Earlier this week, I wrote about the various rental car collision coverage options offered by some of our favorite credit cards. Naturally, plenty of questions came up around what it looks like to actually file a claim, and rightly so. It’s one thing to know that the resources exist, it’s another thing entirely to trust the process in the event that something happens.

So I figured I could break down the mechanics of various programs, but what fun would that be?

Instead, I decided to crash some cars to see what all the fuss was about. 🙂

The scenario

Okay, so that’s not exactly what happened, but I came pretty close to that last summer. In all honesty, up until recently, I was a sign-up bonus, status-waiver-chaser with a side of lounge access credit card user. In other words, I had never even considered the travel protections offered by different cards.

And then August happened.

The month started with a hit-and-run in my personal vehicle (they hit, they ran) the week before I left for a two-week trip to California.

On my first full day there, I lost a set of rental car keys on the beach, and had to get towed 45 miles to the nearest airport Hertz repair center.

Two days later, I had about $1,000 worth of luggage and camping gear stolen out of my replacement car.

Just to round out the week, I decided to end things by driving my car over a rocky outcropping, doing some serious damage to the bumper.

Needless to say, I was done calling Geico and AAA’s roadside assistance.

Just when I was ready to give up driving for good, my friend suggested (with a mix of “hey I taught you something new,” and “duh Steph, don’t you travel for a living?”) that I check out my credit card’s rental car insurance policy.

I’ll admit, for all of the flying that I’d done, this had never even occurred to me. And thus began my crash course in Chase’s primary rental car collision coverage.

The basics

Most credit cards offer some kind of rental car coverage, but Chase is currently the only company consistently offering primary collision coverage at no additional charge on some of its cards. This basically means that you are covered for any damages incurred to your car, regardless of whether or not you carry other insurance.

You are required to pay for the rental with the credit card in question, and decline the collision insurance, in order for the policy to kick in. I carry my own auto policy and never pay for the insurance that the rental car company offers, and I happened to pay for the car with a Chase credit card as opposed to my usual trusty Delta Amex (for reasons having more to do with the magnetic strip than any actual strategy, in the happiest accident of the year).

So I was set.

