Typically when we consider the value of using a credit card to pay for a purchase, we think of it in terms of the rewards that we can earn. However, there’s another major benefit to paying by credit card, and that’s the ability to dispute a charge, or to flag purchases as fraud (this is in addition to any other purchase protection offered by a card).

In this post, I’d like to talk a bit more about disputing credit card purchases. Under what circumstances can you dispute charges, how do you go about doing so, and is there a difference between card issuers when it comes to this? Let’s cover the basics…

In this post:

When you can dispute a credit card charge

Under what circumstances can you dispute a credit card charge? There are a few general things to keep in mind:

- There’s a difference between a purchase you should mark as fraud, and one you should dispute; fraudulent purchases include completely unauthorized ones, with companies you don’t do business with, rather than maybe a recurring payment with a company you do business with (which you would dispute)

- You’re only supposed to dispute a charge after you’ve reached out to the merchant to resolve the issue, and after you’ve come to a dead-end there

- You often have only 60 days from when the purchase was made to dispute a charge; this can be tricky, especially if you’re paying for a service well in advance (like a flight or a pre-paid hotel)

- Think of a credit card company more as a common sense court, rather than an assistant manager at an Olive Garden; in other words, you don’t dispute a charge because the pasta wasn’t very good, or because the service could have been friendlier, but rather because you didn’t get what you explicitly paid for

To give some examples of when a credit card dispute is appropriate:

- If you didn’t receive what you paid for

- If the item you received is defective

- If you didn’t authorize a purchase

- If you were double charged

- If you were charged a recurring fee after cancelling

- If you were charged the wrong amount

Now, there are definitely some grey areas when it comes to whether something should be disputed or not. For example, say you book a business class ticket on a long haul flight, but the seat is broken and doesn’t recline. Say the airline is only willing to give you a small number of miles as compensation.

Is it appropriate to dispute the charge in that situation or not? While the airline isn’t violating its contract of carriage (which is entirely one-sided), the airline is no doubt not living up to what was advertised, if you were promised a flat bed.

How you can dispute a credit card charge

While each credit card issuer has its own exact procedure for disputing a charge, the general concept is the same:

