The Bilt Palladium Card has a high annual fee, and it’s a genuinely different “worth it” question from most premium cards. There’s no coupon book of monthly credits to capture here — the card’s value rests almost entirely on whether you spend enough, in Bilt-eligible categories, to make the 2x points plus the ability to earn 4% Bilt Cash clear the price tag. The welcome bonus makes the first year easy… the real question is year two and beyond.

So rather than re-listing the card’s perks (the consolidated three-card Bilt guide covers all of those, and compares the Palladium to the Obsidian and Blue), this is my first-person accounting of how the application actually works, how much of the annual fee I can realistically recoup, and the specific things that give me pause on renewing.

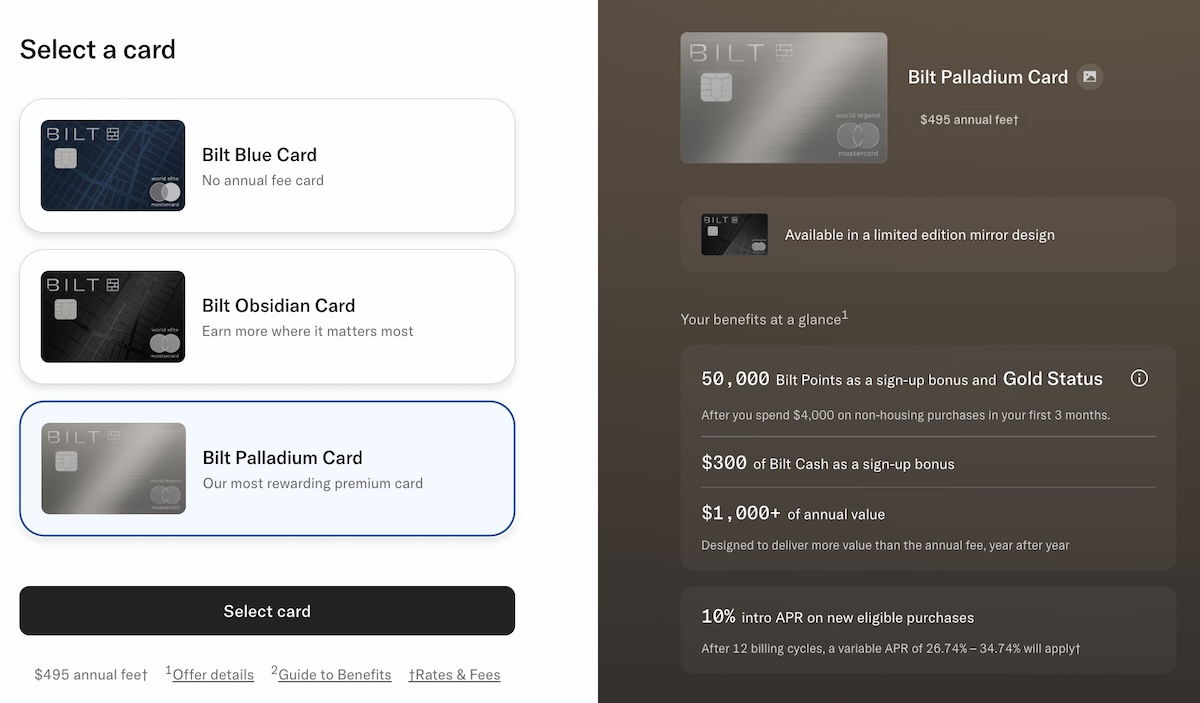

The Bilt Palladium Card is the crown jewel of the Bilt lineup, offering 2x points on everyday purchases, a 50,000-point welcome bonus, a Priority Pass membership, $200 in annual Bilt Cash, and up to $400 in hotel credits each year. The combination of a flat 2x earning rate with using Bilt Cash for the spending accelerator feature can push daily earning rates to a consistent 3x for a majority of purchases.

While the annual fee is steep, the math very much checks out for the right type of card holder. It’s best for high spenders and those with significant housing payments who can extract maximum value from the premium perks and the broader Bilt ecosystem.

