Curve is in the process of launching in the United States. This has the potential to be a game-changer for many people using rewards credit cards, though there are some restrictions to be aware of. While I first wrote about this in the summer of 2021, people are now starting to be invited to apply for Curve, which is a sign that this product will become a reality.

If you’re not yet eligible to apply, I’d recommend getting on the Curve waitlist. This will give you an extra bonus when the time comes to apply, and there’s no obligation to actually get the product.

In this post:

What is Curve?

The concept behind Curve is fascinating — it’s a credit card you can make payments with, and it can be linked to your rewards credit card. Here’s the general idea when you get Curve:

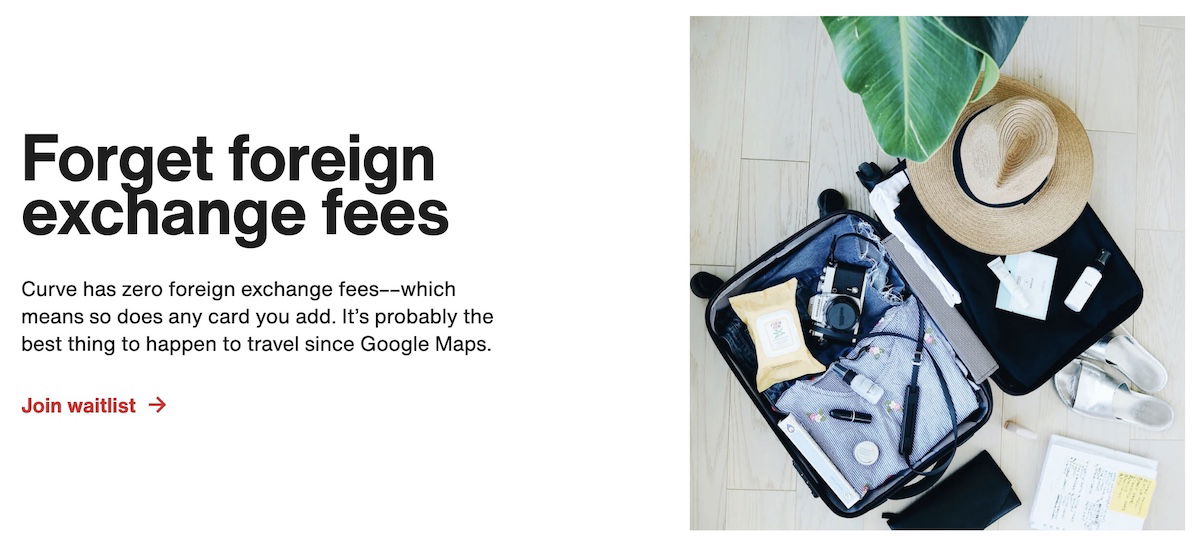

- Curve allows you to link credit cards with major issuers; unfortunately in the United States, only Mastercard, Diners, and Discover work initially, while Visa and American Express don’t work yet

- Then you can make all of your purchases with your Curve credit card, rather than using individual credit cards — essentially Curve pays the merchant, and then Curve charges your credit card

- One of your designated individual credit cards will be charged through Curve for those purchases — transactions will still show up on your individual credit cards, but there will be a note making it clear that the purchase was through Curve, though you’ll still earn bonus points based on the merchant you made the purchase with

