In March we first learned that American Express would be ending the OPEN Savings program as of June 1, 2018. With this program, those with American Express business cards could earn extra rewards for purchases with select retailers, including FedEx, Hertz, HP, and 1800Flowers.com.

Specifically, if you had an eligible card, you could choose to receive either 5% off or two bonus Membership Rewards points per dollar spent. This was a nice additional reward for those with an Amex business card.

At first there was no indication that Amex would introduce a new program, though it looks like they have. As of June 1, 2018, American Express has introduced the “Do More Business” program. This is essentially an extension of the popular “Amex Offers” program, which offers savings for purchases with select retailers.

- American Express® Business Gold Card

- Delta SkyMiles® Gold Business American Express Card

- The Business Platinum Card® from American Express

- Delta SkyMiles® Platinum Business American Express Card

- Delta SkyMiles® Reserve Business American Express Card

- The American Express Blue Business Cash™ Card

- The Blue Business® Plus Credit Card from American Express

- Marriott Bonvoy Business® American Express® Card

- The Hilton Honors American Express Business Card

- Access to Amex Offers

- Redeem Amex Points Towards Airfare

- $375

- Earn 2x SkyMiles on purchases directly with Delta

- First Checked Bag Free

- Priority Boarding

- $0 introductory annual fee for the first year, then $150

- Earn 1.5x on purchases of $5,000 or more in a single transaction on up to $2MM per calendar year

- Redeem Points For Over 1.5 Cents Each Towards Airfare

- Amex Centurion Lounge Access

- $695

- Earn 3x SkyMiles for purchases directly with Delta

- First Checked Bag Free

- Annual Companion Certificate

- $350

- Annual Companion Certificate

- Upgrade Priority

- First Checked Bag Free

- $650

- 2% cash back up to $50k then 1%

- Access to Amex Offers

- No annual fee

- 2x points on purchases up to $50k then 1x

- Access to Amex Offers

- No annual fee

- Earn 6x points at Marriott

- Free Night Award Annually

- 15 Elite Nights Towards Status Annually

- $125

- Earn 12x points at Hilton Hotels

- Hilton Honors Gold Status

- Hilton Honors Diamond Status With Spending

- $195

Amex says that the “Do More Business” program will offer 5-10% savings on many types of business expenses.

The program is integrated into Amex Offers, and if you just log into your Amex dashboard you won’t even see these offers listed separately. However, if you log into your account through americanexpress.com/domorebusiness, you’ll see that it generates a separate tab with these offers.

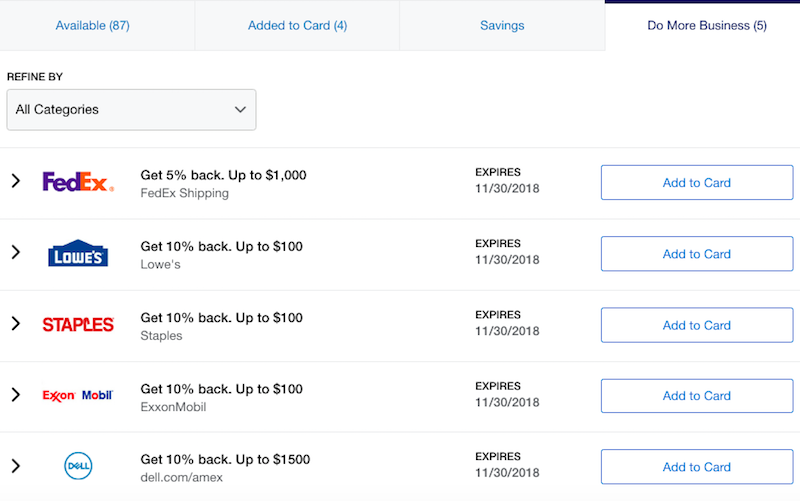

To start, it looks like there are five offers, as follows:

- FedEx: Get 5% back, up to $1,000, through November 30, 2018

- Lowe’s: Get 10% back, up to $100, through November 30, 2018

- Staples: Get 10% back, up to $100, through November 30, 2018

- ExxonMobil: Get 10% back, up to $100, through November 30, 2018

- Dell: Get 10% back, up to $1,500, through November 30, 2018

This is a positive development, especially if these offers rotate over time. The savings amounts are significant, the offers are valid for many months, and the retailers actually seem like they could be useful. So far I’m impressed by this program.

American Express has quite a few excellent business cards, and probably my three favorite are the following:

- American Express® Business Gold Card earns 4X Membership Rewards® points on the 2 categories where your business spends the most each billing cycle from 6 eligible categories. You will earn 4X points on the first $150,000 in combined purchases from these categories each calendar year (then 1X thereafter). (learn more about the card here)

- The Blue Business® Plus Credit Card from American Express has no annual fee (Rates & Fees) and offers 2x points on the first $50,000 spent annually (1x after that) (learn more about the card here)

- The Business Platinum Card® from American Express has excellent perks (learn more about the card here)

What do you make of the Amex “Do More Business” program?

(Tip of the hat to Rapid Travel Chai)

The following links will direct you to the rates and fees for mentioned American Express Cards. These include: The Blue Business® Plus Credit Card from American Express (Rates & Fees).

In March of 2018, my open savings program ended. As of June 1, 2018, the "Do More Business" program began. That's amazing!

However, I just go notified of it through a FedEx mailing today, July 5, 2019!!! ONE YEAR AFTER STARTING!!

IS THIS THE BEST YOU CAN DO AMEX?

SO GLAD YOU KEEP YOUR LOYAL CUSTOMERS UPDATED ON NEW PROGRAMS.

VERY DISAPPOINTED.

I DID ENROLL TODAY FOR THE SAVINGS...LET'S SEE HOW THIS GOES?!?!?

Does each employee card need to be registered separately?

This is awful for business, compared to OPEN Savings. As a business owner, I'm not interested in rotating offers with low caps, like these. I want consistent savings, like before. Just another way in which AmEx is cutting benefits. Yuck.

Got 25% back on FedEx up to $1000 on my SPG Business card

My FedEx offers vary by card flavor. I’ve got 5/10/15/25% off up to $1K

Have you retired?