in index funds means that their shares are quite expensive because everyone is buying them. Trying to make money timing the market is unlikely to work for the average person, and doing so with borrowed money/leverage may lead to financial ruin, but it is possible to lock in decent entry points for those wanting to buy and hold.

I still wouldn't invest in airlines though - as with things like crypto, I think that the regulatory risks aren't properly reflected in their share prices. Changes to frameworks such as open skies agreements are outside of an airline's control and could have serious consequences on its viability- or just ask Finnair how they're getting on with their business model of connecting Europe with Asia via the Russian airspace!

@Simon

Have you heard of this useless electronic medium that people suddenly assign absurd valuations to it called bitcoins.

@Eskimo

Yes, I have heard of Bitcoin...I'm not sure I understand the point - is it that Bitcoin's value has been irrational for as long as it has without any expectation of crashing to zero?

Except, there is a lot of evidence against this argument for semi-strong market efficiency (and some the opposite direction that private information is impounded in the current price). But, these studies find the inefficiency is not exploitable. And, obviously, if one found a way to exploit those inefficiencies, others would copy. This is why a majority of my non-retirement and all my retirement savings are in broad-market etfs and funds. I laugh at those who...

Except, there is a lot of evidence against this argument for semi-strong market efficiency (and some the opposite direction that private information is impounded in the current price). But, these studies find the inefficiency is not exploitable. And, obviously, if one found a way to exploit those inefficiencies, others would copy. This is why a majority of my non-retirement and all my retirement savings are in broad-market etfs and funds. I laugh at those who pay 1% or more on AUM to advisors, when the clear-cut evidence is they don't beat the market regularly in the long-run particularly when one deducts the management fees.* Still, is Buffet just a statistical outlier? Everybody wishes they invested in Berkshire decades ago.

*My observation relates to advisors managing low 8-digit portfolios and less. Things might be different with 9-plus-digit portfolios---I don't know.

@This comes to mind

Regulation Fair Disclosure (Reg FD), adopted by the SEC in August 2000 and effective October 2000, prohibited companies from selectively disclosing material non-public information to favored analysts, investors, or others without simultaneous public release. It aimed to level the information playing field.

Prior to that, Buffet had about double the performance of the market. After that, his edge totally disappeared.

Source: 2/14/26 episode of the All-In Podcast

@This comes to mind

Regulation Fair Disclosure (Reg FD), adopted by the SEC in August 2000 and effective October 2000, prohibited companies from selectively disclosing material non-public information to favored analysts, investors, or others without simultaneous public release. It aimed to level the information playing field.

Prior to that, Buffet had about double the performance of the market. After that, his edge totally disappeared.

Source: 2/14/26 episode of the All-In Podcast

Great, more chum in the water for Tim Dunn.

Here we go!