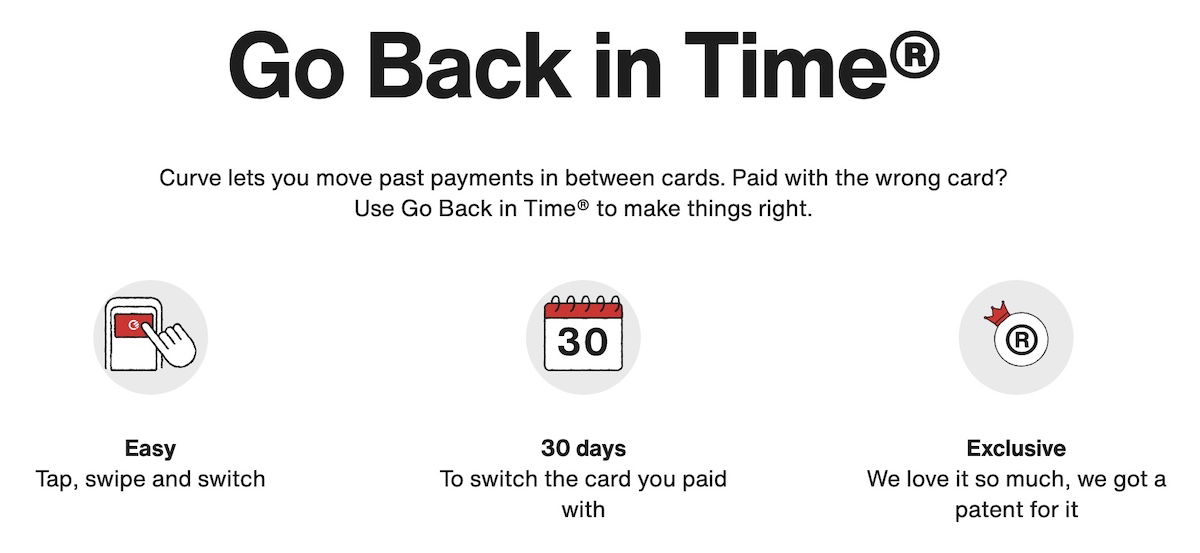

- There are plenty of advantages to using Curve — there are no foreign transaction fees, you can switch the card you paid with for a period of 30 days, Curve offers contactless technology, and more

The concept might sound wild, though Curve has existed in the United Kingdom for a while, so this has been tried and tested elsewhere. Now it’s coming to the United States.

What are the benefits of using Curve?

Above I explained some of the basic features of Curve, though let me give some more concrete examples:

- The Citi Double Cash is one of the best card for everyday spending, but it has foreign transaction fees; you could use Curve to make payments abroad with no foreign transaction fees, and then have it charged to the Citi Double Cash

- If you’re looking to maximize credit card rewards, you can change the card you’ve used to pay for a purchase for 30 days; this can be useful if you didn’t use a card with the right bonus category, or if you have a spouse who isn’t great at using the right credit card for the right kinds of purchases

- If you join the Curve waitlist now (more on that below) you can earn 1% back on purchases for the first six months, in addition to your credit card rewards

How does Curve make money?

You might be thinking to yourself “this sounds too good to be true, so what’s the catch, and how does Curve make money?” Well, that’s a great question.

Like so many companies nowadays, I’m guessing the answer is that Curve probably won’t make money, or at least isn’t looking to make money directly from consumers. I’m guessing venture capital companies will be funding these rewards, and that this is a play for collecting data on consumers, market share, etc.

Curve waitlist & refer-a-friend program

Curve isn’t yet open to the general public, but you can get on the Curve waitlist. All beta users who join the waitlist will receive an additional 1% cash back on every purchase for the first six months, in addition to the credit card rewards that they earn. On top of that, you’ll be invited to apply early. Note that for the cash back bonus, paying taxes, paying for insurance, or buying gift cards, won’t qualify for that bonus.

Last summer there was a promotion whereby those in the top 100 spots on the waitlist would receive 10% cash back on their purchases for the first six months, for a total of up to $1,000 in rewards. I received an email indicating that I was in the top 100 spots, and received an invitation to apply (I know there’s a hard pull here, but I’d assume this doesn’t count as a new product toward the 5/24 limit… or does it?).

OMAAT readers are welcome to leave their referral codes in the comments section, so that others can use them (and please use those and not mine — after all, I’ve already gotten my invite to apply).

Bottom line

Curve is in the process of launching in the United States, and select people are now being invited to apply for the card. This could provide very useful for anyone collecting miles & points. Curve essentially lets you use a single payment card, and then link several other cards so that you can maximize your rewards with every transaction.

If you join the waitlist now, you’ll even be able to earn 1% cashback on your purchases for the first six months, on top of the credit card rewards you usually earn. There’s plenty of long-term value beyond that, like no foreign transaction fees (which pairs nicely with cards that are rewarding but have foreign transaction fees), the chance to change which card you use for transactions after the fact, and more.

What do you make of Curve? Could you see yourself using it?

So this turned out to be a very poor product. They closed my account today forfeiting unredeemed cash back. without any warning or grace period.

