Delta Air Lines has today reported its 2025 financial results, and 2026 forecast, and there’s nothing too surprising. While the airline expected to achieve record profits in 2025, that didn’t turn out to be the case, due to all the economic uncertainty.

Delta is now expecting to earn record profits in 2026 — I understand Delta has to provide guidance, but it just seems that we’re continuing to see a lot of uncertainty, so who knows how things will play out. Anyway, in this post I’d like to focus on the detail of Delta’s 2025 results (particularly in Q4) that I found most interesting.

In this post:

Delta premium revenue jumps 9%, economy revenue drops 7%

Coming out of the pandemic, “premium” travel has been all the rage, and that’s a trend that’s continuing, seemingly with no end in sight. Just listen to any airline earnings call, and you’ll hear premium, premium, premium, premium, premium. Airlines are doing well in their forward cabins, while they’re struggling more in economy.

There’s no better reflection of this than Delta’s latest passenger revenue numbers. Before I share those details, let me just define a couple of things:

- Main cabin revenue includes standard economy bookings, including basic economy

- Premium product revenue includes first class, business class, premium economy, and extra legroom economy

With that in mind, if you compare Delta’s Q4 2025 results to Q4 2024 results:

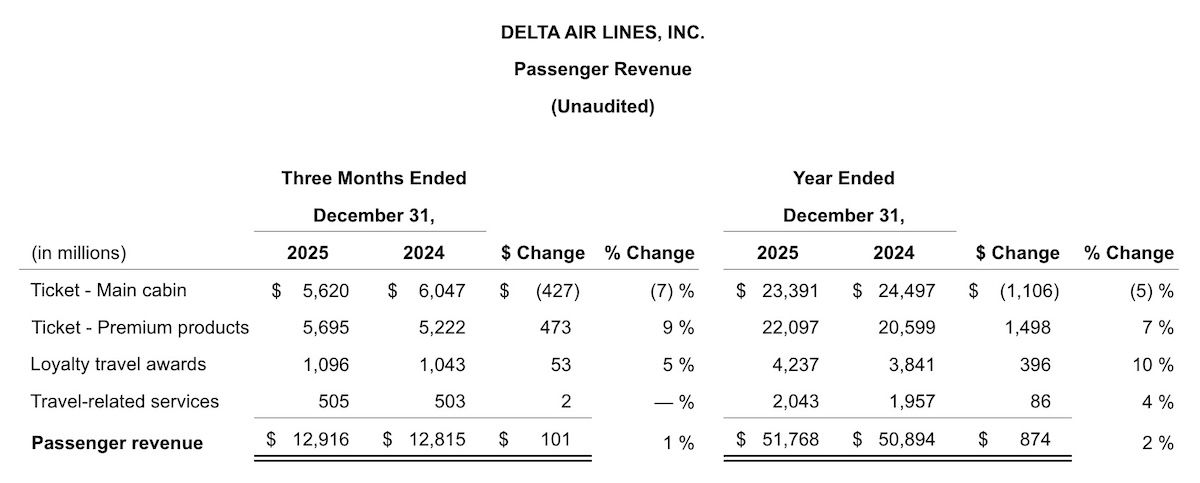

- Main cabin revenue decreased by 7%, from $6.05 billion to $5.62 billion

- Premium cabin revenue increased by 9%, from $5.22 billion to $5.70 billion

As you can see, that means premium cabin revenue exceeded main cabin revenue, which is the first time in the company’s history that we’ve seen that. Looking at the full year, and comparing 2025 to 2024:

- Main cabin revenue decreased by 5%, from $24.50 billion to $23.39 billion

- Premium cabin revenue increased by 7%, from $20.60 billion to $22.10 billion

So for the full year, main cabin revenue exceeded premium revenue. However, it seems there’s no end in sight to this shift, and I wouldn’t be surprised if 2026 is the first full year where premium cabin revenue exceeds main cabin revenue.

Will aircraft LOPAs change more radically over time?

People disagree as to whether the move toward premium travel is a temporary fad, or a permanent shift. If you ask airline executives, they believe it’s the latter.

I suspect they’re largely correct, given the extent to which airline profits in the United States have also increasingly centered around loyalty programs, and premium cabins are a big part of that.

