The Chase Sapphire Reserve® was introduced in the fall of 2016, and took the US credit card market by storm. Chase allegedly reached their 12 month sales goal for the card within two weeks of introducing it. The card was so popular that they ran out of the metal needed to produce the cards. I imagine they knew the card would be popular given the sign-up bonus and great rewards of the card, though it’s pretty incredible that it exceeded their expectations by that much.

This has raised some questions about whether Chase will ever be able to make money with the Chase Sapphire Reserve®. While Chase expenses the customer acquisition costs over the first 12 months, it typically takes seven years before they make money on a customer. The further challenges with this card have been that fewer cardmembers have been financing charges than Chase expected, and that’s a way a lot of issuers make money. Furthermore, cardmembers have allegedly been using the card for more dining and travel purchases than anticipated, and since the card offers triple points in those categories, it’s presumably an area where Chase loses money.

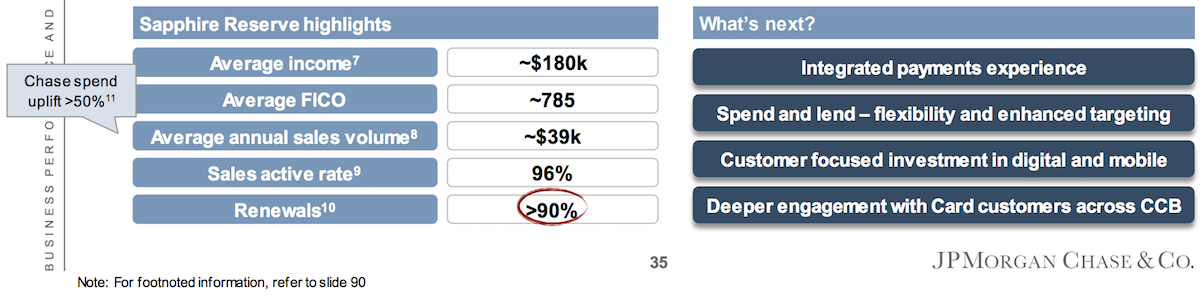

Doctor Of Credit points to a JPMorgan Chase investor day presentation, which contains some interesting statistics about thee Chase Sapphire Reserve®:

- The average income of a Chase Sapphire Reserve cardmember is ~$180,000

- The average FICO score of a Chase Sapphire Reserve cardmember is ~785

- The average annual sales volume of a Chase Sapphire Reserve cardmember is $39,000

- The average sales active rate for a Chase Sapphire Reserve cardmember is 96% (this is the number of cards with greater than zero gross sales divided by the number of total open accounts)

- The average renewals for the Chase Sapphire Reserve are 90%+

Those are some really impressive numbers, and really shows what a success this card has been. The following two statistics stand out to me most:

- The average renewal rate for premium credit cards is 60-90%, so to have a 90%+ renewal rate is virtually unheard of

- The average cardmember has spend of ~$39,000 and income of ~$180,000, meaning that on average cardmembers are spending ~22% of their income on this card, which is fairly close to the average percentage of income that American consumers spend on credit cards; it’s astounding that Chase has been able to capture so much wallet share with this card, and make it a “one size fits all” card for so many consumers

The Chase Sapphire Reserve® is so popular for good reason. While it has a $795 annual fee, the card offers a $300 annual travel credit, 3x points on dining, great travel, car rental, and purchase protection, a Priority Pass™ Select membership, a Global Entry fee credit, and much more.

Do any of the above statistics about the Chase Sapphire Reserve surprise you?

I have it for a year and do a lot of business travel. The Priority Pass got used once (but most of my travel is via train) & did use the travel voucher. The added travel miles have been great as we are classic DINKS who eat out 3x per weeks and travel as much as we can now for fun

@dan yo, I'll get the booze if you bring the white and @hal's in charge of the girls

What? You guys aren't using your points for the equipment needed to make the giant donuts in the Chase commercial ?

I am a CSR holder who is above the average Fico score, but below the average income. I don't have a ton of annual spend, but I can tell you that Chase has lured me into their ecosystem with the CSR (I had aleady had and continue to use the Freedom), to the point where I got the freedom unlimited as well, and those 3 cards now cover 100pct of my spend whereas I used...