Good concept, but the implementation is super buggy for now. Some transactions randomly get assigned to Curve Credit, so you lose the extra rewards you'd get if you used the rewards card directly. Even worse, sometimes transactions are declined after the fact, so you have to keep an eye on your emails in case you have to go in and submit another payment method. Not worth the hassle at the moment.

I just got an email telling me I'm off the waitlist. The 30 day back in time feature has this lovely term per the card agreement:

Be aware your Linked Card issuer may charge you a fee for this and may classify the transaction as a balance transfer. We encourage you to check with your Linked Card issuer.

Can anyone who got this card in March 2022 confirm their use of this feature...

I just got an email telling me I'm off the waitlist. The 30 day back in time feature has this lovely term per the card agreement:

Be aware your Linked Card issuer may charge you a fee for this and may classify the transaction as a balance transfer. We encourage you to check with your Linked Card issuer.

Can anyone who got this card in March 2022 confirm their use of this feature and how their Linked card classified this transaction? I presume I will have a hard time asking my bank about this feature since it's so new.

Well I didn't get far. I got a "So Sorry! Based on the information you provided you are not eligible for a Curve account right now. And, for security reasons, we can't provide you with more info about this." message on the app, and any subsequent launch of the app takes me directly to this message. And they also sent me an email telling me to complete my Sign Up on the App so that I don't miss out on any cashback. What gives?

when you say "spouse" we know youre referring to the wife. they never know what card to use where and when. i trained mine right. every screw up came out of her pocket and i got to have my way for the night...

The big issue is that they do not cooperate with Visa or American Express. I assume that the charge will come through as a technology company or a finance company so for people that are at a restaurant for example, this does not work well if they are charging to a card that gives them more for dining. Also, if there is no credit card symbol such as Visa or Mastercard on the card I...

The big issue is that they do not cooperate with Visa or American Express. I assume that the charge will come through as a technology company or a finance company so for people that are at a restaurant for example, this does not work well if they are charging to a card that gives them more for dining. Also, if there is no credit card symbol such as Visa or Mastercard on the card I assume that many service staff will assume they do not accept it or will not know what is going on.

So they actually have a logo on the card, which is Mastercard, which process the purchase. They now accept visa debit cards and I am certain they will add all other issuers soon. It’s just in beta.

No, Curve is not launching in the US anytime soon. This is about the third or fourth time they're hyping a US Launch Wait List most likely because they're burning through cash and are desperate to raise additional capital. Seeing this Dud hyped yet again on the travel reward blogs probably means Curve is promoting an affiliate marketing promotion for blog sites.

Having had a Curve Card in Europe, their Customer Service is about...

No, Curve is not launching in the US anytime soon. This is about the third or fourth time they're hyping a US Launch Wait List most likely because they're burning through cash and are desperate to raise additional capital. Seeing this Dud hyped yet again on the travel reward blogs probably means Curve is promoting an affiliate marketing promotion for blog sites.

Having had a Curve Card in Europe, their Customer Service is about Last in Class and they're definitely not ready for Prime Time or a launch anywhere else.

I just got my card 2 days ago

Many cards would treat the payment to Curve as a cash advance (similar to when I add money to my Draft Kings sportsbook app using my Chase Sapphire Reserve for example). If so you may get a fee (Chase charges me $10 for each deposit to a sportsbook) and also have to pay interest since there typically is no waiver from interest accruing on cash advances. Also do you really want a middle man between...

Many cards would treat the payment to Curve as a cash advance (similar to when I add money to my Draft Kings sportsbook app using my Chase Sapphire Reserve for example). If so you may get a fee (Chase charges me $10 for each deposit to a sportsbook) and also have to pay interest since there typically is no waiver from interest accruing on cash advances. Also do you really want a middle man between you and your credit cards. I already have that situation with PayPal and my Apple Pay account but at least there I'm dealing with mature companies and proven technology. As an IT professional for almost 40 years there is NO WAY I would use a curve card (regardless of any benefits) at a front end processor for my credit cards. Too many potential points of failure as well as hacker risk with yet another party involved. Also, if there is an issue related to any payment (or settlement to curve) I can't wait to see the finger pointing.

