Making Travel Less Taxing: Introduction

Your Tax Home (Away from Home)

Airfare and Transportation

Lodging and Meals

Entertaining Clients

Car Expenses

The Nitty Gritty: Required Receipts and Tax Forms

Ask Scott!

As discussed last week, I am guest blogging through tax filing season to highlight opportunities to reduce your tax liability with business travel expenses. In last week’s introduction, I discussed the main requirements for deducting your business travel expenses: travel must be unreimbursed and incurred in the ordinary and necessary course of running a business. This week, I’ll discuss the last requirement for travel to be deductible: expenses must be incurred while traveling away from home. Please note the legal disclaimer at the end of this post.

A Second Home, Courtesy of the IRS

“Where is home?” When asked this question at a cocktail party, you will likely answer with either your current place of residence or where you grew up. For frequent business travelers, the ever-complicating helpful IRS would also like to give you a second home—a tax home. According to the IRS, business travel is deductible when your business requires that you be away from your home substantially longer than your normal work hours. The key criteria here is that your work must be taking you away from your “tax home.”

For the vast majority of taxpayers, their tax home is the same as their personal home, but for those who do extensive business away from their personal home, the two may be different. The distinction is important because only those expenses incurred while away from your tax home are deductible. Your tax home is the place where you normally conduct your business, regardless of where you live.

So, hypothetically speaking, for the random road warrior who travels to Ft. Worth each week for work but returns to a personal residence in the Phoenix area on the weekends, his tax home would be Ft. Worth even though he calls Phoenix home. If you have more than one place of business, then your tax home is the place where the majority of your business is conducted. For most taxpayers, the calculus for determining a tax home stops there.

But, if you have no primary place of business, the IRS lovingly refers to you as an itinerant, which to me sounds vaguely like a travel blogger. 🙂 If the IRS classifies you as an itinerant, then you are never away from home, which means none of your travel expenses would qualify as business deductions, so even the most enthusiastic “I’m never home” business traveler is best served tax-wise to have a tax home. Here are the three factors the IRS will consider in determining your tax home when you have no primary place of business:

- You perform part of your business in the area of your main home and use that home for lodging while doing business in the area;

- You have living expenses at your main home that you duplicate because your business requires you to be away from that home;

- You have not abandoned the area in which both your historical place of lodging and your claimed main home are located; you have a member or members of your family living at your main home; or you often use that home for lodging.

If you meet all three factors, your tax home is your personal home, and any travel you incur away from there will clear the “away from home” requirement for business travel deductions. If you meet two of the three factors, you may have a tax home depending on the facts and circumstances (which is IRS-speak for “hire a good tax attorney”). If only one factor applies to you, then you have no true tax home, and none of your business expenses are deductible, unfortunately.

Temporary and Long Term Job Assignments

A temporary assignment (see, e.g., visiting professors, traveling nurses, or oil field workers, among other vocations) on an ongoing basis may cause a change in your tax home depending on the length of the assignment. If, upon taking the job, you expect that it will last for more than one year, the job is considered to be indefinite, and your tax home would change to that location immediately. The IRS considers a job that you expect to last for 12 months or less to be a temporary assignment that does not shift your tax home, thereby making your travel expenses deductible. Thus, all other things equal, a 12 month appointment in a different location is tax preferred to a 13 month one.

During law school, a visiting law professor of mine was delighted to explain to his eager tax students how he was deducting all his living expenses in Charlottesville, Virginia, for the year in which he and his entire family were away from his tax home of Ann Arbor, Michigan. Because his temporary assignment was expected to last for less than 1 year, he was considered to be traveling away from his tax home and all of his lodging and meals were deductible (subject to other limits which I’ll discuss in later weeks). If he had taken the visiting professorship with an understanding from the dean that it was going to be a permanent position, then his tax home would have shifted immediately since his expectation at the time would be that the job assignment would last longer than 12 months. (He in fact returned to Ann Arbor, tax savings in tow).

Where There’s an Expense, There’s (Potential) Income

While it does not matter to the IRS in which state you work, individual states do have a stake where you work. A few commenters brought up state income tax allocation issues last week. So, I thought I’d address that issue briefly here since if you’re traveling away from home on business and incurring expenses, you are hopefully also generating some income while doing so. If not, your days in business may be as numbered as the latest merged airline credit card offer.