However, I don’t think it’s quite as much of a given as they assume, because I think it largely reflects the increasing dual economy we see in the United States — you have a lot of people struggling with the increased cost of living, while you have others getting rich off the strong stock market, which would make you believe that everyone is thriving. If we see a big drop in the stock market, you can say goodbye to the level of premium demand we’re seeing.

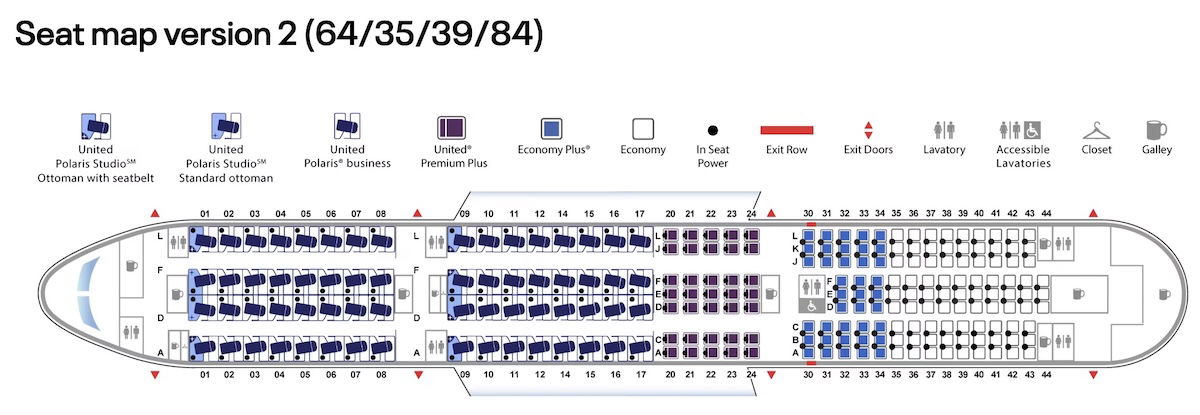

What I find most interesting, though, is how LOPAs are evolving (“LOPA” stands for “layout of passenger accommodations” — essentially how planes are configured). When you look at wide body, long haul aircraft, airlines are clearly going all-in on premium. I mean, just look at the seat map for United’s upcoming Boeing 787-9s (American and Delta are also making their wide body planes more premium, but not quite to this extent).

The planes will feature a total of 222 seats, and 138 of those seats will be premium. Around 80% of the cabin is dedicated to premium seating, so you better hope that premium revenue exceeds economy revenue!

But what I find interesting is that you don’t see nearly this level of transformation on domestic aircraft. The percentage of first class seats remains largely unchanged compared to 20 years ago, even as we’ve gone from seeing 10% of first class seats sold, to seeing 90% of first class seats sold.

For example, just look at Delta’s old Boeing 757-200s, compared to Delta’s new Airbus A321neos:

- Airbus A321neos have 194 seats, including 20 first class seats, 60 extra legroom economy seats, and 114 economy seats

- Boeing 757-200s have 199 seats, including 20 first class seats, 29 extra legroom economy seats, and 150 economy seats

So I guess if you want to look at it differently, you could largely attribute the increase in premium revenue on narrow body planes to more people simply buying up to extra legroom economy seating, given how many more of those seats there are, plus the new ways Delta has monetized those seats.

However, it still seems like US airlines don’t want to exceed that 20-seat first class cabin limit that largely exists on new generation aircraft. Several months back, Delta executives hinted that they were considering making first class cabins bigger, but nothing has come of that yet. I’ve written in the past about how I think US carriers should consider greatly expanding the size of their first class cabins, and I’m curious if that does eventually happen.

Bottom line

In Q4 2025, Delta reached an interesting milestone, where premium cabin revenue exceeded economy revenue for the first time. The trend is clear — premium travel demand keeps increasing, while economy travel demand (or at least the revenue associated with it) keeps decreasing.

Now, this might not be quite as radical as it sounds, as I imagine a large part of this is passengers increasingly paying for extra legroom economy seating, as those cabins continue to get bigger. However, I can’t help but think that we should also eventually see first class cabins get more than 20 seats.

What do you make of Delta’s premium cabin revenue milestone? Do you think we’ll eventually see bigger first class cabins?