Bottom line, things that sound too good to be true rarely are and this seems like a potentially costly (and dangerous) practice.

How is Apple Pay an account? It’s a middleman from a transaction mechanism standpoint, but not a financial one. You’re directly charging your card. There’s no Apple Pay account; the virtual credit card number stored in the Secure Enclave of the device is the bank’s number, and the bank cross references it during a transaction to your real number, which is why you need bank participation for it to work.

LOL @ working with Diner Club. We can all thank BMO Harris for tombstoning that program.

That's up there with "works with JCB."

"How does Curve make money?"

They sell your transaction data. Is that a sustainable business model? ¯\_(ツ)_/¯

Except for the no int'l fee, I don't see any real benefit (except for you Ben, REFERRALS!).

And given that there's 1.5% cash back cards with no intl fee (and Apple Card at 2% via NFC), that extra 0.5% on non-bonused spending is a *really* small benefit.

And if your points/miles life is so complicated that you...

"How does Curve make money?"

They sell your transaction data. Is that a sustainable business model? ¯\_(ツ)_/¯

Except for the no int'l fee, I don't see any real benefit (except for you Ben, REFERRALS!).

And given that there's 1.5% cash back cards with no intl fee (and Apple Card at 2% via NFC), that extra 0.5% on non-bonused spending is a *really* small benefit.

And if your points/miles life is so complicated that you need to switch transactions after the fact routinely, you're doing it wrong.

@ Never In Doubt -- At a minimum, you could use the Citi Double Cash with Curve for six months to get the equivalent of 3% cash back. That's an extra 1.5% compared to your example, and not an extra 0.5%.

Ben, of course you are correct on the math.

That math appeals to...

US credit card users who use a cash back card that's currently unusable internationally because of its fee.

How many of those people who *already* don't have a better option for un-bonused intl spend are suddenly going to want to spend a lot outside the US? They're unicorns.

As for the, "I'll grab it just for six months of 1% more!" folks, you're way beyond me on micromanaging your benefits.

"And if your points/miles life is so complicated that you need to switch transactions after the fact routinely, you're doing it wrong."

The incentive here for me would be the ability to reduce the number of cards I'm carrying while still optimizing bonus categories. I'm a big fan of the slim wallet/phone case with a couple card slots type of setup so being able to reduce the cards I carry around for everyday use to...

"And if your points/miles life is so complicated that you need to switch transactions after the fact routinely, you're doing it wrong."

The incentive here for me would be the ability to reduce the number of cards I'm carrying while still optimizing bonus categories. I'm a big fan of the slim wallet/phone case with a couple card slots type of setup so being able to reduce the cards I carry around for everyday use to one, then just properly reconcile the transactions to the card with the best return later has some appeal.

Re: the foreign transaction fees I actually ran into this somewhat recently. I made a donation to an international charity denominated in their local currency using Paypal and it didn't even occur to me I had my Freedom set as the default payment option until I'd already completed the transaction. For a small dollar amount one off like this it's not that big of a deal to eat the fee, but being able to easily just move it over to a no-FTF card would definitely be a nice QOL thing.

Rob P, if you’d use a giant wad of *physical* cards for in person purchases, you’re doing it wrong.

Google “Pareto principle”.

You can thank me later.

As long as you don't use Go Back In Time, it preserves the MCC code - extra 1% (or 10%) on top of original card rewards is pretty good IMO

You can actually assign cards per category making it really easy. Just carry the curve card and a backup card and you can leave your miles and category rotating cards at home. Just pay with curve and the right card gets charged.

As per my knowledge we can add it to Apple and google pay. Also it is not completely like coin. Coin took $50 but this is for free. That means we are not loosing anything in Curve. Also Coin card has some electric button type to change card you use and have limit for number of cards we can add. Also no rewards in Coin. No option of changing payment to one to other card....

As per my knowledge we can add it to Apple and google pay. Also it is not completely like coin. Coin took $50 but this is for free. That means we are not loosing anything in Curve. Also Coin card has some electric button type to change card you use and have limit for number of cards we can add. Also no rewards in Coin. No option of changing payment to one to other card. I feel that no risk in trying it. It avoids carrying different cards in wallet and probability of missing cashback is very less.

