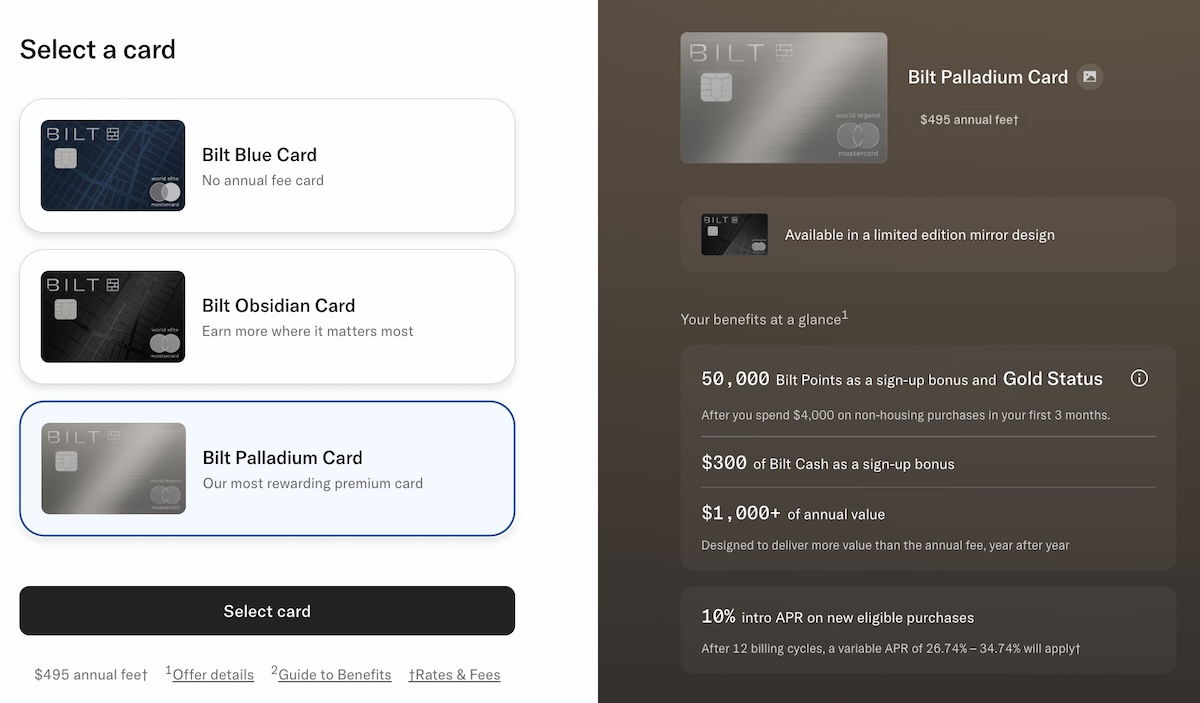

Link: Apply for a Bilt credit card, with three options to choose from

Bilt is the platform that is most known for offering rewards for housing payments. We’ve seen major changes to the company’s rewards concept, and Bilt now has three Mastercard credit cards serviced by Cardless, which are potentially worth considering. This includes the no annual fee Bilt Blue Card, $95 annual fee Bilt Obsidian Card, and $495 Bilt Palladium Card.

I’ve written a guide to Bilt credit cards, and in general, I’ve argued that the highest annual fee Bilt Palladium Card is most worthwhile, followed by the mid-range Bilt Obsidian Card, followed by the no annual fee Bilt Blue Card.

In this post, I’d like to take an in-depth look at the Bilt Palladium Card. What are the card’s perks, and is it worth the steep annual fee?

In this post:

Why I think the Bilt Palladium Card is worth it

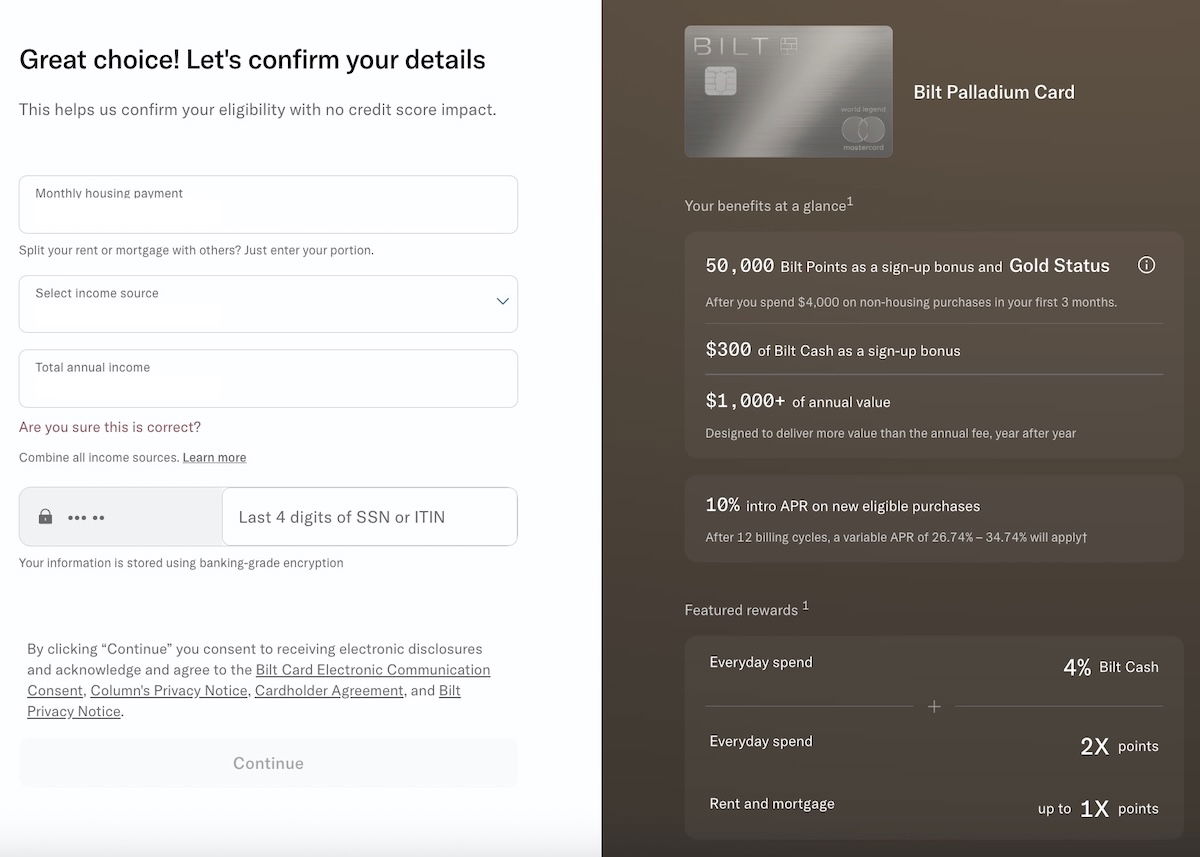

The Bilt Palladium Card is the most premium card in Bilt’s credit card portfolio, and here are the basics of the card’s value proposition:

- The Bilt Palladium Card has a $495 annual fee, with a $95 annual fee per authorized user

- The Bilt Palladium Card has a welcome bonus of 50,000 bonus points and Bilt Gold status after spending $4,000 within three first three months (on non-housing purchases), plus $300 Bilt Cash upon approval

- The Bilt Palladium Card offers 2x points on all eligible purchases, and Bilt Rewards points are super useful

- The Bilt Palladium Card offers 4% back on spending in the form of Bilt Cash, which can be redeemed for all kinds of things, including the ability to earn 1x points on housing payments, points accelerators on spending, and more

- The Bilt Palladium Card offers $200 in Bilt Cash annually as an anniversary bonus of sorts

- The Bilt Palladium Card offers up to $400 in Bilt travel portal hotel credits every calendar year; this comes in the form of a $200 semi-annual credit, valid for a two-night minimum stay

- The Bilt Palladium Card offers a Priority Pass membership, with up to two guests allowed (authorized users also receive a membership)

I think the Bilt Palladium Card is the product that’s most worth considering. Why? For one, the card has a welcome bonus of 50,000 bonus points and Bilt Gold status after spending $4,000 within three first three months (on non-housing purchases), plus $300 Bilt Cash upon approval.

Other than this, we’ve never seen a Bilt card have a formal welcome bonus before, and that’s absolutely worth taking advantage of, as the other two cards don’t offer any points with the bonus. At a minimum, the card is worth giving a try for a year.

Beyond that, what intrigues me about the card is simple — it offers 2x Bilt points on everyday spending, which is pretty incredible. Bilt Rewards points are valuable, as they can be transfered to Alaska Atmos Rewards, World of Hyatt, and a variety of other programs.

While we’ve seen some transferable points cards offer 2x points, I think being able to earn Bilt points at that rate is incredible, and probably beats the other options.