Starting a claim

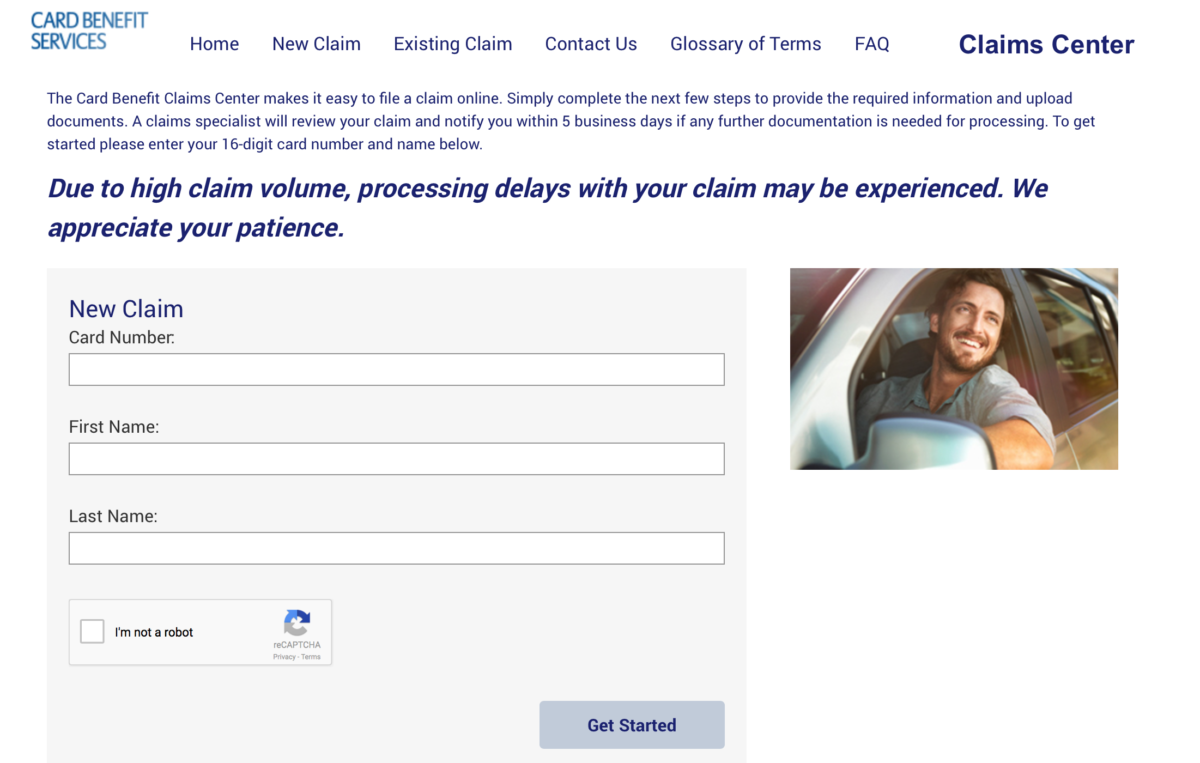

In practice, starting the claim process is more of a chicken-or-egg situation. A quick phone call to the 800 number on the back of my card led me to Chase’s third-party insurance provider, Card Benefit Services, also known as Eclaims Line. (Yes, Eclaims is one word. No, there’s no hyphen. Yes, I’m also twitching.)

I was hoping to start the process as soon as possible, but they can’t really get the ball rolling until you have a copy of the repair estimate and final rental car agreement – aka the end of your rental period.

The reality is that you have 60 days from the date of the incident to file the claim, which should be no trouble for most travelers. (Some cards require a 45-day window, though, so careful!)

In the meantime, I swapped my rental car for a new one (again), incurred a few weird looks from the Hertz reps at SFO, and patiently waited in claim limbo while driving very carefully around the Bay Area until the end of my trip.

The nitty-gritty

Once everything was wrapped up with my final rental car contract and Hertz sent me away (probably hoping to never see me again), it was time to roll up my sleeves and get the paperwork in.

Starting a claim is pretty straightforward:

Here is a list of the documents that they requested:

- A copy of the incident or accident report from the rental agency.

- A copy of the Demand Letter (document from the Rental Agency outlining their payment mailing address, claim reference number, and all damage charges and/or expenses for which they are seeking reimbursement).

- The Final Rental Agreement verifying the return of the vehicle and the final rental charges.

- A copy of the monthly billing statement (showing the last 4 digits of the card number) verifying the charge for damage to the rental vehicle.

- Photographs of the damage to the rental vehicle, if available.

- A copy of the Itemized Statement of Repair(s) or Final Repair Bill from the rental car company for repairs made to the rental vehicle.

- A copy of the travel package, prepaid voucher, and a copy of your travel package invoice.

I realize that this list may induce memories of applying for a mortgage (or adopting a child) and the story probably would have ended here if it weren’t for Hertz’s claims management process.

To their end, Hertz also contracts with a third-party provider, Viking Billing Services, and after ten minutes on the phone with a very cheery Tim, I received everything I needed to file the claim, including the photographs of the damaged vehicle. The only things he couldn’t provide were my credit card statement and travel package invoice, which I had on my end.

I did have to pay for the damages on the spot, which is always a little disconcerting, but he assured me that as long as I filed his paperwork back to the insurance provider, I would have a check in hand before the next billing statement.

The final paperwork

Just to add insult to injury, the internal Eclaims upload system kept crashing, so everything had to be emailed in. Despite my fears of a black hole after seeing the dreaded generic email address, everything went through just fine, as long as I included the claim number in the subject line.

One final email correspondence later (apparently you get some attention when you have to exchange cars multiple times on the same rental) and we were back in business. By early October, I had a check in hand for the amount of $943.59. (I even got to keep the United points, and was $943.59 closer to my Premier Qualifying Dollar spend waiver.)

I’m not a huge advocate of manufacturing spend, but if that’s your strategy, I’m sure there are easier ways to do it.

