The waitlist has opened for the new X1 Credit Card, which is expected to launch in winter 2020. This card seems like a hybrid between Brex and the Apple Card, and I’m equal parts intrigued and skeptical. I can’t help but think that the card might just be too good to be true, and wonder how it’s sustainable…

Let’s go over some of the card basics…

In this post:

Earning points with the X1 Card

The X1 Card will offer anywhere from 2-4x points per dollar spent:

- Earn 2x points on all purchases

- Earn 3x points on all purchases in a year when you spend at least $15,000 on the card in that year

- Earn 4x points for 30 days when you refer a friend to the card, and they get the card; there’s no limit to how many people you can refer, and the person referred also earns 4x points for 30 days

There’s no limit to how many points you can earn, and points never expire.

Redeeming points with the X1 Card

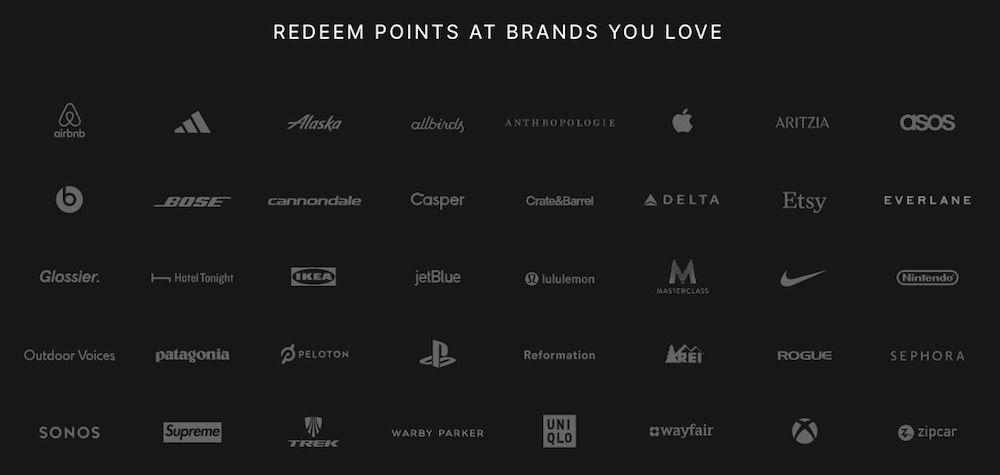

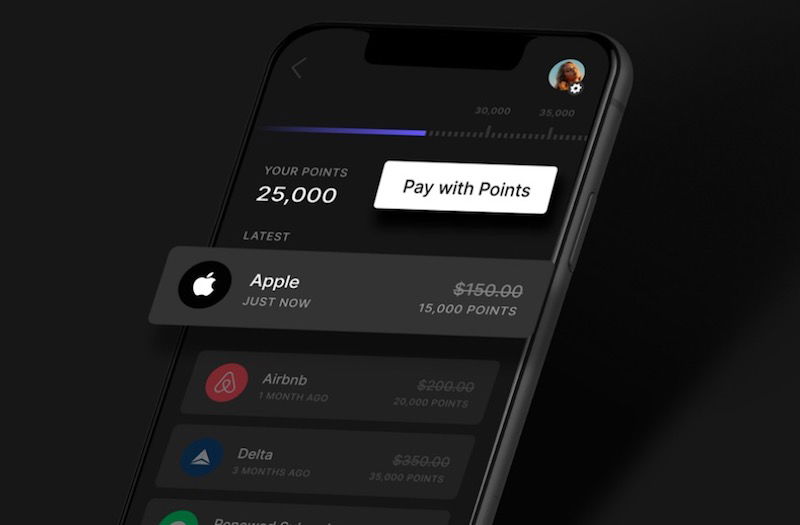

It’s great that you can earn 2-4x points per dollar spent with the X1 Card, but how can those points actually be redeemed? Well, they can be redeemed towards purchases with over 100 retailers.

The redemption value varies:

- At a minimum you can redeem points for one cent each towards purchases with partner retailers

- In some cases you’ll be able to redeem points for up to two cents each towards purchases

- We don’t yet know which retailers will get which redemption value

In other words, the card offers the equivalent of 2-8% back, depending on which earnings tier you fall in, and also depending on which retailer you’re redeeming with.

It sounds like when you redeem your points you don’t actually have to book through a portal, or anything, but rather you can offset the cost of a purchase that you’ve already made.