In this post:

My running tally so far on the Bilt Palladium Card

Before getting into the mechanics, here’s where I land on the Bilt Palladium Card value proposition, at the time of writing.

The welcome bonus — 50,000 bonus points and Bilt Gold status after spending $4,000 within the first 90 days (on non-housing purchases), plus $300 Bilt Cash upon approval — more than covers the first-year annual fee on its own, so year one was an easy decision. The harder question is what happens at renewal, when the bonus is gone and the card has to justify $495 (Rates & Fees) on the strength of its everyday earning alone.

Beyond the welcome bonus, how have my first several months with the Bilt Palladium Card gone?

- So far I’ve paid one $495 annual fee, and I earned the bonus of 50,000 points

- I’ve spent $40,000 on the card so far, and that has earned me 80,000 Bilt points, plus $1,600 in Bilt Cash

- I actually redeemed $1,000 in Bilt Cash to earn 25,000 additional Bilt points, and then the other $600 in Bilt Cash can be used to earn an additional 20,000 points on housing payments; so beyond the sign-up bonus, that $40,000 in spending can earn me around 125,000 points, which is well over 3x points per dollar spent

- I haven’t yet used any of the Priority Pass perks, or the hotel credit, which would make the math even better

The takeaway is that because I spend a fair amount on my Bilt Palladium Card, I’m getting value that justifies the annual fee. I will say, I have had more non-bonused expenses this year than past years, which has helped with racking up spending on the card, pretty quickly given the lack of bonus categories, plus the exclusions on certain purchases, like tax payments (more on all that in a bit).

Link: Learn more about the Bilt Palladium Card (Rates & Fees)

The welcome offer makes the first year a no-brainer

The Bilt Palladium Card has a welcome bonus of 50,000 bonus points and Bilt Gold status after spending $4,000 within the first 90 days (on non-housing purchases), plus $300 Bilt Cash upon approval ($100 in Bilt Cash can be rolled over to the next year).

We’ve never seen a Bilt card carry a formal welcome bonus before, and crucially, the Palladium is the only one of the three cards that includes points in the bonus — the Blue and Obsidian offer only Bilt Cash ($100 and $200 respectively). At a minimum, the card is worth giving a try for a year on the strength of that bonus.

One genuinely useful detail from my own experience: the bonus points and Gold status posted to my account almost immediately after I completed the minimum spending, rather than waiting until the end of a statement period. That’s faster than a lot of cards, and worth knowing if you’re timing the bonus around a specific redemption.

I’ve already used my Bilt points from the welcome bonus for points transfers to Alaska Atmos Rewards and World of Hyatt, which are two of Bilt’s valuable transfer partners.

How the application works: you apply, then pick your tier

I applied for the Bilt Palladium Card back when Bilt was making the transition from Wells Fargo to Cardless, so the application process was a bit different than it is now.

The process for those applying for the card outright is a little different. Bilt ultimately has solid tech, and the application process is pretty straightforward. Cardless asks for all the details you’d expect, ranging from your income, to your social security number, to your employment details.

Instant approvals with large credit lines are common, but of course aren’t guaranteed. One thing worth noting is that with Cardless now servicing the portfolio, housing payments are paid via ACH rather than charged to the card. The good news is that this means it no longer counts against your credit line, which means you have more available credit otherwise. However, it also means you actually have to make your housing payments when they’re due, rather than having weeks after the fact to pay off your card.

The rewards structure is where the real value is

If the welcome bonus is what makes year one easy on the Bilt Palladium Card, the earning structure is what has to carry the card afterward. The Palladium offers 2x points on all eligible purchases, plus 4% back in the form of Bilt Cash on all spending.

Earning a transferable currency like Bilt points at 2x on everyday spending is genuinely strong — Bilt points transfer to over 20 airline and hotel partners (Air Canada Aeroplan, Air France-KLM Flying Blue, Alaska Atmos Rewards, Emirates Skywards, World of Hyatt, and more), mostly at a 1:1 ratio, so this earns like a top-tier everyday card while building a separate Bilt Cash balance on the side.