I am a CSR holder who is above the average Fico score, but below the average income. I don't have a ton of annual spend, but I can tell you that Chase has lured me into their ecosystem with the CSR (I had aleady had and continue to use the Freedom), to the point where I got the freedom unlimited as well, and those 3 cards now cover 100pct of my spend whereas I used to have other daily cards. The good experience I've had with collecting and redeeming those points (usually for free or near free airfare/car rentals booked through chase portal) has made their image very positive for me. Chase is expanding branches to new cities (one is mine) and so they have my attention to other offers for checking/savings/mortgage, etc. It seems the CSR is a part of a long term customer engagement strategy and in my case at least, I can confirm it is working.

It is not 3 points per dollar on travel and dinning. It is actually more because of the 50% bonus you get if you redeem for travel with them. I also think that Chase has relatively high qualifications for one to obtain this card which is why the statistics are so good. It's like the Chase or Visa version of Amex Platinum.

I don't have work travel and we put only about $10K/year on the card (income at $167K/yr is pretty close to the average). We did become Chase Private Clients when you could circumvent the 5/24 rule, but now that you can't, we'll be shifting our bank holdings to BofA in a year when I retire, and using their Premier Rewards card with the Platinum Honors multiplier.

If Chase is happy, then I am also happy because it means that they're not likely to begin 'enhancing' the CSR's rewards earning structure ;-)

The structure of Chase’s rewards earning probably means that it’s a money losing operation or at least not at an acceptable ROI as compared to other business units.

Chase right now has incentivized maximizing value behavior and not profit-generating behavior, even if that profit came from other business units (see Wells Fargo’s and BOFA’s programs).

I expect we will see major tweaks come as the cost of capital rises over time.

I’ve been surprised by the lack of cross selling from the CSR into other products. I get the usual ads for a Chase savings account but nothing targeting my brokerage business. E-Trade calls me every year to pitch for a transfer but Chase hasn’t even emailed me with an offer. Seems like a missed opportunity as I’d be keen to hear the pitch.

Mark-

Certainly that depends on the individual PP lounge you visited right. Some are dreadful while others are surprisingly nice. I think the value of the PP access in your case would come into play for times when there is no AA lounge for you to use.

@ hal

is your company hiring? I am good at carrying around white substances to strip clubs.

I walked into .. and right back out of a Priority Pass lounge.

I will stick with my AA Executive Card with the Admiral's Club access. -- far better

@David: "the statistics refer to individual income, not household income."

I imagine the statistics are derived from whatever income cardholders stated on their credit card application, which can include any income that could be used to pay the bill. (That's what banks tell me when I ask them "do you mean my income, or my household income?")

@Ted "the idea of not caring about smaller amounts of money if you have good earnings is a...

@David: "the statistics refer to individual income, not household income."

I imagine the statistics are derived from whatever income cardholders stated on their credit card application, which can include any income that could be used to pay the bill. (That's what banks tell me when I ask them "do you mean my income, or my household income?")

@Ted "the idea of not caring about smaller amounts of money if you have good earnings is a misnomer"

Exactly :)

There is more to being wealthy than having a good income. Frugality helps. In fact there is a whole online subculture devoted to the idea - google Mr. Money Mustache.

I earn significantly more than the listed average (on a good year, I am self employed and income does vary) and my most recent FICO is 825. I have no home or car debt (paid off). However I certainly do care about the extra points offered by the CSR and combine it with a Freedom Unlimited. I’m deep in the Chase ecosystem as a private client in banking with them as well.

Like a...

I earn significantly more than the listed average (on a good year, I am self employed and income does vary) and my most recent FICO is 825. I have no home or car debt (paid off). However I certainly do care about the extra points offered by the CSR and combine it with a Freedom Unlimited. I’m deep in the Chase ecosystem as a private client in banking with them as well.

Like a previous poster said I value the points much higher then 2 cents each. We generally use them for premium international bookings and get a much higher redemption rate. But the idea of not caring about smaller amounts of money if you have good earnings is a misnomer in my experience. I think people who have worked hard to earn money value it more then anyone.