I've had the Curve card in Europe for a few years. I've not used it extensively, and I had an issue once where I tried to pay using the Curve card, and the money was taken from the backing credit card, but the payment didn't go through at the merchant. I complained and got a refund from Curve, but the issue has put me off using it too much going forward.

Coin was just hardware for lack of a better term. I had one and loved it and was disappointed when it shut down.

Being a Brit, I have held a Curve card for four years now, and your right, once you get your head around the way it works... It is simply amazing. So personally would recommend looking at the "waitlist". And btw I am not employed or have any connection to Curve, only someone who has the card as a general consumer and happy with what it offers.

Nick, you’re very enthusiastic, but non-specific, what is “amazing” about it?

One thing that would appeal to me is that I would only have to remember one PIN, i.e. the Curve PIN. Also, here in the UK there's only a very limited number of debit and credit cards that do not charge foreign exchange fees (luckily I've got those). The ones that do typically charge 2.99% and sometimes a flat fee of £1 or £2 on top of that. In their T&C's they say they use...

One thing that would appeal to me is that I would only have to remember one PIN, i.e. the Curve PIN. Also, here in the UK there's only a very limited number of debit and credit cards that do not charge foreign exchange fees (luckily I've got those). The ones that do typically charge 2.99% and sometimes a flat fee of £1 or £2 on top of that. In their T&C's they say they use a fair exchange rate collected from their wholesale provider. I don't know though how that compares to the true Mastercard exchange rate.

That makes some sense if your options for no intl fee cards are so limited.

That’s not really a problem for Americans.

It's not remotely amazing. I've had it for years too and very rarely use it.

I can see why people like it (no FX fees on weekdays, swapping transactions between cards), but it has been gutted from what it originally was and is now largely pointless.

Can the underlying card be in another person's name? (Essentially can the Curve card act like an FX-free supp card?)

I don't know about officially but I've had no problems doing this. Note that each card can only be added to one persons Curve account. This causes issues if your supps have exactly the same card details as you as only one of you can add the card to your Curve account

I see, still sounds good though, thanks very much!

What would the transaction be classified as?

If Curve is making the payment and then in turn charging your credit card, the transaction is settled between the card issuer and Curve instead of the card issuer and the merchant, right? What happens to the insurance, purchase protection, and other benefits that would otherwise normally apply?

Do bonus point categories still work? What about more specific cases like adding a World of Hyatt credit to Curve and using the Curve card at a...

If Curve is making the payment and then in turn charging your credit card, the transaction is settled between the card issuer and Curve instead of the card issuer and the merchant, right? What happens to the insurance, purchase protection, and other benefits that would otherwise normally apply?

Do bonus point categories still work? What about more specific cases like adding a World of Hyatt credit to Curve and using the Curve card at a Hyatt; would I still get the bonus points there?

Those are questions that we don't currently know the answer to.

I have been using it in the Europe until recently when my bank dropped fx charges. Curve does pass on some merchant ID's as some of my payment do register as specific purchases under the auto accounting at my bank. It isn't full proof in my experience.

Hyatt is Visa, so that's a nonstarter there. :(

If they pay first, then route to my actual card, wouldn’t my actual card see a charge from Curve, not the actual merchant?

If I change the actual card on day 29, would not the new card see it as transaction on day 29, thus extending grace period?

Curve's Customer Support is only available by email and their Customer Service is about the worst I've experienced. Would not use Curve Again if you paid me.

Think the chances of Curve launching in the US are low and the probability of Curve being able to continue to do business in the US if launched are even less.

Somebody please explain to me how adding another middle man would benefit me or make the transaction fees lower?

I get that you have the intro 1% for 6 months, then what?

What about the more you refer, the higher on the list. This is a new Ponzi?

Another startup trying to solve a problem that we don't have.

The product is more useful in the EU market where they started with many banks having fx fees.

I think this might be useful more to people of lower income levels/credit score who might not have access to credit cards without fx charges. It has always been a niche product and in most cases will stay that way.

LOL, no fx charges?

Did anyone care to tell us what fx rates will be used?

I would be more than happy to pay fx fees over dynamic currency conversion all the time.