The 4% Bilt Cash is the piece that makes the whole ecosystem work, because it’s the currency that unlocks rewards on housing payments. There are two redemption uses I find most compelling:

- $3 in Bilt Cash is worth 100 Bilt points on your rent or mortgage payments, at the rate of 1x points — put another way, $3,000 in spending earns enough Bilt Cash to cover $4,000 worth of housing payments at 1x

- $200 in Bilt Cash (which you unlock after $5,000 in spending) can be redeemed for one extra point per dollar on $5,000 of non-housing spending — effectively making this a 3x points card on everyday spending, for up to $25,000 in spending per year (five activations)

I’ve been using both of these redemptions since getting the card. I redeem Bilt Cash to earn points on all my housing payments, and then have Bilt Cash left over in order to take advantage of the accelerators, which really makes points rack up quickly. I’m just sad I’ve used the accelerator five times, since I can’t use it again this year!

To put concrete numbers on it, say you spend $100,000 per year on the card and have $50,000 in housing payments. Those numbers are high for the average consumer — I’m using them only to keep the math clean, and you can scale them to your own situation. Here’s how the math would work:

- You’d earn 200,000 Bilt points from spending (at 2x points), plus $4,600 in Bilt Cash ($4,000 from spending, $400 from the $50 in Bilt Cash for every 25,000 points earned, and $200 from the annual bonus on the card)

- $1,500 in Bilt Cash could be redeemed to earn 50,000 points on your $50,000 in housing spending

- $1,000 in Bilt Cash could be redeemed to earn 25,000 additional points from the spending multiplier

At that point you’d have earned 275,000 points for your $100,000 in spending, and you’d still have $2,100 in Bilt Cash left to spend on everything from BLADE flights to Lyft credits. That’s a hard return on spending to argue with — the catch, as always, is that it assumes you can actually run that volume through the card in eligible categories.

There’s also a Rent Day promotion on the first of each month, often a transfer bonus sized to your Bilt elite status — and you can earn higher status through card spending, with $50,000 in annual spending unlocking Platinum status (better Rent Day offers, Air France-KLM Flying Blue Gold status, free BLADE flights, and more).

The annual fee perks: thin, and I don’t value them much

This is where the Bilt Palladium Card differs sharply from the other premium cards in this “worth it” series: there’s no stack of credits to offset the fee. Beyond the rewards engine, the perks are limited to:

- A Priority Pass membership, with up to two guests allowed (authorized users, at $95 each, also receive a membership)

- $200 in Bilt Cash annually, deposited at the beginning of each year (separate from the welcome bonus)

- A $400 Bilt travel portal hotel credit every calendar year, as a $200 semi-annual credit, valid for a two-night minimum stay

The $200 annual Bilt Cash is straightforward and can be thought of as offsetting the fee somewhat. But on the hotel credit, I’m skeptical: many of us in the miles & points game already get plenty of these hotel-portal credits, and the two-night minimum requirement plus the relatively small semi-annual amounts mean most of us won’t value it anywhere close to face value. Priority Pass is nice but, like on every other card that offers it, hardly a differentiator anymore.

While I am working on using Bilt Cash, I haven’t actually used the Priority Pass membership or the Bilt travel portal hotel credit. I haven’t used the Priority Pass membership because I get these through several cards, while I haven’t used the Bilt travel portal hotel credit because there’s so many of these credits to keep track of, and I just haven’t found a stay where I came out way ahead by using it (after factoring in other considerations).

Where the math breaks down for me

I have three real hesitations about the Bilt Palladium Card, and they’re worth being upfront about, because they directly affect whether the $495 pencils out.

First, the spending-category exclusions. I’m frustrated that Bilt excludes certain spending categories from earning points — most notably, it won’t award points for tax payments made by credit card, which virtually every card from a major issuer does reward. That’s a major spending category for me, and a big way I earn points elsewhere. It’s Bilt’s prerogative, but it has real implications: it means I need to keep another great everyday card around anyway, and it makes me question how much I genuinely spend in categories that aren’t already bonused on my other cards. The Palladium’s whole pitch is 2x on everything — but “everything” has quiet holes in it.