@snic The statistics refer to individual income, not household income. Optimizing redemptions are not the same as optimizing earn categories. You say it's not that complicated to keep 2 cards in your wallet, but how deep does the rabbit hole go? If you really want to optimize, you can easily have a wallet full of different cards (like Lucky).

In the end, it's not going to make a gigantic difference for most people if they...

@snic The statistics refer to individual income, not household income. Optimizing redemptions are not the same as optimizing earn categories. You say it's not that complicated to keep 2 cards in your wallet, but how deep does the rabbit hole go? If you really want to optimize, you can easily have a wallet full of different cards (like Lucky).

In the end, it's not going to make a gigantic difference for most people if they just picked one good card rather than 2 (or more).

@jeff As it should. Credit scores are a reflection of your ability to pay off debt, so a lack of debt would mean less data for the credit issuers to judge your credit worthiness.

I imagine plenty are putting a lot of reimbursed t&e spend on the card. I know I am.

@ Benjamin - my numbers are identical to yours. Not having any debt lowers your score, it seems

@Kevin: "It is PITA to keep track of the Freedom Unlimited categories that earn extra points."

You are confusing the Freedom Unlimted with the Freedom. The Unlimited gives you 1.5 points for all purchases, no categories.

@David, @Tom: "high income individuals have better things to do than to figure out optimization strategies for travel cards"; "If you make $180,000 per year, do you really care too much about an extra $400?"

On the one hand, that makes sense - if you are trading your points in for cash. On the other hand, that points valuation is inaccurate, at least for someone who places a high value on premium cabin travel. It's...

@David, @Tom: "high income individuals have better things to do than to figure out optimization strategies for travel cards"; "If you make $180,000 per year, do you really care too much about an extra $400?"

On the one hand, that makes sense - if you are trading your points in for cash. On the other hand, that points valuation is inaccurate, at least for someone who places a high value on premium cabin travel. It's not necessarily easy to afford business/first class tickets even if you earn $180k per year. In fact, my family makes more than that, but we frankly can't afford to spend it on $20,000 worth of business class tickets for the family to travel somewhere nice every year. So the extra 20,000 points (a good chunk of a premium cabin ticket) is worth more than $400 to me.

That's why I say most people are ignorant about how to maximize points. It's possible that they simply don't prioritize premium cabin travel - although my conversations with "real" people (i.e., not points aficionados) indicate that's not the case. People like the idea of redeeming their points for first class, but either have no idea how to do it or are convinced that the whole loyalty thing is a scam that will never work for them. So, yeah, someone like that who makes a lot of money is not going to care much about 20,000 points that they can redeem for a $200 statement credit.

LOL, I'm clearly dragging the avg income down :)

Anyone want to trade careers? Hal?Sean?

““The average FICO score of a Chase Sapphire Reserve cardmember is ~785”

seems kind of low for persons in that income range ?”

My score is in the 760s with $300K income mainly because I have so little debt. (No mortgage, car paid off.)

"The average FICO score of a Chase Sapphire Reserve cardmember is ~785"

seems kind of low for persons in that income range ?

You all do realize too its not all about the cards. Chase wants your banking and investment business. If they can convert Reserve customers into the banking and chase private client they will make tons of money and easily recoup all points costs.

Lucky, I'd love to see some numbers thrown at this even if they're estimates. So I'm going to attempt to estimate some numbers, which is very dangerous since I'm far from an expert on this.

So at 1% interchange fee going to Chase (I have no idea if that's accurate), and $39k spent on the card, that's $390 in revenue to Chase. Plus assume everyone uses the $300 credit, that's another $150 in revenue...

Lucky, I'd love to see some numbers thrown at this even if they're estimates. So I'm going to attempt to estimate some numbers, which is very dangerous since I'm far from an expert on this.

So at 1% interchange fee going to Chase (I have no idea if that's accurate), and $39k spent on the card, that's $390 in revenue to Chase. Plus assume everyone uses the $300 credit, that's another $150 in revenue on the annual fee. Rounding up a little and that's $550 in revenue. Let's ignore other fees, like financing fees, for now.