The icing on the cake is that is that you’re earning 4% back in the form of Bilt Cash on all your spending, and as I see it, there are two redemption options that are most enticing:

- $3 in Bilt Cash is worth 100 Bilt points on your total rent or mortgage payments, at the rate of 1x points; put another way, you’d get $4,000 worth of housing payments (4,000 points) with $3,000 in spending

- $200 in Bilt Cash (which you’d unlock after $5,000 in spending) can be redeemed for one extra point per dollar on $5,000 worth of non-housing spending, meaning you’d earn 3x points per dollar spent on everyday spending; you can unlock this perk up to five times per year, for up to $25,000 worth of spending

The numbers here are pretty lucrative. Just to give an example with straightforward math, let’s say you spend $100,000 per year on the card:

- You’d earn 200,000 Bilt points, at the rate of 2x points per dollar spent

- You’d earn at least $4,000 in Bilt Cash, at the rate of 4% back (and that doesn’t factor in the annual Bilt Cash bonus)

- You could redeem $1,000 in Bilt Cash to earn 25,000 bonus points on spending (where you’d earn 3x points), and the other $3,000 in Bilt Cash could unlock earning 1x points on $100K in housing payments annually

- You’d also earn Bilt Platinum status, which gives you extra benefits, like some partner status perks, access to better Rent Day offers, etc.

It’s hard to argue with that return on spending, as that’s pretty spectacular.

Why the lower annual fee Bilt cards aren’t as good

Above I made the case for the Bilt Palladium Card, but what actually makes the card more compelling than the lower annual fee versions?

Well, I think there’s an argument to be made for getting the $95 annual fee Bilt Obsidian Card, though there are a couple of main considerations:

- The Bilt Palladium Card has a bonus of 50,000 points upon completing minimum spending, so that’s a lot to forgo by applying for the Bilt Obsidian Card

- The two cards have very different rewards structures, as the Bilt Palladium Card offers 2x points on all eligible spending, while the Bilt Obsidian Card offers 3x points on your choice of dining or groceries (dining is uncapped, groceries is capped at $25K of spending per year), 2x points on travel, and 1x points on all other purchases

I’d say it’s hard to turn down the welcome offer on the Bilt Palladium Card, but beyond that, the decision comes down to how much you spend in categories that would earn bonus points on the Bilt Obsidian Card.

However, what’s the case for instead applying for the no annual fee Bilt Blue Card? The card is pretty basic — it gives you access to the Bilt ecosystem, but it only earns 1x points per dollar spent. So the simple argument in favor of the card is if you absolutely don’t want to pay an annual fee, but can still get outsized value by redeeming Bilt Cash to earn points on housing payments.

But if you’re a relatively big spender, I think the math on the Bilt Palladium Card really works out quite nicely.

My hesitations with the value of the Bilt Palladium Card

While there’s a lot to like about the Bilt Palladium Card, I think there are some important points to make, about things that concern me, or that I maybe don’t love about the program.

For one, I’m frustrated by Bilt specifically excluding certain spending categories from being eligible to earn points. For example, Bilt states that it won’t award points for tax payments put on credit cards. Virtually every card from a major issuer doesn’t have such a policy.

That’s a major “spending” category for me, and a way I earn lots of points with other cards. That’s of course Bilt’s prerogative, but it has major implications for how I value the card. So that’s not a category where I can earn rewards with Bilt, and it means I need to keep around another great card for everyday spending. It also makes me wonder how much I really spend in categories that aren’t bonused on other cards.

Second, I need to figure out how much of the $495 annual fee I can actually recoup. The card does offer a Priority Pass membership, plus up to $400 in Bilt portal hotel credits per year (a $200 credit semi-annually, each requiring a minimum two-night stay).

The restrictions on that hotel credit are potentially a little annoying, and I’m not sure I’ll be maximizing the value of that. So how much will I really be paying “out of pocket” to hold onto this card?

Third, there’s just the general question of how sustainable all of this is, and if it will all stick around. The economics here are better for Bilt than they were under the old system, but still, I feel like we’re going to see some more cuts. For example, will Bilt points continue to be as valuable as they are now, as I can’t imagine the current redemption rates are sustainable for Bilt?

I’m putting this card in the category of absolutely being worth trying, but it remains to be seen if it’s the best option in the long run, based on how things play out. I’m also curious to see how much I actually spend on the card in non-bonused categories, since that will determine how much of the annual fee I’m really recouping. I need to be able to spend a lot — and earn a lot of points — for the $495 annual fee to make sense.

I think one of Bilt’s big challenges is that it tends to have a pretty savvy customer base. After all, these are people who care enough to pick up a card specifically to earn housing rewards. Those people are also more likely to take advantage of benefits, maximize their points redemptions, etc.