I thought airlines have always said premium is more profitable than economy. Does this revenue exclude award redemptions?

Something to consider are the Baby Boomers & Gen X are retired or have accumulated wealth or moving high up the food chain. If not flying in Business Class, they are occupying PE and Xtra Leg Room. This is a large chuck of the flying population on 8+ hour TALT or TPAC flights. Next time, just look for the bald spots or grey hair or blue hairs; they are the ones sitting up front.

absolutely true.

anyone with stock market wealth has seen their portfolio go up 15-20% in the past year. Americans over 59.5 years can access that wealth even before Social Security kicks in.

and while Presidents have done stupid economic things that sink the stock market, killing off that kind of growth in equities is a guaranteed way to lose elections.

the outlook for US airlines in their international operations is bright for years to come.

So when someone pays $30 extra for an exit row seats they're a 'premium' customer? Interesting definition.

It's almost as if when only rich people can afford to buy things, the economy doesn't work.

You do realize that back in the 1950s-1970s most people could not afford to fly or fly only once every few years. Yet no one was saying the economy doesn't work because only rich people could fly.

Good, maybe we'll hear less b!tch!n'. My contention has been that Y+ (Comfort+ on DL) is the "default" coach seat. That is, it offers a seat with similar specs to "golden age" coach. You sit 3-3 on a narrowbody and get 34" of pitch (738). Fly their 321neo you get 33", but a wider than "golden age" seat. All in, with airfare and baggage/seat-assignment fees, that Y+ seat is a great deal adjusted for inflation....

Good, maybe we'll hear less b!tch!n'. My contention has been that Y+ (Comfort+ on DL) is the "default" coach seat. That is, it offers a seat with similar specs to "golden age" coach. You sit 3-3 on a narrowbody and get 34" of pitch (738). Fly their 321neo you get 33", but a wider than "golden age" seat. All in, with airfare and baggage/seat-assignment fees, that Y+ seat is a great deal adjusted for inflation. If you buy Y or Y-, you've decided to get less to save money. The difference in the "golden age" in coach hard product was that it was 1) more expensive, 2) sometimes wasn't as wide (A220 and A320 series are wider seats), and 3) didn't offer a reduced hard product at a discount.

What I think we may see is "premium regionals" - when major carriers like DL, AA spin-off the likes of JSX to provide more premium capacity where it's in demand. Routes could be NYC - Florida/TX for example. Planes could be E175s configured with J and Y+ only, having like 40-50 people instead of usual 75-80.

Then, the airlines won't need to have too big premium cabins on their A321s, allowing those to be...

What I think we may see is "premium regionals" - when major carriers like DL, AA spin-off the likes of JSX to provide more premium capacity where it's in demand. Routes could be NYC - Florida/TX for example. Planes could be E175s configured with J and Y+ only, having like 40-50 people instead of usual 75-80.

Then, the airlines won't need to have too big premium cabins on their A321s, allowing those to be moved around premium and leisure routes. For frequent premium travelers, this will be additional frequencies and fast boarding/deplaning.

Ben clearly woke up trying to bait Tim today. Diabolical :P

Ben covered the story regarding DL's rumored order for 787s and is good enough to follow up on it; he covers most major fleet orders so this should be no different.

The rest is related to DL's earnings which came out; hopefully, he will cover at least the rest of the big 4 as they report over the next couple weeks.

and by DL going first, there are always comparisons of how each subsequent...

Ben covered the story regarding DL's rumored order for 787s and is good enough to follow up on it; he covers most major fleet orders so this should be no different.

The rest is related to DL's earnings which came out; hopefully, he will cover at least the rest of the big 4 as they report over the next couple weeks.

and by DL going first, there are always comparisons of how each subsequent carrier does to DL.

I am going out on a not very long limb and state that no other US carrier will come close to DL's financial report

Looks like DL needs more main cabin extra seating. AA needs as well - when I look at AA seat maps several months out - AA's MCE can be nearly full and the rest of coach is empty. In some markets in CA - like PSP and SNA - MCE seats fill up first. It's like, most people traveling these days have Status and book MCE, if not First Class - which can also fill up weeks before.

"main cabin extra" ... tell me you fly American Airlines without telling me you fly American Airlines.