No annual fee & no foreign transaction with X1 Card

The X1 Card will have no annual fee and no foreign transaction fees. There aren’t many rewarding cards that have both no annual fee and no foreign transaction fees, so that’s awesome.

No hard pull & different approach to credit lines with X1 Card

When you apply for the X1 Card there will be a soft pull from your credit report, rather than a hard pull.

Along those lines, there will also be a different process than usual used to determine your credit limit, and you could find that it will be up to 5x higher than with traditional credit cards:

- Your credit limit will be based on your current and future income

- To have your limit increased you can link your bank account and provide pay stubs

- Your credit limit can automatically increase over time

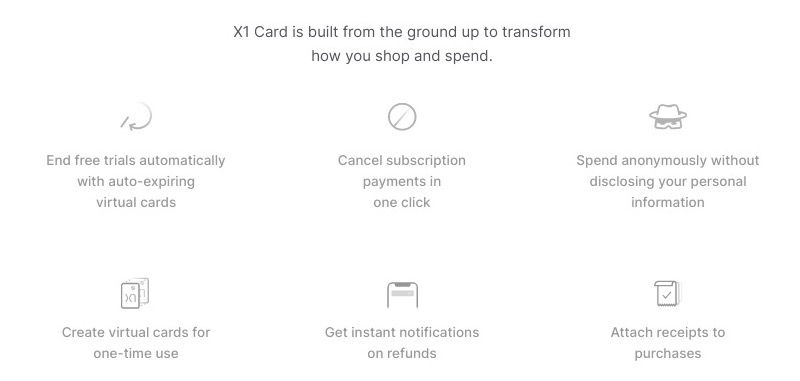

Other X1 Card features

There are some other X1 Card features worth being aware of, which personally don’t make a difference for me one way or another, but others might find them to be interesting:

- You can create auto-expiring virtual cards that allow you to cancel free trials automatically

- You can cancel subscription payments with one click

- You can use an incognito mode to shop anonymously

- You can receive instant notification of refunds

- This will be a Visa Signature Card, so that comes with some benefits too

Join the X1 Card waitlist now

While the X1 Card is expected to launch this winter, you can already join the waitlist, which just requires providing your name and email address:

- The benefit is that if you’re referred you’ll receive 4x points for a period of 30 days

- I’m amused by this waitlist concept in general, as it’s clearly a way to create hype, though I’m not sure what it means in practice

- The company claims there are already 160K+ people on the waitlist

- You’re allowed to advance 100 positions on the waitlist if you share your school and employer info, and you advance 500 positions for each person you refer

It seems like it’s worth getting on the waitlist so you can at least be referred, but otherwise there’s probably no rush. Others are welcome to leave their referral links in the comments section.

My take: potentially amazing, even too good to be true?

Let me start by acknowledging that we’ve seen a countless number of credit card startups that never ever actually came to fruition. In this case there are former PayPal and Twitter executives behind the venture, and it’s also allegedly within months of launching. That being said, I’ll believe it when I see it.

Based on what’s being advertised, this card sounds incredible, at least for those spending $15,000+ per year in categories where they wouldn’t otherwise receive a bonus. The card has no annual fee, no foreign transaction fees, and offers 3x points when you spend at least $15,000 per year, and 4x points for periods where you refer someone. Those points can be redeemed with all kinds of retailers, for a value of one to two cents per point.

Obviously cash in your pocket is better than money to spend with retailers, but I’d certainly take 4%+ with a retailer I spend money with over 2% cash back on another card.

For example, I pay my taxes by credit card, and if I could get 4%+ worth of rewards with a retailer for a fee of under 2%, I’d take it.

I will say that for those who don’t spend at least $15,000+ per year, the Citi Double Cash® Card (review) would be my preference long-term, as you earn 1% cash back when you make a purchase, and another 1% cash back when you pay for that purchase (in the form of ThankYou points). Cash in your pocket is better than points to spend with retailers.

What am I missing about the business model?

You know the saying — “if something sounds too good to be true, it probably is.” Generally speaking credit card issuers make money primarily in three ways:

- Merchant fees

- Annual fees

- Financing charges

Historically we’ve seen credit card issuers offer at most 2% of value (give or take) to consumers without an annual fee and without a significant investment requirement. Obviously some cards have offered bonus categories that have given consumers disproportionate value, but the hope is that this is balanced with spending in non-bonused categories.

But what exactly is X1 Card’s business model here?