So, in summary, the timeline looked something like this:

- August 17th – Get into fender bender, call Chase

- August 22nd – Officially open claim

- August 26th – Return car

- September 12th – Get phone call from Viking (Hertz), send documents to Eclaims

- September 26th – Follow-up “Why are there additional charges from Hertz?” (because lost keys) email exchange.

- October 5th – Claim is closed

- October 11th – Check in hand

Some lingering questions

I realize this is a (slightly ridiculous) personal experience of how the process works, and the narrative is certainly not exhaustive, so I wanted to address a few questions that may still be out there:

Did you try to use the insurance for the key replacement?

No. Lost keys aren’t covered in the inclusions of any of the policies I’ve looked at (technically, they’re not listed under the exclusions, either, although I’m sure that’s an angle that no insurance would buy). More importantly, trying to file a claim retroactively for something that probably wouldn’t fly was frankly just not a priority.

In case you’re wondering, it was a $250 fee, plus towing.

How about for the stolen items?

Technically no – there was no damage to the car (I think I had a faulty key FOB), and only the cost of the vehicle itself is covered under collision damage. If you have stolen goods in your vehicle, you may be able to get coverage through renter’s or homeowner’s insurance, although the deductibles are usually quite high.

(Incidentally, American Express has a rider indicating that they cover lost or stolen property, but their default insurance only offers secondary coverage, so I probably would have still come out behind).

Was your insurance company contacted at all?

Not at all – Geico even lowered my rates for the next billing period. Bless them.

How about Chase? Any issues with them?

Nope.

What if you had damaged another car?

I probably would have called Geico, cried into my beer and found a side hustle to pay for my newly raised premiums. And still called Chase to get the damages on my car repaired.

Any issues/limitations with swapping cars over the rental period?

Anytime you need to swap out a car, it needs to happen at a location with a repair center, and those are typically found at airports – so I was out of luck with my in-town Hertz. Luckily, they let me swap cars twice with no additional charges. I did get a “you’ve been here before…” though.

Are you even allowed near Hertz locations now?

Remarkably, yes, and they even upgraded me to President’s Club thanks to my Delta status. Figures.

Will you test out Amex’s collision coverage, just for a comparison?

Umm, no. As a matter of fact, I think I’m going to go write about airline wine for a while. 😉

Bottom line

As much as I’m a fan of hands-on learning, having this many rental car situations in a week isn’t something I’d recommend.

Fortunately, I lucked out by using the right credit card, which made the entire ordeal much less complicated (and significantly less expensive) than had I been working with my own insurance.

Has anyone else out there had to use their collision damage waiver? How did the process go for you?

Hi Steph

Do you have experience or advice to offer regarding the appeal of a CDW claim denial by Chase Explorer Card? Rented a large van in Los Angeles that had seats removed in the rear and CDW is denying based on type of vehicle and they are classifying as a cargo van. I scratched the side of it and now they want $5,000.

Thanks for your help!

Karen

Steph, Great writing and a good addition to OMAAT. Our experience in renting at FMC was where we neglected to photograph the entire van. There was a minor scuff on one corner of the bumper we didn't give it another thought but we should have gone back to the rental counter to share this info. The folks at Eurocar tried to bill us for $750 in damages for what could be buffed out. My friend...

Steph, Great writing and a good addition to OMAAT. Our experience in renting at FMC was where we neglected to photograph the entire van. There was a minor scuff on one corner of the bumper we didn't give it another thought but we should have gone back to the rental counter to share this info. The folks at Eurocar tried to bill us for $750 in damages for what could be buffed out. My friend did the rental so I'm not sure how he paid but suffice to say they wanted him to pay up. He never did pay but it was an object lesson, photograph the vehicle and delete after the rental has terminated if necessary.

I'm very glad I read this article. I'm on my way to Australia, Fiji and New Zealand (LOTS of award travel and award hotel nights yippee! First class over on Qantas, Business back on Singapore). I'm renting a car in NZ for two days to drive to the Shire and for a two night farm stay. I called Chase to make sure the rental car insurance coverage was in effect there. It is. BUT the...