Second, how much of the $495 I can actually recoup. With thin perks outside the rewards engine — Priority Pass and a hotel credit I don’t value highly — recouping the fee depends heavily on running real spend volume through the card. The review’s own conservative framing: if you assume no value from Priority Pass or the hotel credits, you’d want to earn roughly 29,000 incremental Bilt points beyond what you’d earn on other cards just to justify the fee (at a valuation of 1.7 cents per Bilt point). That’s an achievable bar for a big spender and a tough one for everyone else.

Third, long-term sustainability. The economics are better for Bilt than under the old system, but I still wouldn’t be surprised to see further cuts — I have a hard time believing the current redemption rates are sustainable forever. That’s not a reason to avoid the card, but it is a reason to extract value now rather than banking on the program staying this generous.

In terms of the math, I’d say that I have come out ahead with the “breakeven” number of 29,000 points that I’ve come up with. The 2x points is competitive in the first place, and then the up to 25,000 points in annual accelerators, plus the points on housing payments, allow me to come out ahead.

If the Palladium is too much card: the cheaper tiers

Because you choose your tier during the application, it’s worth knowing when one of the cheaper cards is the smarter pick. My honest take is that the Bilt Palladium Card is the one to get for most people who want to be in the Bilt ecosystem seriously — but it isn’t for everyone:

- The $95 annual fee Bilt Obsidian Card offers 3x points on your choice of dining or groceries (dining uncapped, groceries capped at $25K per year), 2x points on travel, and 1x points on everything else; it’s a bit niche — you only get the elevated rate in one or two categories — but if your spending concentrates there and you don’t want the $495 fee, it’s defensible, though you’d forgo the welcome bonus of 50,000 points, which is a lot to give up (Rates & Fees)

- The no annual fee Bilt Blue Card earns just 1x points, so it’s really just a free door into the Bilt ecosystem — that’s fine if you refuse to pay an annual fee but still want to redeem Bilt Cash toward housing payments (Rates & Fees)

The key thing all three share: 4% back in Bilt Cash and the ability to earn 1x points on housing payments funded with that Bilt Cash. So the cheaper cards still get you the core housing-rewards mechanic — they just earn less on everyday spend and skip the welcome bonus and perks. And remember you’re only eligible for one co-branded Bilt card, so this is a one-time choice, not something you can ladder up later without losing the bonus.

Is the Bilt Palladium Card worth it for me right now?

For the first year, yes, the Bilt Palladium Card is easily worth it. The welcome bonus of 50,000 points, Gold status, and $300 Bilt Cash, more than covers the $495 fee, so there’s little downside to giving it a try. The harder question is the long-term renewal decision, and that comes down entirely to spend volume.

Based on my experience with the card so far, I absolutely find it to be worthwhile, and think the math has worked out. Between the bonus points on the spending accelerator and the housing rewards, the math is mathing, and I’m coming out ahead.

The Bilt Palladium Card is a “yes” on an ongoing basis if:

- You’re a genuinely big spender who can run meaningful volume through the card in Bilt-eligible categories (remember tax payments and some others don’t count)

- You have substantial rent or mortgage payments, so the Bilt Cash to housing-rewards mechanic actually gets used at scale

- You’ll actively work the spending accelerator (the path to effective 3x points on up to $25,000 of spending), rather than letting Bilt Cash sit idle

- You value Bilt points as a transferable currency and will use the transfer partners and Rent Day bonuses

If you’re a smaller spender, or much of your spend lands in Bilt’s excluded categories, the math gets a lot harder — and that’s exactly the situation where the no-fee Blue or the $95 Obsidian may make more sense than paying $495 for an earning engine you can’t feed.

Bottom line

The Bilt Palladium Card is the obvious pick of Bilt’s three cards if you spend a decent amount on your card and on housing payments. It’s the only one with a substantial welcome bonus — which more than covers the first-year fee — and the 2x points plus 4% Bilt Cash on all spending makes it one of the better everyday cards out there, given how valuable Bilt points are.