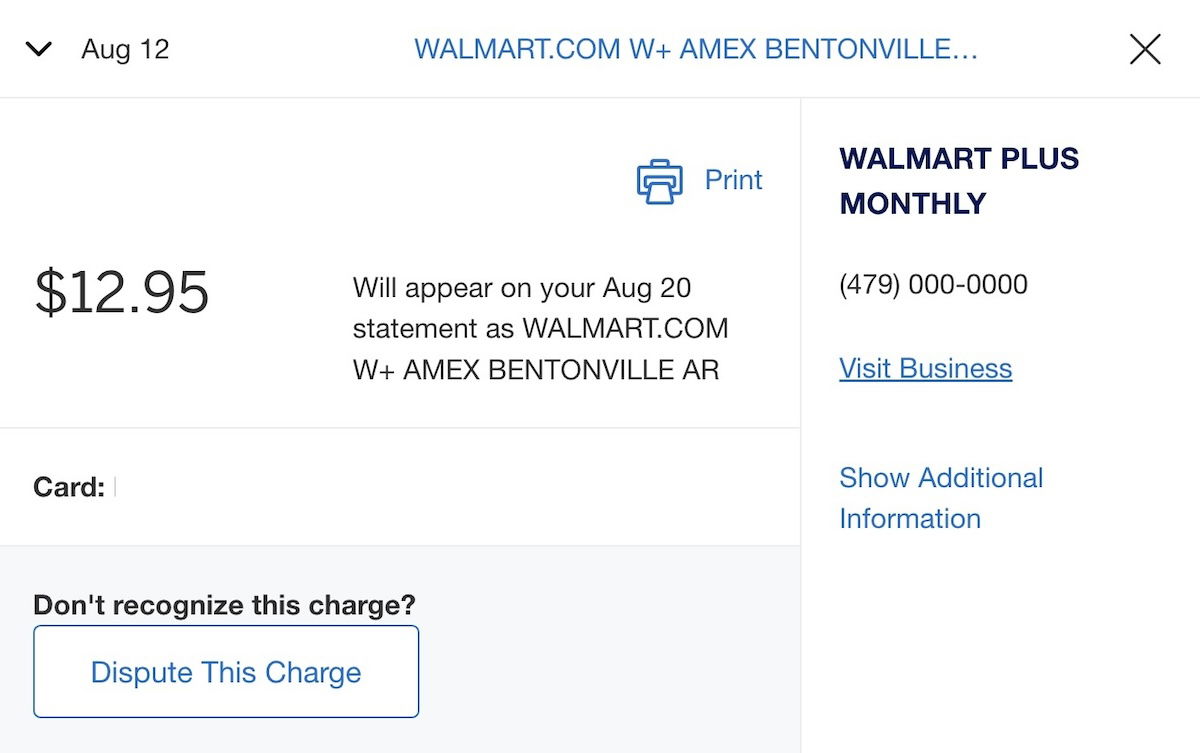

- When reviewing your charges online through your credit card company, you should see some sort of “dispute” button near any eligble purchase, that allows you to dispute the charge

- Alternatively, you can just call the credit card company, and they can help you file a dispute

Typically when you dispute a charge, you’ll be asked to provide some basic details, including confirming that you contacted the merchant first, sharing what went wrong, and more.

When you dispute a charge, you’ll be given a temporary credit for the amount of the purchase, until the dispute is resolved (at which point you’ll either be credited the amount permanently, or will be charged it once again).

The investigation into a charge can take up to a couple of months. This is because the card issuer gives the merchant the chance to respond to the dispute, and that can take some time. So you’ll want to dispute the charge within 60 days, and then you can expect it could take a similar amount of time for a final decision to be made.

Be responsible with credit card disputes

I know many people will dispute credit card charges as their first course of action when they’re not happy, rather than as a last resort. You should always try to first reach out to the company, and only dispute a charge either if you don’t get a satisfactory response, or if you’re approaching the 60-day deadline for disputing a charge.

Just to expand on that a bit:

- If you dispute a charge despite not having first reached out to the company, you might actually be making things take longer, since a dispute takes an extended period of time, while a company can often resolve your issues much more quickly

- While we probably don’t have much sympathy for mega-retailers, for small businesses, credit card disputes can be challenging, since the company isn’t paid until the dispute is resolved

- When you reach out to the company first, you’re really getting two chances at getting something resolved, so it maximizes the odds of a positive resolution

Not all credit card issuers are created equal

On the topic of credit card disputes, here’s what I consider to be an interesting topic. If you’ve disputed credit card purchases with any frequency, you might have noticed that not all issuers handle them equally well. Some issuers are definitely a bit “friendlier” to disputes than others.

For example, in my experience, American Express is the best card issuer when it comes to resolving disputes in a consumer-friendly way. I’ve found Chase to be very good as well. However, I haven’t necessarily had equally positive experiences with other issuers, including Capital One and Citi.

Admittedly this is all anecdotal, and in some situations a dispute is pretty cut and dry, and one party is right, while the other is wrong. However, all else being equal, I find Amex’s excellent handling of credit card disputes to be a reason to use those cards for purchases.

Bottom line

Credit card disputes are a useful tool for situations where a merchant charges you for something you don’t think you should have to pay. While I think it’s important to use this ethically (after reaching out to a company first), this has saved me many times in situations where I got charged for a service that I didn’t receive.

I think it’s also worth emphasizing that different issuers seem to handle disputes a bit differently, and they’re not all equally consumer-friendly.

What has your experience been with credit card disputes, and which issuer have you found to be best?

Amex is not good with disputes any more. Haven’t been since post covid.

Not just the lounges that are under strain.

Disputed a charge in a Hotel in Vienna. No one was available to check me in at 1:40 p.m., check in time was 2:00p.m.