I'm very glad I read this article. I'm on my way to Australia, Fiji and New Zealand (LOTS of award travel and award hotel nights yippee! First class over on Qantas, Business back on Singapore). I'm renting a car in NZ for two days to drive to the Shire and for a two night farm stay. I called Chase to make sure the rental car insurance coverage was in effect there. It is. BUT the Chase rep let me know that New Zealand has a law that you must purchase insurance coverage even if it is covered by your cc.

I also thought it would be a good idea to call my own insurance company (GEICO) just to make sure I would be covered and I found out they do not cover anything outside of US, US territories and possessions, and Canada.

I'm now much more prepared and I will simply purchase the needed and required coverage to augment the Chase coverage. Thanks again for this article.

I have had to use the Chase Collision Damage insurance twice—both times in Iceland. One year we had two flat tires a day apart. This meant two separate claims and two separate paper trails to repay me for fairly inexpensive patch jobs. We had a mid sized SUV. Card Benefit Services spent what must have been a fortune to get the repair documents translated but I got my reimbusement (about $60 total).

The next year...

I have had to use the Chase Collision Damage insurance twice—both times in Iceland. One year we had two flat tires a day apart. This meant two separate claims and two separate paper trails to repay me for fairly inexpensive patch jobs. We had a mid sized SUV. Card Benefit Services spent what must have been a fortune to get the repair documents translated but I got my reimbusement (about $60 total).

The next year we decided that a Toyota Landcruiser would be safer on the rough Icelandic terrain—we visit every year for pleasure and professional reasons. When we returned the car to Hertz, they spotted a dent that was clearly made by a hit and run while it was parked. Tourists are subject to an increasing amount of resentment - especially in Reykjavik. We submitted a claim and had to fight for reimbursement. The claims adjuster classed a Landcruiser with “luxury and exotic vehicals”—like Lamborghinnis. Card Benefit Services doesn’t insure that type of car. Landcruisers aren’t listed in the insurance documents as that type of car but I guess they tried to give it a shot. After some back and forth when I explained that Landcruisers were common in Iceland and necessary on rough roads and foul weather, they relented and I was reimbursed.

I've used AMEX twice, but I pay extra for it to be primary coverage. Both times I just called them, even before I turned my rental in, and they took care of the rest. In fact, for 1 accident the Hertz rental station in Oslo wouldn't talk to AMEX to process the claim, and charged my card for the damage. AMEX processed their own chargeback and wouldn't pay Hertz.

I have to say I'll probably stay with AMEX if possible from the Chase description.

I'm having a problem with Europcar Argentina since December 2017, I had an accident and since I didn't pay for insurance, they required a deposit of $1.100 and after returning the car they took the $1.1k as a guarantee to cover the cost of the repairs.

I started the process with Eclaim but the rental car company doesn't want to provide any document (repair cost etc), so even if you use a CC (CSR in...

I'm having a problem with Europcar Argentina since December 2017, I had an accident and since I didn't pay for insurance, they required a deposit of $1.100 and after returning the car they took the $1.1k as a guarantee to cover the cost of the repairs.

I started the process with Eclaim but the rental car company doesn't want to provide any document (repair cost etc), so even if you use a CC (CSR in my case) doesn't mean they will cover the cost of the repair if the rental company decided not to provide any kind of documentation.

I had a Hertz rental broken into in L.A. last year. Paid with CSP and Eclaims covered the damage to the window. Surprisingly nothing was stolen.

@RCB, I agree with @Kyle. I don't think it is unreasonable for them to ask for a big deposit when they are letting you borrow a $20k+ item and know you will be leaving the country shortly after return. I had the same thing happen to me at Sixt...

I had a Hertz rental broken into in L.A. last year. Paid with CSP and Eclaims covered the damage to the window. Surprisingly nothing was stolen.

@RCB, I agree with @Kyle. I don't think it is unreasonable for them to ask for a big deposit when they are letting you borrow a $20k+ item and know you will be leaving the country shortly after return. I had the same thing happen to me at Sixt in Croatia. They wanted ~$6k deposit and I said fine. The tried to run my credit card and it was denied with two cards (CSP and Citi Prestige, both with plenty of credit limit). I gave up and bought their insurance since it was just a one day rental. I later charged back that insurance charge after finding out that Chase and Citi had no record of an attempted transaction on their end. It was Sixt's own system that didn't let the charge go through. I won that chargeback.