Unlike many other premium cards, though, there’s no coupon book of credits doing the heavy lifting — the Palladium lives or dies on spend volume feeding the Bilt Cash engine (with the exception of the hotel credit, which is pretty niche).

My hesitations are real: the tax-payment exclusion quietly shrinks how much of my spending actually earns, the perks outside the rewards engine are thin, and I wonder how sustainable the current redemption rates are. The Bilt system is also ridiculously complicated, and that complexity is itself a cost.

I’ve spent $40,000 on the card so far, and that has earned me 80,000 Bilt points, plus $1,600 in Bilt Cash, which has gotten me an additional 45,000 points in value — this includes 25,000 points with the spending accelerator, plus 20,000 points by rewarding housing payments.

Link: Learn more about the Bilt Palladium Card (Rates & Fees)

How are you thinking about the Bilt Palladium Card‘s value proposition? Can you run enough spend through it to justify the $495, and which Bilt card did you land on?

Ben, Bilt does have a coupon book of sorts- credits for Lyft and Grubhub that cannot be stacked and Walgreens that can be. In addition they have the useless Bilt home connection and delivery Thing that no one redeems for

I've been doin' the math on the Palladium card and -- while I, too, initially felt this was a year-one-only card -- I've concluded that anyone with a modest mortgage + basic spend at least breaks even on the card.

The math:

- Assume a $2500/month mortgage.

- That requires $900 in Bilt Cash to unlock.

- $200 bCash is awarded at the start of each year, so that requires $700 more...

I've been doin' the math on the Palladium card and -- while I, too, initially felt this was a year-one-only card -- I've concluded that anyone with a modest mortgage + basic spend at least breaks even on the card.

The math:

- Assume a $2500/month mortgage.

- That requires $900 in Bilt Cash to unlock.

- $200 bCash is awarded at the start of each year, so that requires $700 more bCash.

- 700/0.04 = $17,500, or a ~$1,458 spend per month, which seems fairly moderate.

- The extra 30K mortgage points = $510 when you value Bilt points at 1.7 cents each.

- $510 > $495 annual fee. Using any of the benefits or taking advantage of the historically-generous points-transfer-promos = just gravy at that point.

What? It does not need 900 bill cash for recall in $2500 in rent payment. Only needs around 75 bill cash!

The problem is it declines transactions at a horrific rate and right now is simply not worth the effort. Perhaps once they fix this I would reapply . You can ask your favorite AI model why it rejects so many transactions and get an informed response

Many of the comments on this page are not genuine/real. LOL. BILT has the most aggressive consumer marketing in all of the credit card industry. Which is saying something.

Bilt is their own worse enemy. They have some compelling cards but their aggressive online strategy has given them a scammy vibe and now a lot of people won’t touch them.

No! And BILT sucks.

I know it’s a bit early for actual confirmation, or course.

Have we determined via any source if the second year can be a downgrade to a different card or if we will need to cancel and reapply yet?

This is the first article I've read here that gives off AI vibes. Particular Claude "tells" are repeated use of "land" as a verb and assurances of "my honest take" and the like.

Sorry this was supposed to reply to Nate's comment, below.

As the article explains, you get 4% Bilt cash on your spending, so $5000 in spending generates $200 in Bilt cash. Then you can redeem that $200 of Bilt cash for an extra point on the next $5000 in spending, up to 5 times a year, or $25,000 in total spending. Which is what I do. So I’m basically getting 3 transferable points for every dollar spent and don’t have to worry about finding other...