If you travel and conduct business in multiple states, you may need to allocate your income among those states. A full discussion of all 50 states’ income allocation rules is of course beyond the scope of this post, but in brief, state tax officials are no fools and won’t take pity on tax evasion.

The tax departments in high-tax states like California and New York know that every person traveling there on business has an incentive to allocate income away from their grasp. If you work in multiple states, your economic incentive is to allocate as much income as legally possible to the low or no tax states in which you also work.

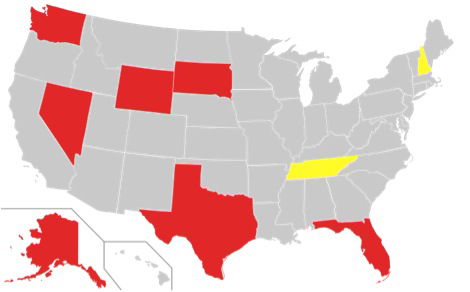

States With No State Income Tax on Wages (NH and TN Tax Investment Income But Not Wages)

If you own real property, the state income allocation is fairly easy: whatever income received from the rental or sale of the property would be taxable in the state in which the property is located. But, what about those who generate income from services? Most famously, NFL players must allocate their income earned based on the days they are in various cities, and since the game schedules are publicly available, any diligent state tax collector is sure to come calling if, for example, Joe Flacco doesn’t include some Louisiana income in his 2013 tax return after his lights-out performance in the Super Bowl.

For those of you with less public lives, what’s the test? Each state differs slightly, but the primary inquiry is whether you perform services in the state or receive income related to a business carried on in the state. For example, if you traveled to New York to meet with a client and made a sale, but you performed all of the work in Washington, then you may escape New York taxation since you did not in fact perform the work while there.

Conclusion and Next Time

Thus, your home for tax purposes turns out to be less than intuitive but quite important to determining whether specific expenses become deductible or not. Feel free to use “where’s your tax home, good lookin’?” as a pick-up line at your next cocktail party and share with us the results in the comments. Next week, I’ll discuss how much you can deduct for airfare when traveling on a part-business, part-personal trip or when redeeming frequent flyer miles for business trips. Please leave any questions you have in the comments! Also, you may follow me on Twitter @ScottTaxLaw or learn more about my legal and CPA practice.

Disclaimer: While I hope the information I provide will be helpful (and hopefully even humorous at times), none of this information should be construed as offering legal advice or creating an attorney-client relationship between the reader and my law firm. You should not act or refrain from acting based on this advice and should consult your own attorney or CPA regarding your specific tax matters. IRS Circular 230 Notice: Nothing in these communication is intended to be used and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law.

My husband works construction. The local contractor currently has a project in Atlanta. So, he hired on in May, and traveled 200 miles away from home (where he maintains a home, and his family lives) every week to work in Atlanta (unreimbursed travel expenses). Unfortunately, I think his tax home would be considered Atlanta, right?

Second question: Can we claim the standard mileage deduction for his trips home? I thought I saw this somewhere and...

My husband works construction. The local contractor currently has a project in Atlanta. So, he hired on in May, and traveled 200 miles away from home (where he maintains a home, and his family lives) every week to work in Atlanta (unreimbursed travel expenses). Unfortunately, I think his tax home would be considered Atlanta, right?

Second question: Can we claim the standard mileage deduction for his trips home? I thought I saw this somewhere and now can't find it.

Thanks in advance.

I am an oil field worker who works 28 hrs. on 20 hrs. off, 2 weeks on 1 week off. The company I work for does not pay per diem. We purchase food on the way to location for each shift and are, obviously, away from our taxable homes for 28 hrs. at a time. This is in West Texas, I was wondering if I can claim my food expenses during my time in the field? Any information you could provide would be extremely helpful, thank you, Russell.

HI,

We hire employees for temporary assignment? Are they considered itinerant if they do not maintain a tax home even though the assignment is temporary (5-6 months)?

Thanks,

liz

Thank you, Scott and Goblueto. That was my question. I appreciate your discussion of it.

Matt -

The foreign sourced income can be excluded from US income if you meet the foreign earned income tax exclusions, which involve living in the foreign country for an entire year or nearly an entire year. If you're only gone a week or two, then that income is not removed from your US tax liability. But, if you pay foreign taxes, then you will be able to take a foreign tax credit against your...