So interesting situation I had this winter, I damaged a minivan but used my Chase card and initiated the claim. The Eclaims people were helpful but told me that my state law (Minnesota) was that it had to be run through my primary car rental insurance 1st, they couldn't act as the primar. I was bummed about that but Eclaims is reimbursing the deductible. Anyone else have this experience?

Steph - great writing, and wonderfully useful couple of posts. You managed to be off in your timing by about a week - I just got back from L.A., where I rented a car, and had to do all this research into coverage myself. Luckily I didn't get into any accidents, but I did fail to find where I had parked my car at the beach for about 10 minutes, thought it was stolen, and...

Steph - great writing, and wonderfully useful couple of posts. You managed to be off in your timing by about a week - I just got back from L.A., where I rented a car, and had to do all this research into coverage myself. Luckily I didn't get into any accidents, but I did fail to find where I had parked my car at the beach for about 10 minutes, thought it was stolen, and started thinking about who I would call and how I'd deal with the credit card claims line. I don't own a car myself (I live downtown in a large city) and therefore have no primary insurance, so I paid with my Amex and refused the car company's theft and collision insurance, which (at least I presume, since I luckily didn't have to test this out) means the Amex insurance kicked in. So my sense is that for people who don't own cars/have primary insurance, it probably doesn't much matter if they use Chase or Amex since they have no primary insurance to begin with.

Great info. Thanks for the insight by sharing your experience! It really re-affirms my main motive for keeping the Explorer Card.

I have recently been through this process and did feel like VCS was holding the paperwork necessary for the claim hostage until I was willing to pay the claim on my credit card. I had originally wanted the insurer to pay VCS directly, but quickly realized that putting the claim on my credit card would expedite the process and it did, I was refunded only a few days later. If the amount of the claim...

I have recently been through this process and did feel like VCS was holding the paperwork necessary for the claim hostage until I was willing to pay the claim on my credit card. I had originally wanted the insurer to pay VCS directly, but quickly realized that putting the claim on my credit card would expedite the process and it did, I was refunded only a few days later. If the amount of the claim is well within your credit limits, then you should do that, and you will receive points for it. Too bad it didn't code as travel :(.

@RCB, you can still use the CC insurance, just accept the rental company's deposit charge. Hertz in CPT did this and it was just like a $5,000 hold on my card. No biggie, it got cleared after I returned the car.

So much interest on this topic, sounds like everyone needs to learn to drive better.

@Garrett Chase just told me you have to pay for the rental on your card. It doesn’t matter how you pay for the damage surcharge. They also did not ask me for proof that I actually paid it.

lol @ decided to go crash some cars. +1 for you. So, you had to pay the credit card bill with the damage charges on it in the meantime, right?

Very good article. Great info. Glad you got everything sorted out.

This was great :) I've always used my CSR for rentals, mostly because points, but I always had the coverage in the back of my head as an extra bonus. Luckily I haven't had to use it, but it's very reassuring to hear an account of it working!

@TravelinWilly - Thank you! I think three years of reading Tiffany's writing on a regular basis has helped my newfound blogging career significantly.

@Robert - Nice! Bear in mind that *some* countries are excluded on certain cards, so if they give you any grief, you may want to double-check the fine print on your terms and conditions. Good luck, let me know how it goes!

@Steve - AMEX's default coverage is secondary (unless...

@TravelinWilly - Thank you! I think three years of reading Tiffany's writing on a regular basis has helped my newfound blogging career significantly.

@Robert - Nice! Bear in mind that *some* countries are excluded on certain cards, so if they give you any grief, you may want to double-check the fine print on your terms and conditions. Good luck, let me know how it goes!

@Steve - AMEX's default coverage is secondary (unless you buy up to their primary coverage), which meant I would have to go through my auto insurance first, and risk a higher premium if I file a claim. They do offer some nice benefits though, depending on your card, including towing (as you mentioned) and coverage for lost/stolen items. I've driven a few...past their prime...cars in my day, so I'm basically loyal to AAA for life.