I agree about the niche product, but how will they even survive. I have tendency to not give personal information to companies that would likely fail. Yes, they protect your privacy. But up until they cease operations, and after maybe the highest bidder?

I'm with you, Eskimo. This does not sound like a sustainable business model, and there could be some unexpected issues (such as problems with refunds, not getting credit card protection, etc.). I am also concerned about privacy. Not even tempting for me because I have none of the cards they work with, but even if I did, I think I would skip it.

I'm with you, Eskimo. This does not sound like a sustainable business model, and there could be some unexpected issues (such as problems with refunds, not getting credit card protection, etc.). I am also concerned about privacy. Not even tempting for me because I have none of the cards they work with, but even if I did, I think I would skip it.

I've used Curve for a couple of years now in the UK - my referral link is http://www.curve.app/join#GSVVI

I must be missing something. The Citi Double Cash is cited but, the Capitol One Venture gets 2X for everything. Is the Double Cash actually better than the Venture?

No, I think Ben just wanted to use an example of a common card with an intl transaction fee that would be "improved" by the Curve product.

I’ve had Venture and currently use Double Cash. They’re both good cards with 2% rewards. The only downsides to Double Cash are the foreign transaction fee, and the $25 minimum for cashing in a reward. Otherwise, I prefer Double Cash because $25 cash is a little more useful than applying $25 to travel expenses, and Venture charges an annual fee of nearly $100. Even though Venture will reimburse you for a Global Entry application, that's...

I’ve had Venture and currently use Double Cash. They’re both good cards with 2% rewards. The only downsides to Double Cash are the foreign transaction fee, and the $25 minimum for cashing in a reward. Otherwise, I prefer Double Cash because $25 cash is a little more useful than applying $25 to travel expenses, and Venture charges an annual fee of nearly $100. Even though Venture will reimburse you for a Global Entry application, that's still less flexible than a cash rebate.

The Double Cash is better than the Venture for one reason: No annual fee. But it does have foreign transaction fees (unlike any cap one card).

As European user of Curve for 2 years and 20+ card Business specialist I can say:

1. Curve will never make money, they will always bring losses. Fees they need to pay are significantly higher than income from interchange. As consumer obviously I don’t care :-).

2. It is not exactly true there are no currency exchange fees. Curve charges extra over weekend. Also there is a fee if you exceed quite low...

As European user of Curve for 2 years and 20+ card Business specialist I can say:

1. Curve will never make money, they will always bring losses. Fees they need to pay are significantly higher than income from interchange. As consumer obviously I don’t care :-).

2. It is not exactly true there are no currency exchange fees. Curve charges extra over weekend. Also there is a fee if you exceed quite low monthly limit.

3. There is no way that issuer of linked card will treat purchase as made in particular merchant. It will always see it as Curve payment. So no increased bonus if you paid at the hotel for example.

4. Personally I use possibility to change card charged quite a lot.

3. isn't quite that simple - Curve passes the MCC , so if it's a travel spend then you'd get the bonus points if you use a travel bonus card for example. But if you get points for spending at a Marriott then that won't work as you're right, they see it as *CRV Marriott XYZ instead of Marriott

Please explain “Curve charges extra over weekend.”

This is copied from the UK terms and conditions:

"Weekend exchange rate. This is the rate at the time the markets are closed in London, UK. It will apply from the time the markets close until they open again."

I assume they add a little something to the exchange rate they use (and charge your account with) in case it moves unfavourably before Monday (when they have to settle with their wholesale currency provider).

During weekend they add commission of 0,5%-1,5%. They claim it is to cover currency fluctuation risk.

So, can it route grocery transactions to a certain card, travel to another, dining to another?

No.

Where did you get that idea?

But that *would* actually be a benefit!

Maybe what confused you is the ability to *change* what card a transaction was routed to *after* the fact.

That seems to be a small benefit, but, again, how complicated is your life if you regularly need to do something like that?

Quarterly categories change. Overall cards get refreshes where categories change. You may need a specific type of transferrable point for an upcoming redemption. Your authorized users (such as a spouse) may prefer to use a single card, leaving points on the table.

There are any number of potential reasons this could come in handy. I'd be excited for the idea of going through once a week and making sure the most lucrative card was used...