Ackchyually... it's called... "Delta Comfort" ...formerly Comfort+, also known as Delta Comfort Basic, Delta Comfort Classic, and Delta Comfort Extra, not to be confused with Delta Main Basic, Delta Main Classic, or Delta Main Extra, also not to be confused with Delta Premium Select (which likely also has Classic and Extra)... /s

If the premium cabin revenue only grew 9% while they've increased the cash price for Delta One almost 100% across the board, this seems like a trend that won't be able to continue. Full fare D1 to LAX from JFK used to cost around 3K, it's now in the mid 6's to almost 7K and premium select is now at the former D1 rate. There are only so many people that will be brand loyal when the cash price for American is still around 3K.

Delta carries the highest percentage of corporate traffic of any US airline; the full price is used to calculate corporate discounts.

And does anyone know the % of corporate pax in the domestic premium cabins for each airline? That will determine what predominantly drives full fare cash rates.

Timo, one understands that passenger demographics are not universally shared, however, a figure of between 30-50 is often quoted for company passengers in the U.S.

I am sure some of this is the upsell over elites, but frankly, they are pricing themselves out of the market in economy main cabin flying. They are often 150$ plus more expensive for the same flights where I am, even in basic, and they simply aren't that much better these days. Far too many delays and cancelations. The biggest joke as a 'premium' flier is I looked to book tickets to Columbia in 1st...

I am sure some of this is the upsell over elites, but frankly, they are pricing themselves out of the market in economy main cabin flying. They are often 150$ plus more expensive for the same flights where I am, even in basic, and they simply aren't that much better these days. Far too many delays and cancelations. The biggest joke as a 'premium' flier is I looked to book tickets to Columbia in 1st and could NOT buy them with Delta. It was 'Premium Select' only which was a comfort plus seat on the regional and a 1st class seat on the 5 hour connection. And it cost MORE than either AA or United in actual 1st class seats ll the way through. Ecuador has become this awful hodge podge of Latam flights on ancient planes with their fake comfort plus which is just economy at the front of the economy section. The last few times I went at least it was on Delta metal.

A small drop in OPM flying due to will be a disaster for US airlines

One thing I'd add as an argument why premium revenue is ongoing reduction in seat pitch in economy. We've seen a slow erosion of seat pitch from 32" to 31" to now 30". This allows airlines to lower their price in economy while charging more for plus, PE, J, etc. At 6'3", I can handle 30" seat pitch for a couple hours, but beyond that? I'm buying extra legroom or better.

When I'd fly...

One thing I'd add as an argument why premium revenue is ongoing reduction in seat pitch in economy. We've seen a slow erosion of seat pitch from 32" to 31" to now 30". This allows airlines to lower their price in economy while charging more for plus, PE, J, etc. At 6'3", I can handle 30" seat pitch for a couple hours, but beyond that? I'm buying extra legroom or better.

When I'd fly B6 with their 32-33" seat pitch, the incentive to buy "even more space" was less (though I'd usually buy it anyway if the upgrade was fair). With them going to 30" in the future, it will be a near necessity for any flights over 2 hours. Hence, they'll be able to charge more for EMS.

And never mind for international flights on 787 and 777 where the seats are 9 and 10 across accordingly with 17" width vs 18" wide on the A330, A350 and A380 (as well as the 767). With the former, I'd rather find a discounted premium points redemption or pay the upcharge for PE or better.

i'm looking forward to when business class bookings collapse and they have to sell them at record prices to fill em up

bizarre.

a collapse of premium class demand means the US economy will be in serious trouble.

Airlines are always reflective of larger macroeconomic issues.

and, as Ben notes, AA and UA will both have widebodies with more business class seats than DL but DL seems to be willing to put larger premium select cabins.

And I'll be right there to gobble up one or two. As long as they are for places I intended to visit. I can't wait...

while including extra legroom economy in premium revenue might be a stretch, the difference in fare between regular economy is not that high.

The chances are that the two amounts are now equal or pretty close to it if you count Comfort Plus in regular economy.

The point is that DL says people are willing to buy up from the basic coach experience and there is no doubt that AA and UA are seeing the...

while including extra legroom economy in premium revenue might be a stretch, the difference in fare between regular economy is not that high.