Jon:

your car insurance covers you regardless of who you rent from, read your policy.

This article literally just saved me $600. I damaged a rental car last week in Italy and had no idea about this benefit. Just submitted a claim online!

Assuming you have one did you check the benefits on your Amex card? Some of them include free towing (for example the one offered by Morgan Stanley). It's a great benefit but very few people even seem to be aware of it, probably because it's isn't included across all Platinum cards but depends upon the issuer.

Sorry Tiffany, but James and Steph are giving you a run for your money in terms of brilliant writing! You're still tops, but you really do have stiff competition here now. :)

@Steph - Another great, engaging blog post, thank you.

@ TravelinWilly -- That's the best possible compliment, thank you.

Glad your US experience went well. We use the AMEX rental coverage when we rent, the $25 one. AMEX was great the one time we had to use it from “claimed” damages to the wheel covers from a car rented in Germany. At first, Hertz Germany refused to work with Amex insurance, then when they finally did (we had to get Hertz US involved), they sent pictures showing scratches that were different from the scratches...

Glad your US experience went well. We use the AMEX rental coverage when we rent, the $25 one. AMEX was great the one time we had to use it from “claimed” damages to the wheel covers from a car rented in Germany. At first, Hertz Germany refused to work with Amex insurance, then when they finally did (we had to get Hertz US involved), they sent pictures showing scratches that were different from the scratches they showed me on the return (the ethics of rental car companies in Germany could an entirely different review). In any case, Amex stood with us and settled the claim. The lesson for us has been, stick with Amex and avoid Hertz, at least in Europe.

"And thus began my crash course in Chase’s primary rental car collision coverage."

"crash course" - good one!

I remember that week, and watching you hit the “rocky outcropping”. All I could do was put my head in my hands and curl up in the fetal position.

So glad that it all worked out and that your card covered it all. I hope to never need the advice put forth in this article.

Steph: Could you or someone at OMAAT dive deeper in reference to liability coverage outside of the US? Our US insurance coverage handles liability coverage within the US. This would include damage to other property, people, vehicles and/or injuries to anyone in the rental car you drive. The Sapphire Reserve CDW covers all damages (to rental car) however; their exact quote on what is NOT COVERED is "Injury of anyone or anything inside or outside...

Steph: Could you or someone at OMAAT dive deeper in reference to liability coverage outside of the US? Our US insurance coverage handles liability coverage within the US. This would include damage to other property, people, vehicles and/or injuries to anyone in the rental car you drive. The Sapphire Reserve CDW covers all damages (to rental car) however; their exact quote on what is NOT COVERED is "Injury of anyone or anything inside or outside of the vehicle." We all assume we have complete coverage when using our credit cards or personal insurance when traveling. WE ARE INCORRECT in this assumption. Thank you for your assistance

steph, very good writing, tone, speed. very nice real.

Does Chase cover Silver Car rentals? I know some policies exclude "luxury cars" and sometimes the A4 is considered a luxury car

@ Ian -- I can confirm firsthand that they do (unfortunately have been in an accident in a Silvercar).

Witty and informative!! We want more steph

@Jared - Nice! It sounds like AMEX has their own internal carrier, which I imagine makes things much easier. For the record, I think most cards (including some bank-issued cards that we don't talk about on here) rely on Eclaims.

@Tennen - Good question - in layman's terms, they just wanted a copy of the Priceline receipt.

@FMLAX - Thanks for making me genuinely LOL this morning!

@DCJoe - Sounds...un-fun, in every...

@Jared - Nice! It sounds like AMEX has their own internal carrier, which I imagine makes things much easier. For the record, I think most cards (including some bank-issued cards that we don't talk about on here) rely on Eclaims.

@Tennen - Good question - in layman's terms, they just wanted a copy of the Priceline receipt.

@FMLAX - Thanks for making me genuinely LOL this morning!

@DCJoe - Sounds...un-fun, in every respect. Good info, though.

@Sheena - Good call - tires are a pretty common exclusion among these policies to begin with. Glad it worked out for you!