Matt -

The foreign sourced income can be excluded from US income if you meet the foreign earned income tax exclusions, which involve living in the foreign country for an entire year or nearly an entire year. If you're only gone a week or two, then that income is not removed from your US tax liability. But, if you pay foreign taxes, then you will be able to take a foreign tax credit against your US income for the amount you paid to the foreign government.

The answer to your last question would depend on the country and their individual tax laws; each country would have their own rules on what constitutes "situs" for tax purposes and generates a tax obligation.

Gobluetwo: I'm in a similar situation. My record so far is having to file in 6 states and another country (for work performed in a prior year). Thankfully my company provides an accountant for people that have too many tax returns to file, though I don't use them except for the international returns (and the associated federal returns) as those are over my head.

We have a system where I just note what state I...

Gobluetwo: I'm in a similar situation. My record so far is having to file in 6 states and another country (for work performed in a prior year). Thankfully my company provides an accountant for people that have too many tax returns to file, though I don't use them except for the international returns (and the associated federal returns) as those are over my head.

We have a system where I just note what state I performed the hours in, which is nice and easy and I get a broken down W2 at the end of the year, at that point I just have to manage keeping a tax home as keeping up with my compensatory situation if I think I'll be somewhere longer than a year.

Hi Scott,

Can you speak a bit about income allocations when corporate work is performed internationally? When can foreign sourced income be deducted from US salary on a W-2, and what obligations are there to pay taxes to foreign governments on short business trips of 1-2 weeks?

Thanks.

@Mark S - Yes, as mentioned at EggSS4, you could realize some savings by having some of your income not taxed in those other states since all states have at least some amount (although usually relatively small) that is not taxed at all. Particularly since you live in California, allocating your income to other states would benefit you tax-wise. You'd have to balance the savings against the hassle of filing in those other states and...

@Mark S - Yes, as mentioned at EggSS4, you could realize some savings by having some of your income not taxed in those other states since all states have at least some amount (although usually relatively small) that is not taxed at all. Particularly since you live in California, allocating your income to other states would benefit you tax-wise. You'd have to balance the savings against the hassle of filing in those other states and keeping track of the travel, but a good CPA can make that relatively painless!

@Joe, please send me a message on twitter @ScottTaxLaw. I would need some additional facts to properly comment, but I wouldn't classify you as an itinerant quite yet.

Thanks, @gobluetwo for the additional interpretation of Levy's question. If you have a contract with an organization in State B that requires travel overseas, and you perform the work overseas, then I think the income would be allocated to state A even though your client is in state B, because you performed the work out of the country. Unfortunately, the U.S. taxes all worldwide income, so there's not an option to say that the work...

Thanks, @gobluetwo for the additional interpretation of Levy's question. If you have a contract with an organization in State B that requires travel overseas, and you perform the work overseas, then I think the income would be allocated to state A even though your client is in state B, because you performed the work out of the country. Unfortunately, the U.S. taxes all worldwide income, so there's not an option to say that the work was performed in no state at all.

@EggSS4 - yes, that may work out well for you if you can only be in the other state for say a few weeks. But, some people don't like the hassle of filing extra state returns. Let's say that the state income tax rate is 6% in both states, and you make $2,000 a week. You would save 6% x $2,000, or $120, on one week's income. That savings may not be worth it to some people but of course your tax may vary. :)

I have another specific and potentially unique situation. My home is in State A, where I worked in a part-time job for a week in January. Then, I took on a temporary job in State B from mid-January through the end of May, knowing that it would end at that time. I was then unemployed and living with my parents for the remainder of the summer and autumn in State A, until I then began...

I have another specific and potentially unique situation. My home is in State A, where I worked in a part-time job for a week in January. Then, I took on a temporary job in State B from mid-January through the end of May, knowing that it would end at that time. I was then unemployed and living with my parents for the remainder of the summer and autumn in State A, until I then began a new (permanent) job working in State C in November.

When determining my tax home, I don't think I'd qualify for "performing part of my business in the area of my main home and using that home for lodging while doing business in the area" since I barely worked in State A, nor did I have incurred living expenses while being there under my parents' roof. I assume that I would be classified as an itinerant and could not deduct expenses incurred while temporarily living and traveling to/from State B?

Thanks for your input.