- Is the company somehow getting significant discounts when consumers redeem points with retailers? I can’t imagine Apple and Delta are giving the X1 Card significant discounts when you redeem your points there.

- Is the X1 Card hoping that its client base is much more likely to finance charges?

- Since it’s tech people behind the card, is this a “build market share at a loss and hope to be acquired” play?

- Is this an introductory offer, and then eventually the value proposition will get much worse?

- Is the primary goal here to just get a lot of data on cardmembers, and leverage that to make money?

I just don’t see where the margins are here, though I’d love if someone could help me understand what I’m missing…

Bottom line

The waitlist is open for the X1 Credit Card, and it should launch this winter. This card sounds extremely intriguing. You’ll be able to earn up to 4x points per dollar spent, and each point can be redeemed for one to two cents towards purchases with a variety of retailers.

On top of that, the card has no annual fee, no foreign transaction fees, and some other innovative features. In many ways the card sounds too good to be true.

You might as well add your name to the waitlist so you’ll earn 4x points for 30 days. In the meantime I’m anxiously awaiting the card’s launch, so we can learn all the details…

What do you make of the concept of the X1 Card?

just got my card today!

:):):)

x1creditcard.com/r/rbEZnLC

referring is caring :) https://x1creditcard.com/r/lcLQvpb

Best referral code ever!!!

https://x1creditcard.com/r/YSgaGkp

Use this link and pay it forward!: https://x1creditcard.com/r/ULIGYL9

x1creditcard.com/r/kI7ouDl

I'm looking forward to the concept behind this card. I hope it's extremely beneficial to everyone who decides it's worth the wait!

Referral code:

https://x1creditcard.com/r/YSgaGkp

x1creditcard.com/r/1bujqWm

Sounds great no credit check need on income and it's a metal card can't wait to get mine

https://x1creditcard.com/r/8OXsK7u

My referral code.

To receive 4x points use this link: x1creditcard.com/r/qzpRM2D

My referral code is PNhszo6 or link below

https://x1creditcard.com/r/PNhszo6

here is my referral code, if you want to use it:

https://x1creditcard.com/r/8upADtR

Used RCA's code, now use mine:

https://x1creditcard.com/r/bmbpgk5

here is my referal code, if you want to use it:

https://x1creditcard.com/r/2LFdSgG

Thanks

Used Mike's code, here's mine

https://x1creditcard.com/r/UhRVC4x

Referral link:

x1creditcard.com/r/IChCg9K

Thank you if you use it

Just signed up with Shane's code. Here is my referral code:

https://x1creditcard.com/r/HT928Wj

Here is my referral

Www.x1creditcard.com/r/idXJzrN

Here is my referral

Www.x1creditcard.com/r/idXJzrN

Just signed up with Charlie's code... Here's mine:

https://x1creditcard.com/r/71VKOnZ

I think the business model is based on data monetization!

Anyway, here’s my referral code btw if anyone wants to use it:

https://x1creditcard.com/r/Buh95BI

Thanks!!

My referral link https://x1creditcard.com/r/0pzU6O6

for 4x, use my bonus code!!:

u6OESDb

https://x1creditcard.com/r/Z44rFue

https://x1creditcard.com/r/qZ6wvJR

https://x1creditcard.com/r/PvdHg1Q

Referral if anyone is interested: https://x1creditcard.com/r/5kID2vX

Thanks!

Paid it forward with Sarav's link!

Here’s my link for those of you that would like to pay it forward to me.

Can’t wait!

https://x1creditcard.com/r/iKHS0SV

Referral Link:

https://x1creditcard.com/r/bXC8JUb

Lol I forgot to post my link!

https://x1creditcard.com/r/A8hOcJV

Just signed up using Shane's referral. Please up using mine. GOD BLESS YOU

You can join the wait list at https://x1creditcard.com/r/qzpRM2D

You can use sign-up code qzpRM2D for immediate 4x points for 30 days

Additionally, you can move up the wait list by answering a few questions after sign-up

Looks like a great card to me; hopefully it actually launches.

https://x1creditcard.com/r/J6hntH8

Thank you for the information and thank you MH for the referral link.

Here's mine, thank you in advance if you use it!

x1creditcard.com/r/eyDpkwR

Thanks interesting read, let's see if it goes live, please find my link :

https://x1creditcard.com/r/esZIXEL

Here we go:

https://x1creditcard.com/r/4s24idP

Consider my signup link please: https://x1creditcard.com/r/6S3tv2G I think people are missing some great benefits of the card. Create a virtual card that disappears when you want it to for such things as trails and one time payments. Put an extra lock on security.