Quarterly categories change. Overall cards get refreshes where categories change. You may need a specific type of transferrable point for an upcoming redemption. Your authorized users (such as a spouse) may prefer to use a single card, leaving points on the table.

There are any number of potential reasons this could come in handy. I'd be excited for the idea of going through once a week and making sure the most lucrative card was used for every purchase. Leaving points on the table is giving away money.

Actually, yes, it can. There is a option in the app where you can create rules based on category as well as transaction amount.

So for example, gas purchases go to a specific card, grocery purchases to another card, and so on.

At least on the USA, the biggiest problem is that they don't currently accept VISA credit cards (they do accept visa debit). They also don't accept American express at all. The...

Actually, yes, it can. There is a option in the app where you can create rules based on category as well as transaction amount.

So for example, gas purchases go to a specific card, grocery purchases to another card, and so on.

At least on the USA, the biggiest problem is that they don't currently accept VISA credit cards (they do accept visa debit). They also don't accept American express at all. The beta email they sent noted these limitations and claimed that they are working on a solution to support VISA credit cards. Honestly this is the only major issue that's holding me back from using this service a lot more frequently.

Isn't this basically like Coin, which promised something similar and then launched in 2015 only to shut down in 2016?

Yes, exactly.

As for my knowledge it is not completely like coin. Coin took $50 but this is for free. That means we are not loosing anything in Curve. Also Coin card has some electric button type to change card you use and have limit for number of cards we can add. Also no rewards in Coin. No option of changing payment to one to other card. I feel that no risk in trying it. It avoids carrying different cards in wallet and probability of missing cashback is very less.

Not really. Coin was a product that actively mimicked whatever cards you copied onto it; the payment terminal wouldn’t be able to tell the difference between the Coin and the real card. Coin died because unlike with old magnetic stripe cards, you can’t easily copy over the information from a chip card, and this was post-Target hack when all the card issuers started pushing hard for chip reader terminals.

Meanwhile, this thing behaves as a...

Not really. Coin was a product that actively mimicked whatever cards you copied onto it; the payment terminal wouldn’t be able to tell the difference between the Coin and the real card. Coin died because unlike with old magnetic stripe cards, you can’t easily copy over the information from a chip card, and this was post-Target hack when all the card issuers started pushing hard for chip reader terminals.

Meanwhile, this thing behaves as a passthrough, slurping up all your transaction data. Coin was a little gimmicky; this is much, much worse. Honestly it’s disappointing to see Ben promoting this.

İt is a credit card , read the updated t&c

Joining the waitlist to apply for a Curve credit card does not guarantee eligibility for the card.

Isn't the U.S. Curve product going to be a credit rather than a debit card and, if so, how does this change the value proposition?

@Never In Doubt - only ever having to carry a single card, but being able to maximize rewards by putting each purchase on the best card for it, would be pretty big for me. Even when I have carried several different rewards cards, I have a hard time keeping track of which is best to use at a given time.

Don’t have Apple Pay or Google/Android Pay?

If your use of in person physical cards is so complex/burdensome because of the vast number of them, you’re doing it wrong.

You’re also confused, nothing about Curve helps you “keep track of which is best”.

If you're not sure what the MCC is, you could put the spend on Curve first, then redirect the spend to the card with the bonus cat after.

Edge case at best!

But I guess if you're making lots of big charges with uncertain coding (really?), and micromanaging the f**k out of them, this is the offer for you!

Best of luck with the referral clicks, but except for “eliminate intl transaction fees from a card”, which is likely an edge case for most OMAAT readers, where’s the benefit?

The benefit is that you can lose your Curve and whoever finds it has access to a whole bunch of your cards! :)

No they can't. Only if they have the app, your password and secondary authentication details AND they have gone through a series of questions and answers when you install the app and get all of them right. So I feel better security than most credit card companies...5

Even that's not a benefit. I'm not liable for CC charges. Why go through extra contortions to help CC companies out? Seems like a waste of effort.

Do you think this can be used for rent payments for landlords that accept debit cards?

It's a credit card, according to the T&C

Joining the waitlist to apply for a Curve credit card does not guarantee eligibility for the card.

Yes in the UK it can be as long as the card that you nominate to take the payment has enough cash in that account.