It’s a much less profitable customer base than with something like Amex, where you have people who don’t really care about the points, but they just want the “status” of spending on an Amex card.

My experience “applying” for the Bilt Palladium Card

Bilt recently transitioned from Wells Fargo to Cardless, and existing cardmembers had the opportunity for a seamless transition, so that’s how I acquired this card.

If you’re an existing cardmember, there’s no hard pull when you apply for the new card, and instead, there’s just a soft pull. So unless something absolutely drastic changed since your previous application, you’re supposed to also be approved for the new card (however, there are a concerning number of reports of non-approvals). If you get approved, your credit card number even stays the same as you transition to the new product.

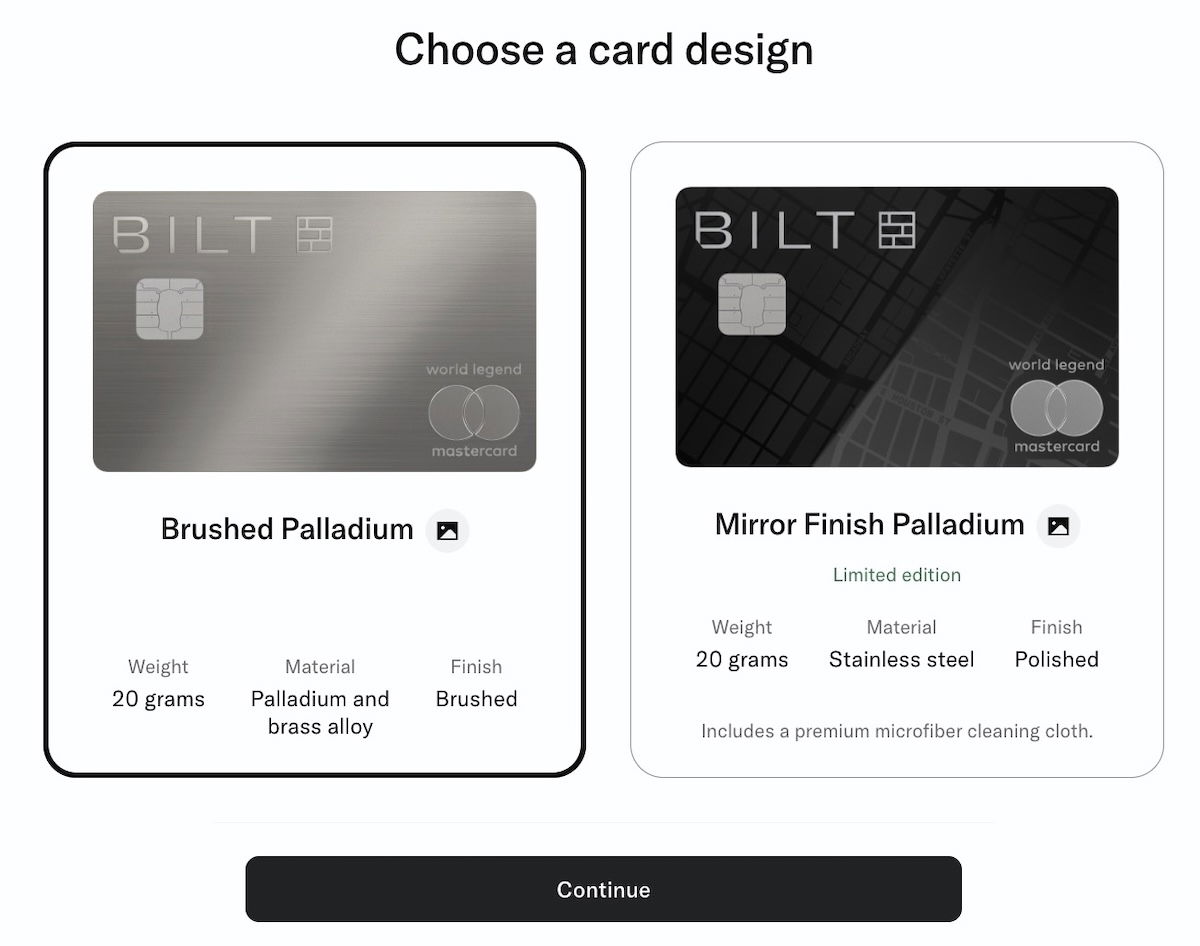

With that in mind, let me share my experience. After going to Bilt’s new credit card page, I logged into my account and clicked the “Apply now” button, and I could choose which card I wanted. I selected the Bilt Palladium Card.

I could then choose my card design, between brushed palladium or mirror finish palladium.