I retuned to a hall way, asked a person who appeared to be a housekeeper, about thelocation of the checkin-desk(?0. She pointed to an open door, a man, the owner(?) was on the phone. he waved me away and I returned to the front door, rang the bell, no one...

Disputed a charge in a Hotel in Vienna. No one was available to check me in at 1:40 p.m., check in time was 2:00p.m.

I retuned to a hall way, asked a person who appeared to be a housekeeper, about thelocation of the checkin-desk(?0. She pointed to an open door, a man, the owner(?) was on the phone. he waved me away and I returned to the front door, rang the bell, no one answered. My granddaughter went up the stairs, three flights and the same person waved her away. By this time it was closer to 2:00p.m.

Called booking.com, explained the situation, representative canceled the reservation.

When my AmEX statement arrived, i was charged the full amount. i disputed this charge. The process was quick for my written detailed dispute, which was required by AmEX.

The owner, denied the dispute, said we had left before the reception desk was to open, his description of the incident was full of untruths, including the wrong date and time. I tried to call the hotel, in order to rectify the whole incident, suggesting I pay half of their fee., they refused hung up and disconnected the line. I lost.

Beware, don't go to Hotel Suzanne

@S.Jean... you should have lost. Not great service but you were there and left before check in time.

Interesting post I would have to disagree with American Express handling disputes well. Decades ago yes today no.You are arguing with uneducated others in overseas call centers who document poorly incorrect information and American Express routinely closing cases that are unresolved and the need to reopen them again.Ive reduced my business with them enormously and cut up most of my cards

Citibank has 100% track record in my experience

If you have a...

Interesting post I would have to disagree with American Express handling disputes well. Decades ago yes today no.You are arguing with uneducated others in overseas call centers who document poorly incorrect information and American Express routinely closing cases that are unresolved and the need to reopen them again.Ive reduced my business with them enormously and cut up most of my cards

Citibank has 100% track record in my experience

If you have a premium card during normal business hours dealing with US call centers.They are the Gold standard after my 50 plus years charging in 2026.

No matter what else that sucks about them this is their one clear strength.

Chase subpar to ok Bank of America and Wells Fargo perhaps in your next lifetime you may get something resolved

You gotta fight the good fight, but, man, sometimes it takes waaay more effort than it should...

Worth a read if you get past the paywall (try archive.ph)

https:/www.nytimes.com/2026/03/05/travel/hotel-mold-rodents-credit-card-refund-refusal.html

If you dispute anything with a large company, be prepared to get blacklisted. Large companies don't actually spend time reviewing whether the dispute is legitimate, they typically do not respond at all - and if they don't respond, the credit card sides with you. However, the company then blacklists you - not a problem if you are never ever going to use them again. A big problem with a large rental car, flight or hotel...

If you dispute anything with a large company, be prepared to get blacklisted. Large companies don't actually spend time reviewing whether the dispute is legitimate, they typically do not respond at all - and if they don't respond, the credit card sides with you. However, the company then blacklists you - not a problem if you are never ever going to use them again. A big problem with a large rental car, flight or hotel company. This is always a big concern, your claim may be 100% legitimate and it may just be a billing error - doesn't matter, you get your money back but be prepared to never ever be able to do business with them. I have several examples . Hertz banned me for life after I disputed a billing error. Virgin Atlantic went even further. I had cancelled mileage tickets within 24 hours but they charged me a $50 booking fee and simply didn't respond. So I disputed it with Chase and got my money back. However, meanwhile I booked new, completely different tickets with Miles on Virgin Atlantic and you can probably already guess what happened. Yup, they canceled them too but didn't inform me - so I ended up not having a ticket at all. I found out not at the airport but a week before my flight which was during summer schedule. I called them up and they said - yup, we canceled your tickets because you had disputed another transaction earlier. So you seem it doesn't matter if you are right, if you have a dispute with a large company, you either have to resolve it with them directly which is often impossible because they simply don't respond, or you choose to pay for their mistakes. Or else be ready to be blacklisted by them.

