The major credit card issuers have various policies in place to crack down on those who apply for credit cards exclusively for welcome offers. While credit card issuers sometimes have big bonuses to get customers to apply, they do so with the hope of people holding onto a credit card long term. While it’s understandable that sometimes a card might not work out for someone, those who constantly open and close cards may find themselves facing some restrictions.

In the case of American Express, the issuer has a policy of only letting cardmembers earn the welcome offer on a card “once in a lifetime” (this is one of several Amex rules, along with things like the five card limit). Anecdotally, a “lifetime” in this context typically refers to a period of around seven years, though that policy isn’t published. So if you’ve had a card before, you won’t generally be eligible for the welcome offer on the card again.

In the case of American Express, there’s a pop-up that shows up during the application process for some people, and in this post I’d like to talk about how that works.

In this post:

What is the Amex application pop-up warning?

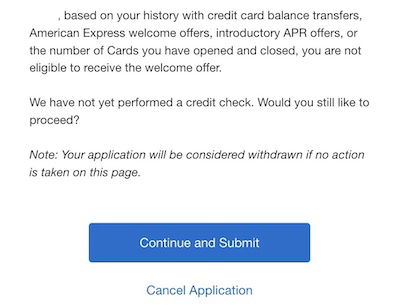

During the American Express application process, you might see that you’re faced with the following pop-up:

Based on your history with credit card balance transfers, American Express welcome offers, introductory APR offers, or the number of Cards you have opened and closed, you are not eligible to receive the welcome offer.

We have not yet performed a credit check. Would you still like to proceed?

Note: Your application will be considered withdrawn if no action is taken on this page.

This will typically appear after you enter your personal information and submit your application. As the message states, there’s the potential that you won’t be eligible for the welcome offer on the card that you applied for.

This means you could still apply for the card and simply not receive the bonus. But this also gives you the option to cancel your application, so that there’s no credit pull (separately, Amex also has an awesome “Apply with Confidence” feature on some cards, which tells you if you’re going to be approved for a card before there’s a credit pull).

What causes the Amex application pop-up warning?

There are several reasons you could potentially be faced with this pop-up warning during the application process.

You could get this message because you’ve applied for a particular card in the past, and just didn’t remember. In this case I’d consider the message to be genuinely helpful and a great feature, since you’re able to avoid a hard pull for a card where you won’t get the bonus.

Under other circumstances this can be a bit more confusing, though. The warning officially states that you could be ineligible due to one of four reasons:

- Your history with credit card balance transfers

- Your history with Amex welcome offers

- Your history with introductory APR offers

- Your history with the number of Amex cards that you’ve opened and closed

Suffice it to say that this is vague. What does all of this mean in practice? I’d say the most likely reasons you’d be faced with this message is the following:

- Even though you may technically be eligible for a welcome offer based on not having had that exact card before, Amex may decide that you’ve had too many cards in that same card “family,” and maybe canceled too many of them too quickly, didn’t spend enough on them, etc.

- Maybe Amex feels you have opened and closed too many cards with the issuer, and/or haven’t spent enough on the cards for it to make sense to approve you for another bonus

- If you’ve engaged in any sort of other behavior that Amex frowns down upon, Amex may decide not to offer you a welcome bonus on a particular card

One other interesting twist is that sometimes these pop-ups are specific to certain “families” of cards. In other words, you may get this message when applying for a Hilton Honors Amex you’ve never applied for before, while you may not get this message when applying for an Amex Platinum Card.

How common is it to see the Amex pop-up warning?

It’s always hard to know just how common these kinds of pop-ups are, especially since those of us into miles & points are obviously among those most likely to be targeted by these restrictions.

I think most of us can understand why Amex would want to restrict people who repeatedly open and close cards, without keeping them for a long time and spending money on them. However, I’m increasingly seeing data points of people getting this warning even though they only have a few Amex cards, have had them open for years, have never even had a card in the same family, etc.

So while I don’t have an explanation as to what is causing this, know that you’re not alone if you’re finding yourself getting the pop-up warning even if you’re a good Amex customer.

Is there any way to get around the Amex application pop-up warning?

If you’re faced with this pop-up during the application process, is there anything you can do? Yes and no.

No, there’s no one you can (realistically) contact to appeal this warning, and there’s no way that you’ll get this removed from one minute to the next. For whatever reason Amex has decided you shouldn’t be eligible for a welcome offer on a particular card, and that’s that.

The good news is that just because you get this message once, doesn’t mean you’re locked out of earning welcome offers forever. While there’s no magic formula, here are some things to consider doing:

- Avoid applying for Amex cards for some significant amount of time (maybe a few months, at least); I’d assume Amex is tracking how often people apply for cards, so don’t submit an application every few days to see if the pop-up still shows up

- If you have a lot of open Amex cards you’re not spending money on, put some spending on those cards to show some activity

- Since these restrictions are often specific to “families” of cards, after a few months maybe try applying for a card in a different “family,” to see if you have the same message (it’s also possible you might not get a message like this if you applied immediately for a different card, but I’m trying to recommend a conservative approach here)

Like I said, there’s no consistent way to get this resolved. Assuming you’ve never had a particular card before, Amex has probably decided that something about your current relationship with the company isn’t ideal, and try to adjust things accordingly.

Bottom line

Amex has a pop-up warning during the application process, which will tell you if you’re not eligible for the welcome offer on a card, prior to even pulling your credit. This is helpful if you’re not sure if you’ve had a card before, given Amex’s “once in a lifetime” application rule.

But Amex isn’t just using this pop-up in situations where you’ve had a particular card before, but also sometimes in situations where the issuer has simply decided that you shouldn’t get the bonus on a card. This can happen for a variety of reasons, and the best way you can deal with it is by continuing to spend responsibly on your Amex cards, and not applying for other Amex cards for a while.

Have you ever dealt with Amex’s pop-up warning? If so, what was your experience?

If you're not approved for a MR card, try a hotel branded Amex instead

"Join" the morons , and "Pay" the fees . Morons' problems .

It’s funny how un-self-aware you are, and how devoid of any sense of irony in what you write.

Never stop posting.