The chances are that the two amounts are now equal or pretty close to it if you count Comfort Plus in regular economy.

The point is that DL says people are willing to buy up from the basic coach experience and there is no doubt that AA and UA are seeing the same thing.

and DL's MAX 10s will have more Comfort + seats than the 737-900ERs so the extra length is largely going to more premium seats.

internationally, the difference between DL and both AA and UA is that it has been much harder to get an upgrade into Delta One than in AA or UA's business or first (AA int'l) products. Both are tightening up upgrades because they see the demand that exists and DL has captured for years.

THAT is what is driving the increase in premium revenue along w/ the addition of premium economy.

and any president that sinks the stock market will be ousted. It is perhaps a stronger 3rd rail of the US economy than Social Security

Tim is high again.

GUC is the easiest to get upgraded followed by PP and SWU is almost useless.

That being said, GUC is the least useful of them all. Especially if you need to buy an overpriced PE ticket.

"people are willing to buy up from the basic coach"

But the point is not people buying up.

They are buying "out" because airlines blackmail them with inhumane basic restrictions, buying out of...

Tim is high again.

GUC is the easiest to get upgraded followed by PP and SWU is almost useless.

That being said, GUC is the least useful of them all. Especially if you need to buy an overpriced PE ticket.

"people are willing to buy up from the basic coach"

But the point is not people buying up.

They are buying "out" because airlines blackmail them with inhumane basic restrictions, buying out of something that used to be free is now what you call "buy up". You're basically paying more for less.

first, DL does not do gate upgrades to int'l business while AA and UA have but are reducing it.

second, all airlines have reduced economy seating. and, yes, people are buying up regardless of their reason.

there are a few airlines that have 32 inch or greater in economy but not a whole lot.

"first, DL does not do gate upgrades to int'l business while AA and UA have but are reducing it."

AA UA doesn't either fluffy Tim.

Eskimo, are you for-real trashing GUCs? No way, dude. Horrible take. GUCs rock (even if you have to pay for PE, you're still saving thousands and thousands of dollars on D1 for long-haul). RUCs are alright (if you can redeem on 763 for transcon JFK-SFO for Main to D1). And, unlike AA's SWU and UA's PlusPoints, Delta's GUCs and RUCs actually confirm at booking, much of the time. Nope. I'm 100% Delta on this. Tim, let Eskimo have it; he's wrong.

Tim, control your alter ego.

Your stupidity and lack of reading comprehension is crossing to 1990.

"GUCs and RUCs actually confirm at booking, much of the time" = "GUC is the easiest to get upgraded"

"and any president that sinks the stock market will be ousted. It is perhaps a stronger 3rd rail of the US economy than Social Security"

That's aging pretty well, isn't it?! lol

my portfolio is up healthy double digits over the past year - and it is in line with the markets.

and, yes, AA and UA have done alot of upgrades within the last 24 hours whether they are physically at the gate but essentially they are giving away unsold seats.

when you know that you have a good chance of getting an upgrade, there is less chance of buying it.

Tim, what are you fluffing?

Like DL, AA UA doesn't give away unsold intl seats upgrades.

Yeah this is just a lie. UA does not do this.

So then Delta should be bold and try a bigger Comfort+ section and eliminate regular economy. American Airlines did that with MRTC More Room Throughout Coach but abandoned that.

A few observations:

1. The days of thinking the leisure traveler only cares about the cheapest fare available are coming to an end. Some with the income want a better experience

2. The days of free upgrades to those generally flying on OPP are becoming much more limited. Flying week and week out will never translate into abundant upgrades. At least domestically most companies/clients only pay for coach travel. And that's where you will...

A few observations:

1. The days of thinking the leisure traveler only cares about the cheapest fare available are coming to an end. Some with the income want a better experience

2. The days of free upgrades to those generally flying on OPP are becoming much more limited. Flying week and week out will never translate into abundant upgrades. At least domestically most companies/clients only pay for coach travel. And that's where you will be sitting unless you pay out of pocket.

3. If the demand exceeds of supply of premium seats you will see remodels towards more premium. Paid premium, not upgrades.

The new reality is that OPM flyers are forced to pay out of pocket to go to work (absurdly). There is no glory in domestic OPM flying

A couple of thoughts:

In terms of "permanency" of the move towards premium, I suspect it also all depends on the strength of ULCCs in the future. The bigger the ULCCs, the more competition for the economy class traveler.