Used John's link

Here is m my link https://x1creditcard.com/r/LwDz2W6

Used John's link.

Here is mine

https://x1creditcard.com/r/LwDz2W6

Thank youTim! Would appreciate if someone could pay it forward for me.

https://x1creditcard.com/r/268mhMl

Thanks for using my referral link: https://x1creditcard.com/r/BEbZZUi

send to your friends and family

https://x1creditcard.com/r/XgZhDrL

try it out and pay it forward

https://x1creditcard.com/r/XgZhDrL

It's the same principle as Revolut. They're free and offer great things other banks/cards don't offer, until they attract a big enough customer base to start charging fees. Of course part of the customer base will walk away after the introduction of fees, but many will stay... Thus the need to create a hype.

Your welcome, and thank you!!

x1creditcard.com/r/dxKftBy

@Ben/Lucky: What about cash back? Are you hooked redeem with the retailers or what's the return for cash back?

You can join the wait list at https://x1creditcard.com/r/qzpRM2D

You can use sign-up code qzpRM2D for immediate 4x points for 30 days

Additionally, you can move up the wait list by answering a few questions after sign-up

My referral link:

https://x1creditcard.com/r/ddnL5xD

Thank you.

Use referral code hyLUxyv or Sign up at the link below for 4x points for your first month! Plus get an additional month and move up the waitlist for every referral you get!

https://x1creditcard.com/r/hyLUxyv

My referral link :)

x1creditcard.com/r/RVay4xZf

Let’s hope they will eventually make their points transferable, then it could be a really nice card.

Thanks for considering my link.

https://x1creditcard.com/r/ZonH3iz

Referral link

Thanks in advance

x1creditcard.com/r/S9OJPUD

I used the code from @HockeyCoachBen - on the off chance you’d like to use mine from among the many here, it’s:

https://x1creditcard.com/r/Tq3GzJy

Thanks in advance if you decide to use it!

Paul

x1creditcard.com/r/q2jFTV2

Here's my referral link - use to receive x4 points for 30 days

https://x1creditcard.com/r/xBxHTGI

https://x1creditcard.com/r/rAwi7xx

You can use this link to get yourself a month of 4x points. It'll also give me a month as well!

I am honestly not sure if I see the value in this. Maybe is a a card for the band conscious. Basically you get 2x-3x back (depending on your spend) that you can redeem for gift cards at major brands (or at least the that is what the redemption image shows). The problem is if you buy tangible goods you can almost always get a better price by not buying through the Brand directly.

...I am honestly not sure if I see the value in this. Maybe is a a card for the band conscious. Basically you get 2x-3x back (depending on your spend) that you can redeem for gift cards at major brands (or at least the that is what the redemption image shows). The problem is if you buy tangible goods you can almost always get a better price by not buying through the Brand directly.

3 cents back (if you spend $15,000) is a decent value, but I think I would still get more value putting my money on the chase Trio of cards and getting ultimate rewards points.

Used Ben’s link. Now here is mine referral link. Thank you.

https://x1creditcard.com/r/ddnL5xD

Use my referral code if you like to get 4X points for the first 30 days.

Link: https://x1creditcard.com/r/NpNxe5n

Code: NpNxe5n

Copy and paste in “sign up bonus”

Used Lisfranc's link. Would appreciate if someone could return the favor!

https://x1creditcard.com/r/b8HsRm4

This seems like the kind of company that will be in the news due to a data breach. And also the kind where the card benefits will rapidly change for the worse in year 2.

Interesting prospect, we'll see if it pans out!

Here's my referral link to anyone who would be willing to help, still in medical school so any bit helps :)

https://x1creditcard.com/r/DFZsRYW

thanks

https://x1creditcard.com/r/0jE5QDE

If anyone wants to use mine :)

Use my link and get 4x for the first month!

https://x1creditcard.com/r/kpvr79I

It seems like they're following a fairly straightforward playbook for subprime cashflow underwriting cards ... and just not fully understanding the gaming possible with their rewards program.

This approach to what's called cashflow underwriting was first pioneered by Petal Card, though Brex was what made it famous on the business side. As noted above, it's had some success with getting a new class of consumers into the credit system, though the target consumer is...