I had to file a claim with Card Benefit Services after I was hit in a parking lot in LA. As I had rented the car directly through Avis, I had to supply a copy of the master rental agreement showing that I used my Chase Sapphire card to secure the reservation. As I am an Avis preferred member, I simply go to the car and drive off. A copy of the “contract” is in...

I had to file a claim with Card Benefit Services after I was hit in a parking lot in LA. As I had rented the car directly through Avis, I had to supply a copy of the master rental agreement showing that I used my Chase Sapphire card to secure the reservation. As I am an Avis preferred member, I simply go to the car and drive off. A copy of the “contract” is in the car upon arrival. The contract simply stated that I had used a Visa card to secure the reservation, and the identifying information (last four digits) of the card was not noted on the form.

This led to much difficulty in getting the accident covered... Eventually after many phone calls to Avis, I spoke with a customer service rep who was reluctantly willing to provide Card Benefit Services with a letter confirming my use of the Chase Sapphire card to hold the reservation. The insurance ultimately covered the claim which was over $800.

Whenever I rent a car now, before driving off I make sure I have a document which displays proof of the card I used to secure the rental. If renting in the traditional way (going to the desk, signing paperwork and having them hand you the keys) this most likely would not be an issue, but if you are using a preferred program such as this it is important to check it out before driving off the lot.

Little thing many people don’t know: a lot of times you can rent a car through your car insurance... they have a corporate code for you to attach to your Hertz/Alamo/Enterprise/Sixt/whatever account. In my case, if I use that code and rent it, I still get Hertz points, I still get rent through Hertz directly, but my car insurance actually covers the rental car. Just something to look into if you rent regularly. Mine also...

Little thing many people don’t know: a lot of times you can rent a car through your car insurance... they have a corporate code for you to attach to your Hertz/Alamo/Enterprise/Sixt/whatever account. In my case, if I use that code and rent it, I still get Hertz points, I still get rent through Hertz directly, but my car insurance actually covers the rental car. Just something to look into if you rent regularly. Mine also offers extra coverage for a few bucks a month, and issues with my cars have always been resolved expediently- including swapping cars. I’ve had Hertz come pick up their car and drop me a new one, in lieu of dropping it off at a rental center, even if there were damages or mechanical issues.

Also, if you don't own a car and want to get "non-owned" liability coverage for when you drive rental cars/Zipcar/etc, this agent in New York is very good.

http://campbellsolberg.com/

Found them through this excellent AutoSlash post:

https://www.autoslash.com/blog-and-tips/posts/a-quick-primer-on-car-rental-insurance

I haven't used the CDW with my credit card, but I did get insurance coverage on a rental car in the UK last year...sooooooo glad I did. I apparently scuffed the tires a bit trying to drive and park, and they wanted to charge me for 4 new tires. (For the record, they were not bad at all...those scammers at Enterprise have quite the operation going at Heathrow.) I've never been more relieved to have...

I haven't used the CDW with my credit card, but I did get insurance coverage on a rental car in the UK last year...sooooooo glad I did. I apparently scuffed the tires a bit trying to drive and park, and they wanted to charge me for 4 new tires. (For the record, they were not bad at all...those scammers at Enterprise have quite the operation going at Heathrow.) I've never been more relieved to have them ask about insurance on the vehicle and be able to say..."Enterprise insurance, so here's the keys...bye!"

In case you all are wondering, the Chase eclaims system does not pay out for cleaning fees charged by a rental car company. Last summer my son threw up in a rental car a few days before we returned it. We cleaned up everything as best we could, but there was some staining on the floor and seat, and the smell was still slightly there. They charged us a 100 euro cleaning fee (pretty reasonable,...

In case you all are wondering, the Chase eclaims system does not pay out for cleaning fees charged by a rental car company. Last summer my son threw up in a rental car a few days before we returned it. We cleaned up everything as best we could, but there was some staining on the floor and seat, and the smell was still slightly there. They charged us a 100 euro cleaning fee (pretty reasonable, actually). Wasn't sure if it would be covered by the Chase insurance, so I filed a claim to see- first time ever.

They said since there was do damage or repair to the car, they couldn't pay anything out. Sounds like the same reason they wouldn't pay for your key replacement fee.