I was then asked to confirm the information I had provided to Wells Fargo in the past, including my monthly housing payment, income, etc.

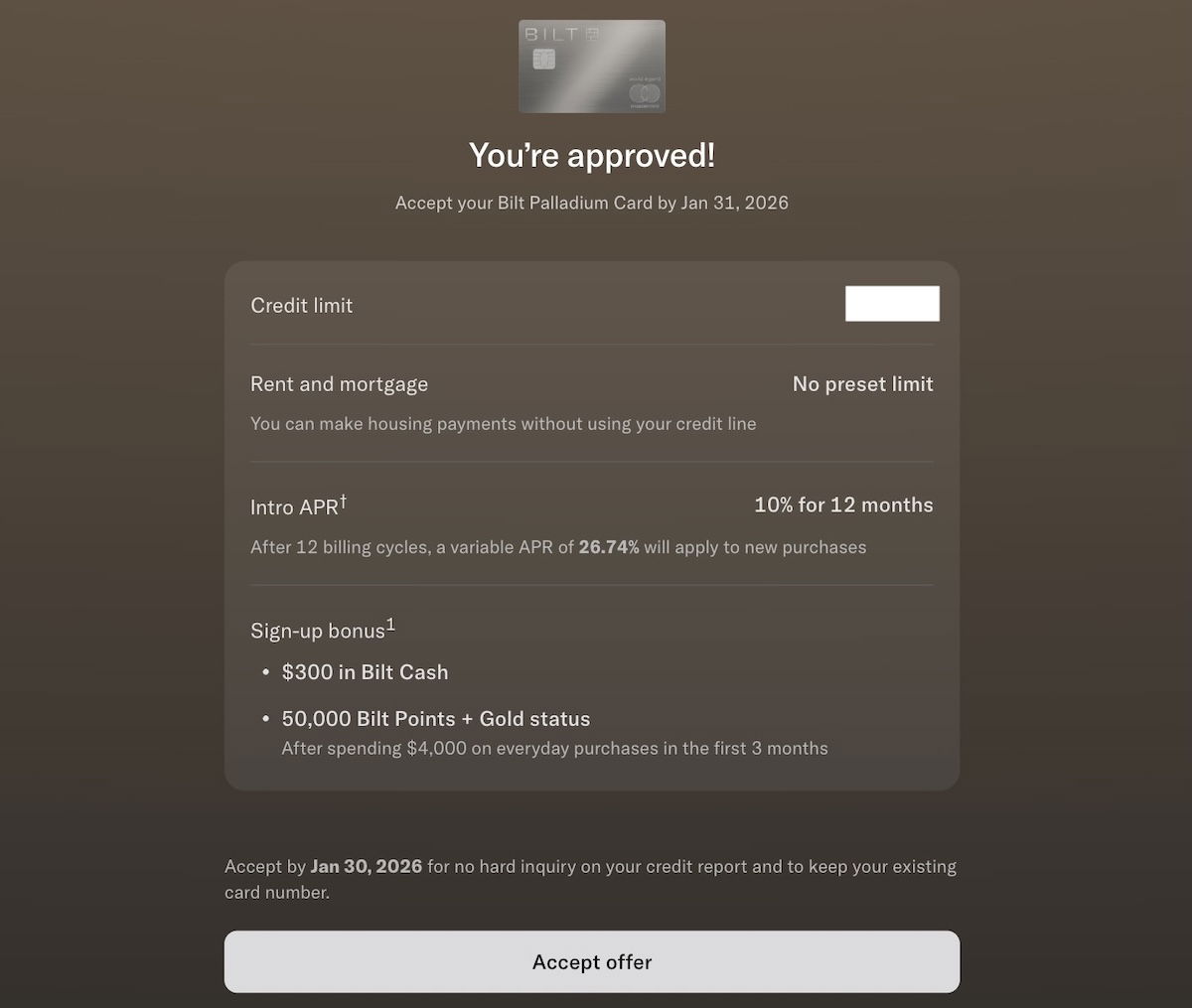

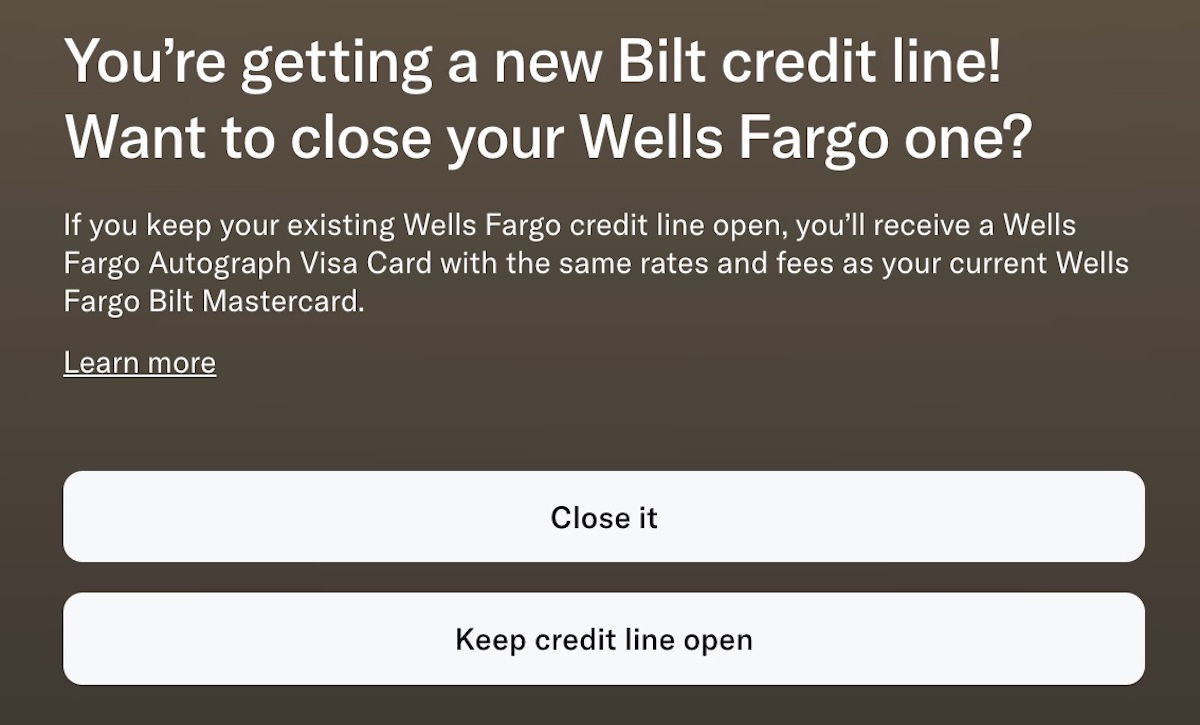

I then submitted that information and found that I was approved, with a big credit line (though it was still about 30% smaller than my Wells Fargo credit line, which was oddly large). Keep in mind that with the transition to Cardless, your rent or mortgage payment no longer counts toward your credit line (since it’s paid by ACH rather than being charged to your card), so that gives a little more flexibility. I was asked if I wanted to accept the offer.

After accepting the offer, I was asked if I wanted to keep my Wells Fargo credit line open, which I didn’t want, so I clicked “Close it.” In theory there’s value to keeping cards open in order to maximize your available credit, which can be good for your credit score. However, I have so many credit cards and so much available credit that I’m no longer trying to keep them open unnecessarily.