This may be a bit too specific for this discussion but I live in California and work as a pilot for a company doing aerial survey. The company is based in Virginia. Several times a year I travel to Virginia and prep a plane for a project and then go for several weeks at a time to somewhere in the US or Canada and work and eventually return home to California until another project arises....

This may be a bit too specific for this discussion but I live in California and work as a pilot for a company doing aerial survey. The company is based in Virginia. Several times a year I travel to Virginia and prep a plane for a project and then go for several weeks at a time to somewhere in the US or Canada and work and eventually return home to California until another project arises. I found a federal statute 49.40116 concerning employees of air carriers not having to file in every single state they fly. We are doing aerial work so I am still unclear how I get defined by this. I was figuring that in the end living in California, I would end up paying equally whether I pay just to California or to each state I fly in, but would I actually save money by filing in each state? In 2012 I spent at least a week flying in California plus 5 other states and had stopovers in 7 other states.

Very interesting post.

If your stay in another state is brief, as long as you don't live in a state without income tax, isn't it almost certainly better for the tax payer to have that (say) week away - since your income reported to the state you're traveling to would be low enough to end up in the state's lowest tax bracket, vs. your home state where almost all of your income is charged?

re: Levy Flight - sounds like he's saying something like: lives in NJ, but works for a company in Philly (or NYC). However, travels overseas frequently for his job.

I think in this case, I would guess that the tax home would be where you primarily work when you're not traveling. If when you're not traveling, you're in the office 100% of the time, state B would be your tax home. If you're virtual,...

re: Levy Flight - sounds like he's saying something like: lives in NJ, but works for a company in Philly (or NYC). However, travels overseas frequently for his job.

I think in this case, I would guess that the tax home would be where you primarily work when you're not traveling. If when you're not traveling, you're in the office 100% of the time, state B would be your tax home. If you're virtual, for all intents and purposes, then state A would be your tax home.

I am not an accountant.

Anyway, my company's time keeping system used to be really convenient for entering the state in which you worked. One year, I ended up paying taxes in 3 different states due to travel. Now, we upgraded our platform and it's not straightforward, so I know a lot of folks who just don't do it anymore (if they ever did it in the first place).

@Levy Flight - I am not sure I fully understand your question. Can you send me a message on twitter with some additional details, and I'll do my best to answer? Thanks.

I am curious about a situation where live in one state (A) but have a contract with an organization in another state (B) that requires travel overseas. Is tax paided in State A or B?

@Jon, good question. Yes, the employee will be able to do so as long as the expenses are unreimbursed. However, unreimbursed employee business expenses are subject to a limitation. Only those amounts that exceed 2% of your adjusted gross income are deductible, and the deduction is taken on Schedule A, Itemized Deductions. If you're traveling that often and for that many weeks, though, your expenses may exceed that 2% limit, and it may provide you some tax benefit.

Can an employee of a company deduct expenses for traveling from the employee's out-of-state home to the company's client's office location, where they will be working 40-hrs a week for 3 months? It wasn't clear to me whether only "self employed" people can claim deductions for traveling away from their tax home, or whether this also extends to employees of corporations.

@Jeff, I don't know his situation, but if i did, I wouldn't be able to disclose it ethically.

@Johnnycakes, although the in's and out's of what our travel bloggers can deduct would be fascinating to some of us, I'm hoping to provide information that is broadly applicable to all business travelers in this series. I think you'll see in future weeks some of the limits that apply to all business travelers, though, including our beloved bloggers. :)

@johnnycakes - I know some travel bloggers deduct every penny of their travel expenses. I'm not comfortable going that far. A fair amount of mine involves visiting family with absolutely no relation to the blog.

Matt -

If at the outset, you anticipate that the job will last less than a year, your tax home doesn't change and you can deduct your expenses. When you discovered that it will in fact last longer than a year, your tax home changes, and you won't be able to deduct travel costs from that point forward.

What if you initially accept an internship that's less than a year, file taxes, but then the internship rolls over and ends up being longer than a year?

i'd be very interested in reading about an anonymous travel blogger example, in which you detail for us how much, or how little, of their travel expenses can be deducted for business purposes on their self-employment deductions, sched. C.

as a novice, I had imagined they could deduct nearly everything, from food to flights and hotels, if they were the type to highlight all those details in a trip report on their profitable blog.

So lucky doesn't deduct his trip costs for taxes?