Assuming 50% (I'm making that up) of that $39k on average is in the 3x categories yields 58,500 Ultimate Reward points. Those "cost" Chase what, 1.5 cents each? That's $877.50. And the other 50% in the 1x category is another $292.50 worth of points.

Factoring in the costs for all the other benefits, like Priority Pass, travel insurance, etc. and I can see how Chase loses money without financing charges, people not maxing out the $300 credit, etc.

It is PITA to keep track of the Freedom Unlimited categories that earn extra points. I'll just dump my everyday spend on my Amex SPG and rely on their superior customer service.

I, as David, use it for work travel, and get reimbursed.

Around 95K/yr. worth of flights, rentals and dinners.

I don’t use it at all for my personal stuff, unless going on vacation.

@snic high income individuals have better things to do than to figure out optimization strategies for travel cards. Some do because they enjoy doing it (aka a hobby), but many who seebit as a chore would not do it even if they could squeeze out slightly more value.

@ Hal: Could we become friends? ;)

My numbers are in-line with the average CSR member

@snic

So you spend $39k at 1.5x instead of 1x to get an extra 19,500 points. This is worth maybe $400 at 2c per point. If you make $180,000 per year, do you really care too much about an extra $400? Most people won't bother.

Interesting statistics. I put around $100k annually on the CSR last year (spend that previously used to be split between the CSP and other cards), which is 99%+ either 3x bonused (travel/dining) or foreign currency spend (no FTF). My total USD denominated non-bonused spend on the card was only $163.98 across 11 transactions.

Conversely, I put around 75% of my non-bonused USD spend on the Freedom Unlimited. The remaining spend was on various other loyalty...

Interesting statistics. I put around $100k annually on the CSR last year (spend that previously used to be split between the CSP and other cards), which is 99%+ either 3x bonused (travel/dining) or foreign currency spend (no FTF). My total USD denominated non-bonused spend on the card was only $163.98 across 11 transactions.

Conversely, I put around 75% of my non-bonused USD spend on the Freedom Unlimited. The remaining spend was on various other loyalty cards (eg. Hilton hotel spend goes to Hilton cards, etc..) or to meet minimum spending thresholds for bonuses.

Chase has really locked in my spending with the CSR and I have multiple friends and colleagues who have a similar spending pattern.

considering its only $55 net in annual fee more a year over the Sapphire Preferred, its a keeper for me as I spend about $30k on it a year (half on travel and dining).

I spend about 95k a year at restaurants (partly because vegas/miami clubs and strip clubs are coded as restaurants) So that extra 1pt per $ vs say Citi Prestige is over the $150 cost of the card. So yeah, I'll renew. The other benefits on the card are pretty useless though.

these numbers will go down drastically.

I don't plan to renew this year.

If these numbers are accurate, they underscore how ignorant most people are about how to maximize points. (Maybe that ignorance is particularly pronounced among this higher income echelon?) It wouldn't be that much more complicated to keep 2 cards in your wallet instead of just 1: the Chase Sapphire Reserve and the Chase Freedom Unlimited. Since much of that $39k in spending is likely not on travel and dining, people could earn tens of thousands...

If these numbers are accurate, they underscore how ignorant most people are about how to maximize points. (Maybe that ignorance is particularly pronounced among this higher income echelon?) It wouldn't be that much more complicated to keep 2 cards in your wallet instead of just 1: the Chase Sapphire Reserve and the Chase Freedom Unlimited. Since much of that $39k in spending is likely not on travel and dining, people could earn tens of thousands of points more each year by simply using the Freedom Unlimited for "everything else".

This might be a "second best" outcome from Chase's point of view, because they have to give you more points for the same spend. But it's better than that spend going on a different bank's card.

I also expect there are many who, like me, routinely use it for large expenses that work will reimburse me for rather than having a business card so although I'm spending a large part of my "income" on the card - the largest % of my card spending comes back to me. I pick up several $5-$8K dinner events on this card each year that pay for the card several times over.