It seems like they're following a fairly straightforward playbook for subprime cashflow underwriting cards ... and just not fully understanding the gaming possible with their rewards program.

This approach to what's called cashflow underwriting was first pioneered by Petal Card, though Brex was what made it famous on the business side. As noted above, it's had some success with getting a new class of consumers into the credit system, though the target consumer is more subprime than for the average rewards card.

The rewards program does make sense when you consider it through the lens of the expected behavior of their average consumer. In particular, note that the card is normally a 2% cashback card, with an upgrade to 3% only available after $15,000 in spend. Given that normal consumers spend ~20% of their gross income on their credit card and targeting moderate-income americans, with this program their average customer will earn little or nothing at the 3% rate. Similarly, 30 days of an extra 2% back compares favorably to the $100-$300 bounties big credit card banks are paying for customers. Since total interchange for a Visa Signature Select runs ~2.3% + 10c per transaction, they end up with a respectable margin here.

Of course, this does not account for MSers with their $500 Wallgreens purchases or million dollar tax (over)payments....

On the redemptions/partners side, they're probably partnering with one of the big partnership aggregators to offer those deals (the same way the shopping portals work). You can also take a look at point.app (a debit card) for another company taking the same approach.

Given the strong and exclusive partnership AmEx and Delta have for SkyMiles cards in the USA, I suspect that the partnership here is not about SkyMiles and they aren't a transfer partner per se. Instead, I'm thinking it's somehow through their gift card office that's been willing to offer modest but useful discounts to select merchant partners like the 10% off Delta GCs sale that Costco had around Thanksgiving last year. (I'm sitting on a...

Given the strong and exclusive partnership AmEx and Delta have for SkyMiles cards in the USA, I suspect that the partnership here is not about SkyMiles and they aren't a transfer partner per se. Instead, I'm thinking it's somehow through their gift card office that's been willing to offer modest but useful discounts to select merchant partners like the 10% off Delta GCs sale that Costco had around Thanksgiving last year. (I'm sitting on a decent amount in discounted Delta GCs at this point from another online shopping portal rebate site but need to burn credits from flights cancelled this year first)

@Kalboz,

"transfer partners", or simply redeem at $0.01 cpp?

If it turns out to be a proper points-transfer, than this is a great deal (for transfer to Alaska/Delta).

If it is merely a 1 point = $.01c redemption for Alaska, then it's pretty meh.

Ooh, all of my favorite things:

Former Twitter executives!

Bank of America!

Complete and utter lack of liquidity!

Imma jump right on that, hermano!

Thanks Julian,

Would appreciate if someone could return the favor.

https://x1creditcard.com/r/268mhMl

My referral link

https://x1creditcard.com/r/Ft0fI4o

https://x1creditcard.com/r/gV4Lybb

I will not send nudes if you use my link.

I used Matt's code. Here's mine:

https://x1creditcard.com/r/I4RgkeK

I used Matt's link.

Here's mine: https://x1creditcard.com/r/I4RgkeK

Thanks for using my link

https://x1creditcard.com/r/2Lj2WvI

https://x1creditcard.com/r/andOIxm

Thanks in advance and a good day to you.

One more for the list:

x1creditcard.com/r/yzgpslW

Use my link: https://bit.ly/2HlOiiN

Here is my referral link: https://x1creditcard.com/r/TaEFk9I

Thanks again for the post and using my referral link. Happy days to you ☺️☺️

The business model isn't that mysterious. The restricted points you're earning are good at a limited number of vendors that have negotiated discounts/wholesale rates. Of course, given those restrictions you can earn more than the ~2% that cash back cards provide.

If those vendors work for you though, it sounds like a great deal if it lasts.

Signed up using link from Kara. Would appreciate if anyone used mine. Thanks.

https://x1creditcard.com/r/s3QiuTf

referral link. Thank you! https://x1creditcard.com/r/2Lj2WvI

https://x1creditcard.com/r/R2R1rHr

Thanks if you used it!

@Sam as one of those young professionals I think thats exactly right... this card seems custom tailored right down to the weird tech-y name

My referral link, thank you.

x1creditcard.com/r/pN9tHm7

I’m such a sucker for hype...

https://x1creditcard.com/r/s91srPM

My referral link: https://x1creditcard.com/r/K8sFUuQ

https://x1creditcard.com/r/ERZwKBy

I used Avi's link. Please use mine, thanks!

https://x1creditcard.com/r/SEidoSe

Hey I just logged in....and this is crazy....