@Tja You should actually thank Hertz because why would anyone want to do business with such a horrible company. OMATT sure had posted enough bad things about Hertz for you to switch to another car rental company. As for Virgin Atlantic, could it be that you booked not too far from the prior award cancellation that they just automatically flagged the new booking as possible fraud? Did you check your booking confirmation and any email...

@Tja You should actually thank Hertz because why would anyone want to do business with such a horrible company. OMATT sure had posted enough bad things about Hertz for you to switch to another car rental company. As for Virgin Atlantic, could it be that you booked not too far from the prior award cancellation that they just automatically flagged the new booking as possible fraud? Did you check your booking confirmation and any email updates before heading to the airport on the day of departure?

I have a tricky situation to dispute and seeking an advice : on Feb 19th , there was a national strike day in Argentina and Aerolineas cancelled our flight SLA-MDZ and the next earliest flight was on 22 ( there are no daily flights between the two cities). In the meantime, on 21 we were having another booking with Aerolineas from MDZ to BUE, but we weren’t able to get to Mendoza on time - is this a reason for dispute with Aerolineas ( 7 tickets ) ?

I am in the middle of a dispute now. I booked airline tix and found cheaoer ones an hour later so tried to cancel via website no go so i called the airaline and after 2.5 hours on hold got a human and cancelled. Two days later got an mail saying we are processing your refund. It has been almost a book and no refund. I started a dispute for the 2 tix purchased and...

I am in the middle of a dispute now. I booked airline tix and found cheaoer ones an hour later so tried to cancel via website no go so i called the airaline and after 2.5 hours on hold got a human and cancelled. Two days later got an mail saying we are processing your refund. It has been almost a book and no refund. I started a dispute for the 2 tix purchased and uploaded info.. Only one tix refunded??? now try to get the second one credited. I called Amex and they said they would do manually.?? we will see

I have had excellent results and assistance from Citi when I have had to dispute a charge with them. It's happened a few times over the about 25 years I've had their card.

Sadly I lost a large dispute through Amex after the merchant, Brilliant Earth, lied about who had possession of the item and said I was seeking unjust enrichment by trying to keep an item and get money back through a chargeback. I tried appealing and CFPB complaint but no dice despite all my proof and written evidence from the merchant admitting they have the item.

CFPB doesn't really exist anymore. Sorry @FFFM

My experience has been excellent with Elon Financial, which issues the Fidelity cash back cards. Of course, I’ve only ever filed disputes that deserve to be approved, at least from my point of view, but they’ve consistently credited back everything I’ve disputed. The one area where I think they could improve is they seem to require all documentation to be submitted by snail mail, not electronically. Maybe that’s a regulatory requirement?

Amex’s new dispute “process” of accepting any merchant reply without reading it to rebill you fails their obligation under Reg Z.

My experience with Bilt 1.0 with a disputed charge was more merchant friendly than consumer friendly and it made me not want to use my Bilt for everyday purchases.

You can dispute a charge after 60 days, but the "burden of proof" shifts to you (the disputer), whereas before 60 days the burden of proof is on the merchant

Several years ago I came across a PhD dissertation done on the topic of credit card disputes and the cost to process them. The cost per dispute was surprisingly high (something like $50 at the time). Nowadays more companies use AI. I've found that Citi will frequently automatically permanetly approve disputes i submit on my AA Exec Mastercard which I spend over $100k per year on. Chase, on the other hand, I just had to...

Several years ago I came across a PhD dissertation done on the topic of credit card disputes and the cost to process them. The cost per dispute was surprisingly high (something like $50 at the time). Nowadays more companies use AI. I've found that Citi will frequently automatically permanetly approve disputes i submit on my AA Exec Mastercard which I spend over $100k per year on. Chase, on the other hand, I just had to call Friday to get resolution on a $15 bogus no show charge from Yelp on my CSR.