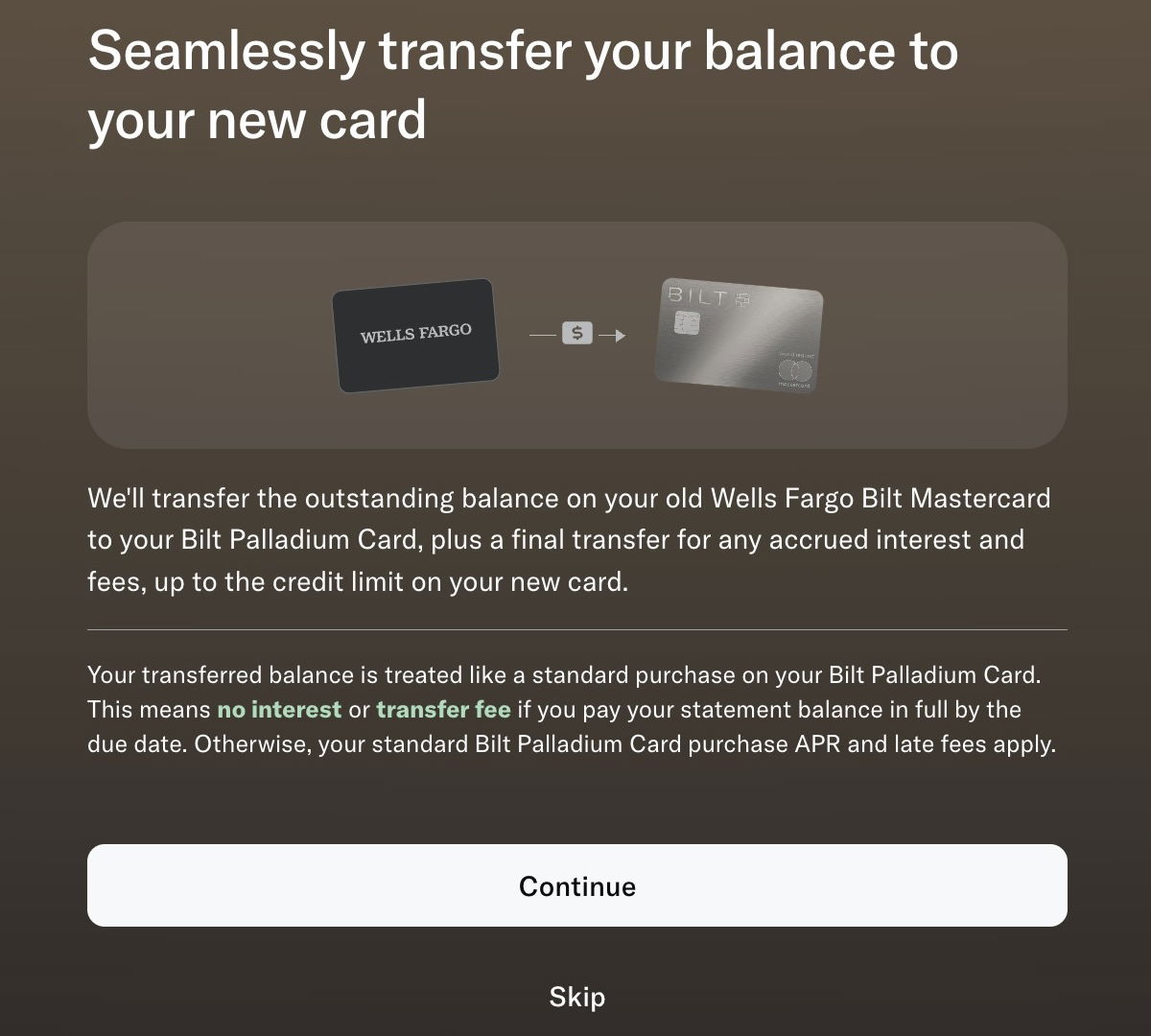

Lastly, I was asked if I wanted to transfer my balance to my new card, and I said that I did.

All-in-all, I found it to be a straightforward process. For what it’s worth, I found that the bonus points and Gold status posted to my account almost immediately after completing the minimum spending (compared to being at the end of a statement period, or something).

Bottom line

Bilt now has three credit cards at different price points, and I’d argue that the $495 annual fee Bilt Palladium Card is the obvious choice, assuming you spend a decent amount on your credit card, and on rent or mortgages.

It’s the only card with a substantial welcome bonus, and as I view it, that bonus more than covers the card’s annual fee for the first year. The biggest selling point of the card is that it earns 2x points on all spending, which I’d argue makes it one of the best cards out there for everyday spending, given the value of Bilt points.

Then your spending earns you Bilt Cash, which you can redeem for a combination of housing payments and to earn even more bonus points, so that you can earn 3x points on up to $25,000 of spending annually.

However, I also have concerns. I don’t like how tax payments aren’t eligible for earning points, and I’m not sure how easily I’ll be able to recoup the annual fee, given the lack of meaningful benefits outside of Bilt Cash and the Bilt hotel credit.

For now I’m viewing this as a card that I’m giving a try for a year, and then I’ll decide on my long term strategy based on how things play out. For the first few weeks my experience has been good, but we’ll see how this all evolves.

How are you thinking about which Bilt card makes the most sense, and which did you decide on, if any?

Agree with JL below. The new 2.0 is a nightmare. My rent payments won’t go through. No one will respond to emails or chats from Bilt. Their platform is melting down and there is no support. Who cares about anything else if I’m 7 days past due paying my landlord because Bilt can’t get their act together!

Ben, I have seen quite a number of posts, both from you and others, since launch about the value proposition of Bilt and why it's a ecosystem to be a part of. And you highlight your experience with the application process, with the seemingly obvious goal of getting more readers to sign up. However, I've seen relatively little reflection from you or feedback from your followers about actual experience using the card. Maybe I just...