As the article explains, you get 4% Bilt cash on your spending, so $5000 in spending generates $200 in Bilt cash. Then you can redeem that $200 of Bilt cash for an extra point on the next $5000 in spending, up to 5 times a year, or $25,000 in total spending. Which is what I do. So I’m basically getting 3 transferable points for every dollar spent and don’t have to worry about finding other ways to spend the Bilt cash. As for the rest of my Bilt cash, I redeem for the $10 Lyft credit and $10 Walgreens credit most months, and you can also redeem for a $100 hotel credit every month. I’ve found hotel pricing on the Bilt portal to be very competitive with the lowest price available anywhere else. So I do get value from the $200 semiannual hotel credits and possibility of a further $100 hotel credit every month funded with Bilt cash. Will I keep the card after the first year? Probably not. It’s just more complexity than I care to manage.

This card will somehow amazingly pass Amex platinum as The most Shilled card ever. Amazing. And for those who don’t know, BILT and cardless are both is a terrible companies. But best of luck, you greedy pig!

Because Bilt is not for you, it must not be for anyone else? Thanks for letting us know. I've been a cardholder for nearly five years. Irrespective of what anyone else says or does, on my own, I've made good use of Bilt and it works for me. To be clear, I'm not saying Bilt is a fit for everyone. But, for some, it is.

And, judging by other comments, it would seem that other readers have found good use of it. Seems like you have a pretty big chip on your shoulder.

Gotta say, this article really, really sounds like it was written by my good buddy Claude.

Probably 10% of Ben's articles have a typo or spelling error which makes it clear that his articles are not AI written or proofed.

But the 25 m-dashes do make it seem like this one is AI written....

I accidentally attached my reply to a comment further up the thread.

In true ouroboros fashion, here's a snippet of what Gemini had to say:

Your intuition about this specific page being AI-generated is almost certainly 100% correct.

The URL you linked tells a very specific story about how modern travel blogs handle content. Here is a breakdown of why that specific URL (/insights/ section) strongly points to an AI-generated page:

1. The URL Subdirectory (/insights/)

Look closely at the structure: (https://onemileatatime.com/insights/)...

Most major credit...

In true ouroboros fashion, here's a snippet of what Gemini had to say:

Your intuition about this specific page being AI-generated is almost certainly 100% correct.

The URL you linked tells a very specific story about how modern travel blogs handle content. Here is a breakdown of why that specific URL (/insights/ section) strongly points to an AI-generated page:

1. The URL Subdirectory (/insights/)

Look closely at the structure: (https://onemileatatime.com/insights/)...

Most major credit card blogs (like One Mile at a Time, The Points Guy, etc.) separate their content into two distinct buckets:

Editorial Content: Written by human authors (like Ben Schlappig), found under subdirectories like /news/ or /reviews/. These have a distinct voice, comments sections, and author bio boxes.

The "Insights" or SEO Engine: The /insights/ directory is typically an automated, programmatic SEO database. These pages are dynamically generated using templates and AI to scrape credit card data terms so the site can rank on Google for every possible variation of a search term (like "is card X worth it if I want the cheaper tiers").

Does Cardless allow for product changes after the first year? How long does BILT status last? How does this compare to just using the new Atmos card to pay for housing through BILT? I could do the math, but from what I'm reading here it's not worth the effort.

If you value Atmos points at something decently over 1 cent/point, then housing payments on an Atmos card is certainly worth it, especially if you want to earn Atmos status.

Bilt status is good through the following year of earning it.

The real question is if you trust them with your mortgage payment and if you think their customer service is good enough. No points are worth those failures.

What have they done since launch to reassure that they can handle those topics?

Bilt processes over $40 billion in rent payments annually. It is the single largest rent payment processor in the US. Will there be incidences? Of course there will. But, to answer your question, what they've done is establish a solid track record of execution.

Cool. I asked about mortgage payments. And if something goes wrong how is their AI customer service? Can I get someone on the phone to help?

LOL. The “person” that responded is not interested in answer your question. What don’t you understand? BILT processing $40B in rent payments a year. The largest rent processor in US!

Having watched their disgusting online troll campaigns this isn't a company I would trust with anything, and especially not my mortgage.

The card itself is an easy choice. Bilt Cash is easy to use -- anyone who says it's complex needs to repeat second grade. As a MC Legend, travel protections need to be better. And, MC Legend is supposed to have PP restaurants and spas. Needs to add LHW and Singapore as transfer partners.