In terms of making the first-class / extra legroom section bigger on aircraft, I see that as a very complicated, time-consuming process. Depending on the flight schedule of an aircraft, a bigger first-class / extra legroom...

A couple of thoughts:

In terms of "permanency" of the move towards premium, I suspect it also all depends on the strength of ULCCs in the future. The bigger the ULCCs, the more competition for the economy class traveler.

In terms of making the first-class / extra legroom section bigger on aircraft, I see that as a very complicated, time-consuming process. Depending on the flight schedule of an aircraft, a bigger first-class / extra legroom may work on one segment, but not the other. I suspect the bigger first-class / extra legroom will be limited to certain aircraft that can be scheduled to certain markets.

Wondering if first class cabins on narrowbody jets remains the same size due to the amount of galley space they have while galley space is more flexible on widebodies. With upgrades hardly ever clearing I know the seats are selling out on a lot of the domestic flights I take

Came here to say this. Doubt there's much space in a narrowbody forward galley left over after catering 20 seats for, e.g., a California to Midwest route that needs a full meal service, two drink services, three trash sweeps...24/28/32 seats might make it tough to provision a premium soft product.

You have to remember cargo as well. More premium passengers means less checked luggage, more room for cargo. I know this is the case for a few transatlantic routes.

Anyway I think this all makes sense since travel is really getting more expensive. For a family of 4 in Europe, you are dropping 15-30k for two weeks... just a bit more for eco plus or even J on sale.

"you could largely attribute the increase...to extra legroom economy seating"

Exactly. I'm more curious about the cabin metrics (and no, extra legroom isn't a separate cabin).

It's a bit odd to me that Comfort+ is classified as premium cabin.

It's still an economy seat in the economy cabin by all metrics, it feels a little dishonest, especially since they anyways give them away for free a lot of the time to status passengers unlike true D1/PS which aren't eligible for upgrades on international itineraries.

Weird way to word "Economy class underperforms for DL"

Very weird mindset to have.

Underperformed implies there's a bar that they are benchmarking against, this is just a relative comparison.

If premium cabin revenue was only $5B this time around, but economy revenue was the same, would you still say it underperformed?

Maybe, maybe not. A much better metric would be $/square foot, or $/square foot/hour, or something like that. You can't really tell who's overperforming just based on raw revenue.

"Will aircraft LOPAs change more radically over time?"

I thought about this before, but what if angled lie-flat seats became the new Premium Economy. Something like United's domestic 777s or business class of years past. But I figured that will probably cannibalize Business Class.

So probably the next best thing IMO would probably a deeper recline of Premium Economy, something like a La-Z-Boy.

In the mean time, plenty of carriers have increased their capacity such...

"Will aircraft LOPAs change more radically over time?"

I thought about this before, but what if angled lie-flat seats became the new Premium Economy. Something like United's domestic 777s or business class of years past. But I figured that will probably cannibalize Business Class.

So probably the next best thing IMO would probably a deeper recline of Premium Economy, something like a La-Z-Boy.

In the mean time, plenty of carriers have increased their capacity such as CX.

It could mean that J needs to become F for better product differentiation.

Originally, a lot of carriers were scared of PE cannibalizing J, but it seems to have not been the case. Rather than business class people booking down, you have economy class booking up. I could see the PE evolving to angle flat 2-4-2 or 2-3-2 if an efficient enough product can be created.

The reason why PE works today isn't because the...

It could mean that J needs to become F for better product differentiation.

Originally, a lot of carriers were scared of PE cannibalizing J, but it seems to have not been the case. Rather than business class people booking down, you have economy class booking up. I could see the PE evolving to angle flat 2-4-2 or 2-3-2 if an efficient enough product can be created.

The reason why PE works today isn't because the product is that amazing, it's because it uses only marginally more space than economy, usually a 30 to 40% increase, but yields much more proportionally, often as high as double of economy.

How lieflat J cannibalize F is already on the wall.

There is a big rumor going around that UA is planning to reconfigure their 737-700s with a 24 seater first class cabin. While it's just a rumor, word is its more likely to happen than not. As to why, I'm not quite sure.