Ben, I have seen quite a number of posts, both from you and others, since launch about the value proposition of Bilt and why it's a ecosystem to be a part of. And you highlight your experience with the application process, with the seemingly obvious goal of getting more readers to sign up. However, I've seen relatively little reflection from you or feedback from your followers about actual experience using the card. Maybe I just missed those posts, or maybe you've been lucky enough to not have hit any snags. But my experience has been nothing short of a nightmare so far. Failed mortgage payments that Bilt can't account for, funds withdrawn from my checking account that still haven't been returned despite the mortgage servicer never receiving the funds (twice!), not being able to get a hold of chat support after being on "hold" for 8 hours each day multiple days, radio silence of support via email, the list goes on. I've seen multiple reports on blogs elsewhere of similar issues.

I agree with what has been written so far about the value. I expect these issues are just part of the growing pains and will be fixed in the coming months. I just think you're doing a disservice to your readers by not mentioning that perhaps it isn't the right time, at this very moment, to become part of the "beta testers" that we clearly are due to the poorly executed Bilt 2.0 launch.

Ben - now that you've got the Palladium card, have you sock-drawer'd your Venture X and Double Cash cards? If not, what percentage of your non-bonus spend does each one get?

Here's another criticism. For being a Mastercard Legend -- the tip-top category of card -- secondary auto coverage, seriously?

Hey Ben. I assume you have a venture x as well. How are you integrating that card along with the palladium?

he's mentioned this briefly but i'll answer in case he doesnt see: theres basically no reason to spend on Cap 1 cards if you have palladium. Bilt has way more/better partners and better ratios. Only few you're missing available via Cap One but not Bilt: EVA (4:3 ratio, so better via Citi anyway), Singapore (available via everyone else), and JetBlue (5:3 ratio lol).

So TLDR mine (and I assume Bens) Venture is sock drawered...

he's mentioned this briefly but i'll answer in case he doesnt see: theres basically no reason to spend on Cap 1 cards if you have palladium. Bilt has way more/better partners and better ratios. Only few you're missing available via Cap One but not Bilt: EVA (4:3 ratio, so better via Citi anyway), Singapore (available via everyone else), and JetBlue (5:3 ratio lol).

So TLDR mine (and I assume Bens) Venture is sock drawered for now. I still earn referral points as well as Cap 1 offers though

I don’t have rent or mortgage, so I can’t see how this card pans out for me. Maybe illustrate with $2k/month ($

($24k /year).?

I have two Hilton Aspire cards and two Hilton Surpass cards. If I’m not working on a SUB, I put the non bonuses dpenf on that card. If I hit $15k, I get a third (and perhaps fourth) FNC to go with my Aspire cards, good for any Hilton. Also...

I don’t have rent or mortgage, so I can’t see how this card pans out for me. Maybe illustrate with $2k/month ($

($24k /year).?

I have two Hilton Aspire cards and two Hilton Surpass cards. If I’m not working on a SUB, I put the non bonuses dpenf on that card. If I hit $15k, I get a third (and perhaps fourth) FNC to go with my Aspire cards, good for any Hilton. Also $15k on my Hyatt card for the cat1-4 free night.

Seems like I get a better return on that than the Palladium Card (assuming I hit $15k or $30k). 50k points for $495 isn’t all that great. Points won’t come before Hyatt devaluation most likely. Other than Hyatt and United, my Amex points are plenty for the other Bilt cards.

Use your Bilt Cash for point earning accelerators. You'll earn 3X on your entire annual spending. Exclude consideration of any other credits. Apply that concept to your specific circumstances. Best of luck.

May try out the Palladium card for the first year considering the welcome bonus, then product change to Bilt Blue if the benefits don’t pan out.

This is the way. February 2027 gonna be interesting, as everyone downgrades, unless there is some compelling retention offer. Let's be clear, without the SUB, another year of $495 is insane. No semi-annual $200 BILT travel credit for prepaid 2-night stays is gonna make this a keeper...

In spite of earning an interchange fee on tax payments . . . and thus covering point earning . . . Bilt management seems terrified of those few individuals who might game the system. But, there are those of us with legitimate high income who make legitimate large tax payments who are being alienated. It's unfortunate. Bilt is missing out on a substantial amount of charge flow from non-gamers.

PS - It is the same shortsightedness as Bilt's initial decision (which it reversed) to exclude PayPal and other payment platforms. I buy from a number of businesses (including non-US businesses) that only accept payment via PayPal or wire transfer. Again, spoiling it for the many for fear of the few.

Thank goodness BILT reversed the PayPal decision, because you're absolutely right, ample legitimate businesses and charges using that platform.

Yeah, they really should reverse excluding tax payments. Yes, they earn money off those payments, but to not award points is cheap. Like, many of us have 1040-ES each quarter.

Are tax payments still excluded if we make the payments through PayPal?