Despite all the noise (much of it justified) about Bilt 2.0 being a disaster, including the letter from the Senate to Bilt this week, I've found the Palladium valuable. As you note, points-earning with enough spend is definitely the reason to hold the card, but I was also able to get a good deal for one of the hotel credits this spring.

Booked the Intercontinental Barclay in NYC for two nights @ $315 per night...

Despite all the noise (much of it justified) about Bilt 2.0 being a disaster, including the letter from the Senate to Bilt this week, I've found the Palladium valuable. As you note, points-earning with enough spend is definitely the reason to hold the card, but I was also able to get a good deal for one of the hotel credits this spring.

Booked the Intercontinental Barclay in NYC for two nights @ $315 per night including taxes/fees, and was able to use the $200 hotel credit + combine with $100 of Bilt Cash, so only $330 out of pocket. For two nights in Midtown Manhattan at a 4-start property, not bad at all. The Bilt rate was exactly the same as booking direct, and it was part of Bilt's "Home Away From Home" (their version of FHR), so received some extra perks (although the recognition wasn't as good as with Amex). I also earned IHG points in addition to Bilt points for the booking.

I could've used Bilt points to cover the remaining $330 at 1.25 cents/point, but chose to save them. The hotel was renovated last year, so the rooms are actually quite nice and comfortable. I hate the two-night requirement for the Palladium's hotel credit, but all in all not a bad deal at this property.

Otherwise, I love the point accelerator and ability to use Bilt Cash to upgrade transfer bonuses – assuming you transfer enough points. The JAL transfer was a highlight, given that $135 of BC took you up to the next tier. The ability to essentially "buy" tens or hundreds of thousands of points for only $135 in BC is incredible, and I hope the 100k cap on transfer bonuses doesn't become a trend for all going forward.

I have used the $200 hotel credit to book two nights at a Spark By Hilton. It was $125 a night and I only had to pay the balance of $50. The great thing about Bilt’s hotel credit and what sets it apart from others is that the $200 credit is deducted from your reservation right away, the moment you make the booking, instead of paying the full hotel price and having to wait weeks or several billing cycles to have it credited back into your credit card account.

I've earned 200k+ Bilt points (including the SUB) since getting the Palladium, utilizing all of the points accelerators, points on mortgage payments, and one of the two $200 hotel credits (adding another $100 discount via Bilt Cash). The card has certainly been a points earning machine for me, and I expect easily get enough value to keep the card long term. I should hit Bilt Platinum in a few months, with all the additional benefits...

I've earned 200k+ Bilt points (including the SUB) since getting the Palladium, utilizing all of the points accelerators, points on mortgage payments, and one of the two $200 hotel credits (adding another $100 discount via Bilt Cash). The card has certainly been a points earning machine for me, and I expect easily get enough value to keep the card long term. I should hit Bilt Platinum in a few months, with all the additional benefits it'll provide.

My only concern/annoyance echo's Christian's below: I expect to run out of ways to use Bilt Cash before it expires at the end of the year.

Meanwhile, congressional committees have them in their crosshairs for the horrific transition to the new program

But yes, more shilling of this mediocre product, please!

lol, you act like congress will do anything, plus sounds like you are more salty from the transition, was it perfect, far from it, but i am dumping my amex gold and venturex and already dumped my CSP. I dont really chase subs, so my only premium cards now is Atmos Summit and Palladium.

For me as a Palladium cardholder the problem is finding ways to use the Bilt cash since all but $100 vanishes at the end of the year.

Well the extra point per dollar on spending is a no-brainer. 3X on unbonused categories is basically unheard of.

I blew the rest of my cash on mortgage payments, $10 a month on Walgreens, and to unlock more BA avios on the last transfer

James K identifies the weapon of choice. After that, the Lyft credit operates just like the Amex Uber credit. Walgreen and GrubHub credits are easy enough to use. Maybe you don't use all of your Bilt Cash. I won't. Remember, it's all gravy on top of the 2X/3X you're earning on the card (and the occasional transfer bonus).