“A copy of the travel package, prepaid voucher, and a copy of your travel package invoice.”

Call me dense, but I have no idea what this is. I’m guessing it only applies to those who book their car rentals via TAs or OTAs?

In any case, sorry that you had to go through such an ordeal. It’s definitely not something you’d want anyone to have to deal with... :-(

"I probably would have called Geico, cried into my beer and found a side hustle to pay for my newly raised premiums."

*Looks at OMAAT*

Seems like you've done it already! :D

Loved your writing Steph.

In short, I have used the AMEX insurance coverage in Trinidad. The process was easy. A simple phone call was all that was needed to start the process. AMEX worked directly with the Hertz rental. Just ensure that all transcripts of conversations are kept.

@Andy - Wow! You've got me beat! Did you buy a lottery ticket?

@Sam - When I was filing, I vaguely remember there being an option at one point to have the billing company go directly through the insurance. I didn't go that route, because I was warned that it would be more cumbersome, but I remember it coming up in conversation.

@RCB - Did you take a print copy of your policy along? Not necessarily a solve, but it may help. My dad had the same...

@Sam - When I was filing, I vaguely remember there being an option at one point to have the billing company go directly through the insurance. I didn't go that route, because I was warned that it would be more cumbersome, but I remember it coming up in conversation.

@RCB - Did you take a print copy of your policy along? Not necessarily a solve, but it may help. My dad had the same thing happen to him recently in Frankfurt (they always take it at the airport, but didn't at the off-airport shop, for example...)

Great article, and good information regarding the process!

I’m in Chile right now and the car rental place refused to accept my Chase insurance plan unless I paid them a $2,000 deposit. In Paris the deposit demand was $5,000. Makes me so aggravated when I have the best insurance on the market and can’t use it.

@DaninMCI Her previous post on credit card rental car coverage did make clear the need to carry liability insurance (the stuff you legally must have if licensed to drive). If the only damage is under collision or comprehensive (ie, you are not at fault or you hit a stationary object like a curb/rock), the advantage of using (primary) credit card coverage is that your "real" car insurance company need never know = continued "claim free"...

@DaninMCI Her previous post on credit card rental car coverage did make clear the need to carry liability insurance (the stuff you legally must have if licensed to drive). If the only damage is under collision or comprehensive (ie, you are not at fault or you hit a stationary object like a curb/rock), the advantage of using (primary) credit card coverage is that your "real" car insurance company need never know = continued "claim free" discounts.

Fortunately, the only time I ever experienced damage in a rental car was when my father was driving it, and I had made sure he was on the rental agreement as a driver so there was really no issue (for me) -- ironically, it was a loaner after my car was hit so I hadn't actually paid for the rental to begin with.

Anyone know what happens if your damage amount exceeds your credit climit? If you have to by other means then card that prefers your policy for this reason, is that an issue?

I have used the Chase car insurance three times (twice with my United Explorer and once with my Ink) for rentals in the UK when high roadside kerbs got the better of low profile tires and alloy wheels. Very straight forward process. On one occasion "administrative" charges were not reimbursed and also once I actually made money as the exchange rate changed between the time the damage was charged on the card I got the...

I have used the Chase car insurance three times (twice with my United Explorer and once with my Ink) for rentals in the UK when high roadside kerbs got the better of low profile tires and alloy wheels. Very straight forward process. On one occasion "administrative" charges were not reimbursed and also once I actually made money as the exchange rate changed between the time the damage was charged on the card I got the reimbursement check. The car insurance is the main reason I keep a United Explorer card in my wallet

I appreciate Steph's attitude, and writing voice -- the voice is different from Lucky's, but still quite pleasant to read. In both cases, I feel encouraged to read to the end!

And of course it contains very useful specific tips for us to remember whenever we damage a rental car.

In my case, after my son slid Hertz's Chevy into a snowbank, my USAA card covered the (total) damages, but Hertz still blackballed me for several years.

Most auto policies do provide coverage while driving a rentalnor borrowed car in the USA and some include Canada. The real gap is if you are injured or you injure someone else no matter what card you have.