Here's my referral code: https://x1creditcard.com/r/w9iu2fJ

Use it maybe?

https://x1creditcard.com/r/DoOXvPq

My referral link: https://x1creditcard.com/r/aVHEdZJ

Would appreciate if you could use it :)

If you like hockey (and beer) then you need to use my referal link! https://x1creditcard.com/r/C9hwd50

(Worth a shot! lol)

One Referral Link To Rule Them All:

https://x1creditcard.com/r/lXBeOkU

Please consider using my link! https://x1creditcard.com/r/8YDkdiF

I believe the key is the income based credit limits.

This has the potential of granting some very high limits to individuals who are high income/high debt (think, young professionals) who will be likely to make purchases and pay off over time, generating finance charges.

My link, thanks x1creditcard.com/r/OsrTqNX

Ben,

I’m quite sure that retailers are footing a large share of the discount, with that amount still being less than your average cost per acquisition. That would explain the business model.

Interesting concept, to be sure.

@ Robin -- I would agree if the retailers were brands that frequently discount, but you think Apple and Delta would be providing meaningful discounts to a competing credit card product? I highly, highly doubt it...

I definitely think we may see close to two cent redemptions for brands that often discount, but I just don't see most of these brands offering much to X1 in exchange, and I don't think it's a core part of the business model. I could be wrong, though...

https://x1creditcard.com/r/6ZbeRvj

My referral link:

https://x1creditcard.com/r/l2DG8z1

Couple of points I might have missed above:

- This is a Bank of America card

- Relevant (as to our hobby) transfer partners are to Alaska & Delta and perhaps Hotel Tonight & airbnb.

Here is my code: https://x1creditcard.com/r/zb1yxgB

Another potential way they could make money: sell your personal information. Your employment, school, phone, address, income, etc is very valuable information for many businesses, such as insurance salesman and all.

@bigbellyronpaul is right, with the added nuance that this company is probably betting that they’ll be able to make much better use of personal data than many issuers currently do (given the tech executives behind this card), and then monetize the hell out of that data. Big data, when used properly, is a goldmine (and is notoriously underutilized by traditional financial firms). There’s a huge untapped/undertapped revenue stream here, which allows this company to enrich...

@bigbellyronpaul is right, with the added nuance that this company is probably betting that they’ll be able to make much better use of personal data than many issuers currently do (given the tech executives behind this card), and then monetize the hell out of that data. Big data, when used properly, is a goldmine (and is notoriously underutilized by traditional financial firms). There’s a huge untapped/undertapped revenue stream here, which allows this company to enrich the consumer value prop. The trade-off (if you want to call if that) is that you’ll probably have to (get to?) experience laser targeting like what you experience in the digital space today. It might end up feeling a bit “big brothery” to some users.

Thank you in advance for kindly using my referral code.

x1creditcard.com/r/MojQ5QB

I used Kara's code listed above.

https://x1creditcard.com/r/x8eElFy

My referral code:

x1creditcard.com/r/a7Vo0Mc

Thanks!

My referral code: https://x1creditcard.com/r/Ceh1WDM

Thanks!

My referral link: https://x1creditcard.com/r/Py3V5gI

Thank you for using my link.

Paid it forward using Lou’s link. Here is mine and thanks! x1creditcard.com/r/W5JSv1n

My referral link: https://x1creditcard.com/r/B6lDx7G

Thanks in advance!

Ben,

It look very good to be true especially no hard pull.

However, do you know which financial institution is the issuer?

Appreciate if you can use my link to join X1 card wait list. Thanks.

https://x1creditcard.com/r/PTq2Cd6

Here’s my referral code: https://x1creditcard.com/r/SKF5QpU

Interesting concept. Essentially a Brex-like competitor for the consumer market but with a rewards structure that presumably allows X1 to offer discounts that are absorbed by retailers.

Referral link: x1creditcard.com/r/x8eElFy

Thanks if you use it.

Hi Lucky,

They don't have to make money for years to come as long as they can show exponential growth. This is typically Silicon Valley to tech start up model. They may eventually achieve profitability when they have large user base so they could negotiate better deal with those retailers. Uber is not making money. Even Snowflake is not making money. As long as they can show growth and sell the dream to get funding, it can last for years.

referral link: https://x1creditcard.com/r/AWZu8sp